ECONOMIC OVERVIEW

- A collection of Chilean, Peruvian, and Brazilian economic data, regional unemployment figures, and Banxico’s quarterly report are accompanied by inflation data out of the US, the Eurozone, and Japan, Canadian GDP, and the RBNZ kicking off the next round of central bank decisions.

- In today’s report, our team in Mexico argues that the Mexican economy will rebound in H1-24 thanks to fiscal spending ahead of the June elections. We’ll see how Banxico feels in next week’s quarterly report, coming on the heels of an inflation miss and meeting minutes that point to a March rate cut majority.

- Peru’s CPI print on Friday may show an uptick in inflation, but our economists believe mining, oil/gas, and fishing output data are the most interesting to watch. After a weak 2023, we think 2024 started out with a strong rebound in output with supportive base effects but also with the country’s economy turning the corner.

- Chile’s macro flood on Thursday is followed by Friday’s monthly economic activity data where a growth rebound is expected. This may help out the beaten CLP, to which our team in Santiago does not think the BCCh should respond, seeing limited risks of currency weakness to pull away inflation from its convergence to target.

- Colombia’s calendar is quiet outside of unemployment figures and a non-rates-setting BanRep meeting. Brazil publishes mid-Feb prices data expected to show sideways inflation in the mid-4s, and closes out the week with Q4 GDP figures that should confirm the country’s soft economic performance over H2-23.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Mexico and Peru.

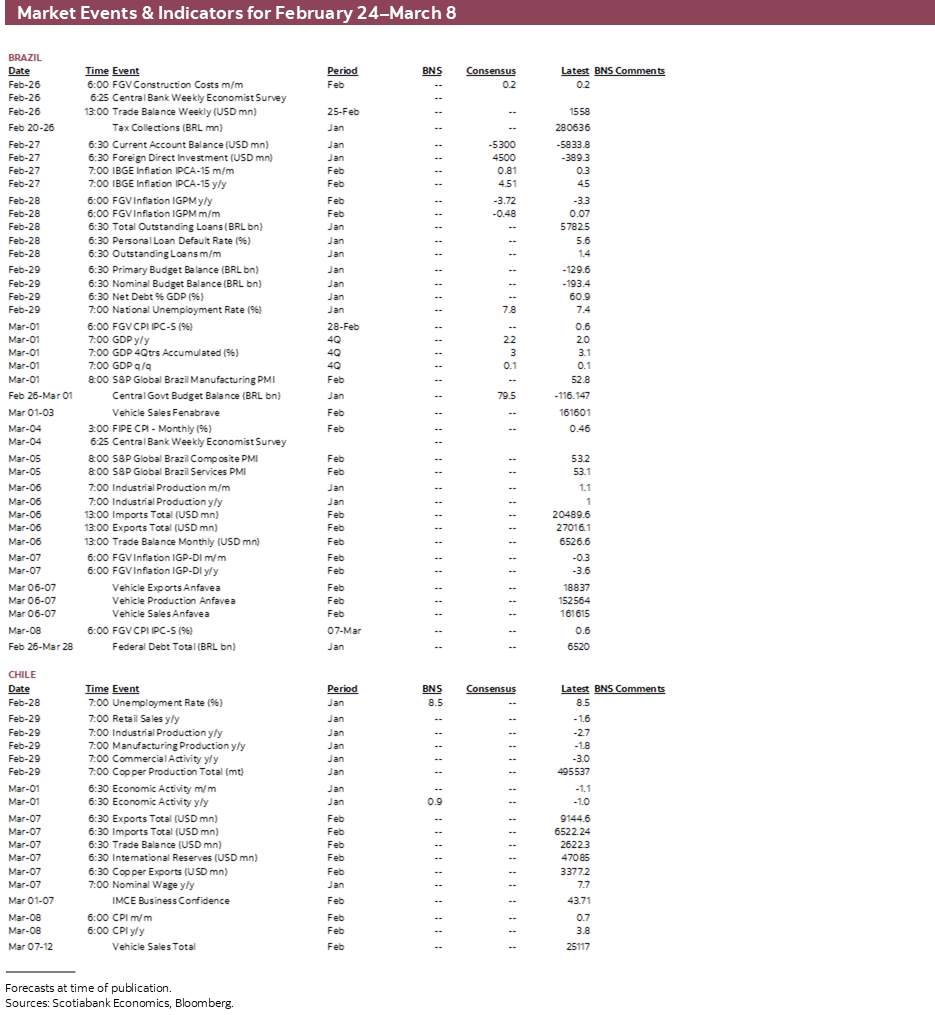

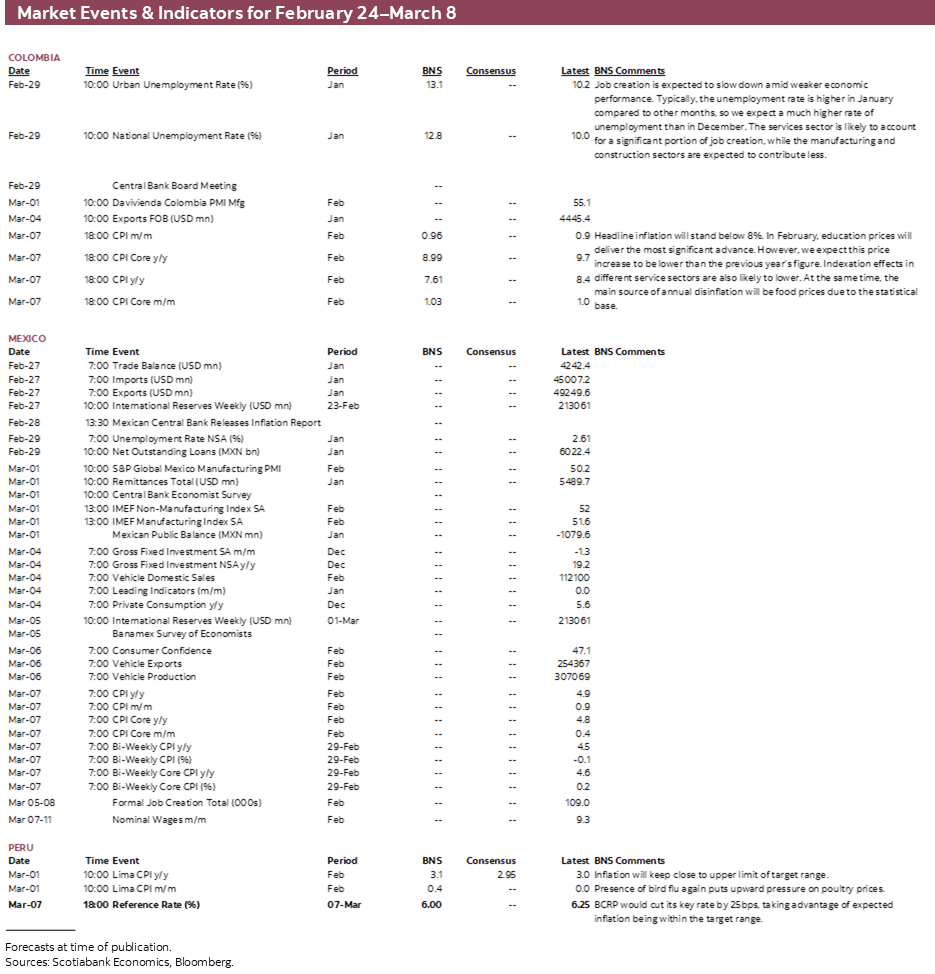

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period February 24–March 8 across the Pacific Alliance countries and Brazil.

Charts of the Week

ECONOMIC OVERVIEW: CHILE AND PERU MACRO, BANXICO REPORT

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- A collection of Chilean, Peruvian, and Brazilian economic data, regional unemployment figures, and Banxico’s quarterly report are accompanied by inflation data out of the US, the Eurozone, and Japan, Canadian GDP, and the RBNZ kicking off the next round of central bank decisions.

- In today’s report, our team in Mexico argues that the Mexican economy will rebound in H1-24 thanks to fiscal spending ahead of the June elections. We’ll see how Banxico feels in next week’s quarterly report, coming on the heels of an inflation miss and meeting minutes that point to a March rate cut majority.

- Peru’s CPI print on Friday may show an uptick in inflation, but our economists believe mining, oil/gas, and fishing output data are the most interesting to watch. After a weak 2023, we think 2024 started out with a strong rebound in output with supportive base effects but also with the country’s economy turning the corner.

- Chile’s macro flood on Thursday is followed by Friday’s monthly economic activity data where a growth rebound is expected. This may help out the beaten CLP, to which our team in Santiago does not think the BCCh should respond, seeing limited risks of currency weakness to pull away inflation from its convergence to target.

- Colombia’s calendar is quiet outside of unemployment figures and a non-rates-setting BanRep meeting. Brazil publishes mid-Feb prices data expected to show sideways inflation in the mid-4s, and closes out the week with Q4 GDP figures that should confirm the country’s soft economic performance over H2-23.

The past five days have been relatively quiet in Latam as domestic calendars were bare of major data or events—with the exception of Mexico where a busy Thursday was the highlight. Next week’s schedule is a bit fuller and better distributed across the key Latam economies as things start to pick up across the region and in the G10 ahead of March policy decisions. A collection of Chilean, Peruvian, and Brazilian economic data, regional unemployment figures, and Banxico’s quarterly report are accompanied by inflation data out of the US, the Eurozone, and Japan, Canadian GDP, and the RBNZ kicking off the next round of central bank decisions.

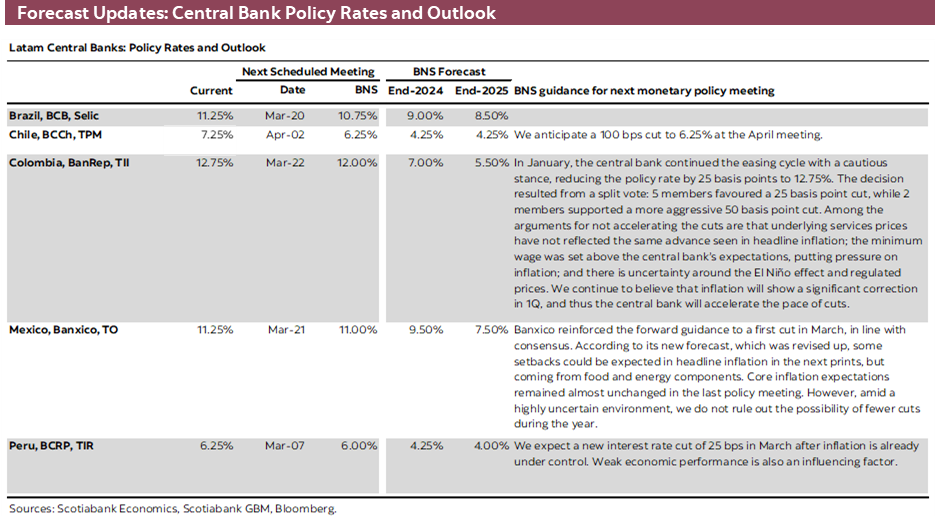

Banxico’s quarterly report due Wednesday will help us get a better sense of how officials perceive the risks to their inflation goal, presenting their outlook for the economy after a disappointing end to 2023. Still, the publication is unlikely to influence markets to the degree that the recent inflation and GDP data, and Banxico minutes releases did (see Latam Daily).

Final Q4-23 GDP and December IGAE data out this week reaffirmed Mexico’s economic deceleration in the final months of 2023. Our economists argue in today’s report that this soft patch will be short-lived, followed by a strong first half of 2024 thanks to a fiscal boost ahead of the June presidential elections. As for CPI, inflation came in below expectations in H1-Feb data published yesterday, with the miss driven by a sizeable deceleration in non-core prices that had been driving upside surprises of late.

A string of hotter prints was starting to build some anxiety in bets that Banxico would start its rate-cutting cycle next month; to some degree, the pushing out of the expected start of Fed easing was also niggling. Now, Thursday’s softer inflation print and Banxico’s January meeting minutes—that suggested the most popular view among officials was a March cut—have left the market more confident about its March call.

It’s now Chile’s turn to have a Súper Thursday, with its customary release of retail sales, industrial/manufacturing production, commercial activity, and copper output figures, all for January, due on the same day, the 29th. The next morning, the INE will publish January economic activity data that we expect will show a 0.9% y/y increase to claw back some of the 1.0% contraction recorded in the final month of 2023. This would be a similar pattern to that of industrial/manufacturing data reported on Thursday, while retail sales may edge closer to the zero mark after twenty months of year-on-year contractions. On Wednesday, unemployment rate data should have little impact on markets.

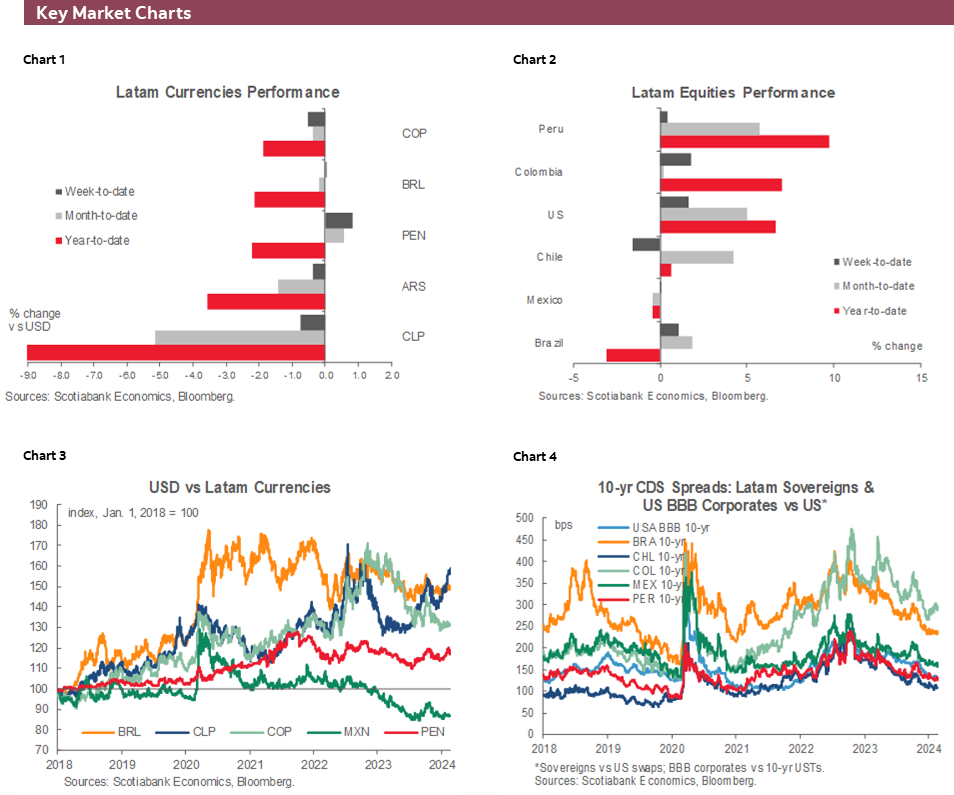

Maybe if we get some better Chilean data the recent rally in the country’s front-end will hit a wall. And maybe that could help the CLP, which has lost over 10% year-to-date vs the USD. But, our economists do not think this should be too much cause for worry, as they outline in today’s Weekly. As far as the BCCh is concerned, “it is not a problem for monetary policy, since inflation is around 3% and any exchange rate pass-through on tradable goods and eventual second-round effects will be mitigated by a weak cyclical position.”

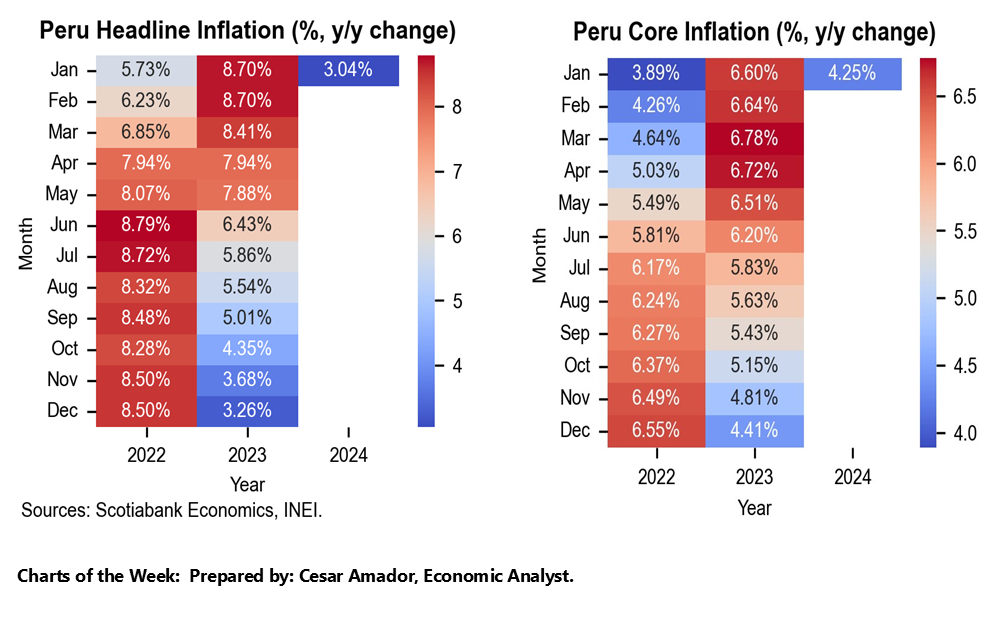

As always, Peru’s statistical agency is the first to release full-month inflation figures, but we’ll have to wait until Friday for February CPI data. There’s no doubting the encouraging path of inflation in Peru, going from 8.7% in January 2023 to 3.0% y/y last month. February’s data may see this progress stall somewhat according to our economists’ tracking of prices that tees up a 0.4% m/m increase for a 3.1% y/y print. It’s just a bump in the road however, so the team thinks that next week’s most important releases will be those for January mining, oil and gas, and fishing output published alongside the CPI data. As they cover in today’s report, sectoral output data for January “will be key to paint the picture for the rest of the year” as their early estimate of 2% y/y growth for the month would be a strong way to break the negative prints that we got through most of last year, and a nice way to start 2024.

Elsewhere in the region, Colombia’s calendar is bare of market-moving releases with only unemployment figures on tap. BanRep’s meeting on Thursday is not a rate-setting meeting, but maybe they’ll come closer towards a decision to cut rates by the 75bps that we expect at the March 22nd decision. Brazil’s schedule has a couple of key releases. On Tuesday, IPCA-15 figures for February are expected to show no progress in inflation, holding around the 4.5% y/y reading for January, as food and fuel prices apply upward pressure on the overall basket. Outside of non-core risks, services inflation has to cool its advance or markets may be a bit more hesitant about their call for another 50bps cut at the May meeting (currently pricing in 42bps). Brazil’s week ends with the release of Q4 GDP data on Friday, where the median economist expects practically no growth q/q after a similarly soft 0.1% q/q rise in Q3; expansions of 1.4% in Q1 and 1.0% in Q2 were certainly not repeated as those owed plenty to a surge in agricultural output.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—We Will Not Have an Exchange Rate Intervention

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

The Chilean peso (CLP) has shown a relevant multilateral depreciation. Nothing surprising in a context of high exchange rate volatility generated by the reduced depth of the capital market and the erratic probability of seeing a closure of the structural reforms (tax and pension) in the short term. In addition to the above, there is an inadequate level of international reserves. Both dimensions are the main determinants of the higher exchange rate volatility and the preponderant role of foreigners on the exchange rate, through the wind and unwind of the carry trade.

In this context, the CLP has depreciated multilaterally, with our Central Bank (BCCh) being particularly proactive in its view of the monetary policy rate in recent times. This has occurred in a scenario in which some central banks have joined this view, but somewhat more timidly. Thus, the positions that favoured the interest rate differential have been unwinding with a reactivity on the exchange rate markedly higher than that observed before May 2021.

Is this large multilateral depreciation that has pushed the real exchange rate above what is considered equilibrium a problem for monetary policy? We believe it is not. It is not a problem for monetary policy, since inflation is around 3% and any exchange rate pass-through on tradable goods and eventual second round effects will be mitigated by a weak cyclical position. The current inflationary level is also very important. It is not the same to have a real depreciation of 15%—as the one observed between June 2023 and February 2024—with low inflation than to have it with double-digit inflation. We should have monthly inflation reflecting the exchange rate pass-through and a narrow margin in these first months of the year, together with the usual indexation effects. Nothing dramatic and unlikely to prevent convergence to 3%. Moreover, this “summer” inflationary concentration becomes a challenge for monetary policy, not to bring inflation back to 3% as seems to be the consensus expectation, but to keep it around that figure during the second half of the year.

Indeed, the pressure from domestic demand will be opaque and the exchange rate will return closer to its equilibrium level. In this context, we continue to believe that the scenario of a monetary policy rate below neutral is gaining strength for the second half of the year, just as we expected months ago that the benchmark rate would be at its neutral level by mid-year, as seems to be the consensus today. Is it time to intervene? The answer follows from the previous reflection. First, any intervention will lack credibility given the low level of international reserves, which we should recover, hopefully sooner rather than later. Moreover, an intervention that might eventually be successful would only increase the probability of having inflation sharply below 3% towards the policy horizon and, consequently, would further increase the probability of a rate below neutral, quickly dulling the desired effect on the exchange rate. The automatic adjustment of the economy, where serious macroeconomic imbalances have been absent for some time now, is taking place. In this scenario, the only thing to do is to allow relative prices to adjust. Let us hope that the political side of the equation does not generate events that prevent the above, but, on the contrary, facilitate this process.

Mexico’s Economy Confirms Slowdown at the End of 2023… We Expect it Will be Temporary

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Mexico’s economy confirmed its slowdown as it headed towards the close of 2023, but a sharp increase in the public deficit heading into the June 2024 election (the Public sector’s Borrowing Requirements are projected to grow from 3.0% of GDP to 5.4%), the economy is set to receive close to US$30bn in fiscal boost. With that in mind, we anticipate that the weakness in activity at the close of 2023, will be reversed in the first half of 2024 (the election will take place the first Sunday of June). In addition, supply chain disruptions related to drought in the Panama Canal, and geopolitical risks in the Suez Canal, alongside the El Niño weather pattern suggest there are lingering upside risks to inflation. We see these risks more as threats of slowing inflation drops rather than major upside risks to inflation, but they are worth keeping an eye on. Banxico’s communication seems to suggest that a start to the easing cycle could come as soon as March’s meeting, and we tend to agree that the table is set for it, given the policy rate is around 450bps on the “tight side”, which would seem to give Banxico room to safely cut about 100–150bps in the current environment. We expect cuts beyond that will likely accompany falls in core-CPI as well as easing by the Fed.

Peru—Remember That Thing Called Positive GDP Growth? Well, It’s Coming Back!

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

We’ll be receiving plenty of information next week on March 1st. The most important data may not be February inflation, as one might expect for what it might mean for monetary policy, but, rather, sector data growth, which should give us a better idea of the performance of aggregate GDP growth for January. Data GDP growth will be key to paint the picture for the rest of the year. We expect growth of close to 2.0%, y/y. If this is accurate, then it will mean a clean break from negative monthly growth that occurred throughout most of 2023.

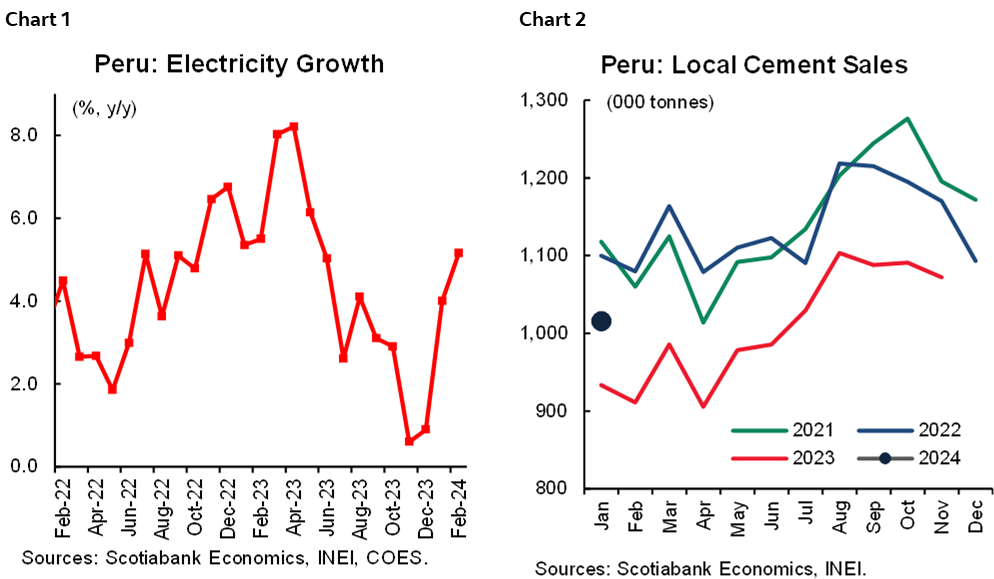

Why are we so optimistic (if 2.0% growth can be called optimistic)? Part of the reason was that GDP performed dismally in January 2023, due to changes of authorities at all levels, protests that all but paralyzed parts of the country, and high inflation. None of these factors persist today, and given the low y/y base, there is bound to be a rebound in growth. The question is how much? So far so good on the data front. Electricity grew 4.0% in January (and is up 5.2% to date in February), compared to 1.5% growth on average in the fourth quarter of 2023 (chart 1). Cement sales, a proxy for construction, soared 9% YoY in January (let’s not get too excited, it was off a very low base) (chart 2). Both figures portend not only positive growth in GDP, but, significantly, a robust rebound in domestic demand, which has long been a concern of ours.

Next week we will the release of figures for mining, oil & gas, and fishing. These figures will tell us to what extent natural resource sectors are reinforcing the rebound in domestic demand sectors. Mining GDP growth should continue to be positive, but only mildly so, as the impact of the new Quellaveco mine, which was fully operational in 2023, will have exhausted itself. Fishing GDP growth will likely be negative, as the fishing season ended in December this time around, whereas it had extended into January last year. But the impact won’t be material, given the low weight fishing has in GDP.

Also helpful in terms of GDP is that El Niño is not having the impact we had feared so far in 2024. Rains in the north and weather in the south are bordering on normal. The only anomaly that is occurring so far in 2024 is that it is an unusually hot summer, and heat can have some impact on agricultural productivity. We won’t know if that was the case in January until the agriculture GDP figure is released later in March.

The upshot of the January GDP figure to be released is to what extent will it vindicate the notion that 2024 will be better than 2023.

February inflation will also be released. Yearly inflation fell from 8.7% at the beginning of 2023, to 3.0% in January. This strong decline is likely to pause in February. The key prices we track point to a monthly inflation of 0.4% to date. This is a tick above 0.3% in February 2023, which means that there is a good chance that inflation might rise a bit, or at least keep stable. The pause in the inflation downtrend may extend to March, but the downtrend should resume in April. The BCRP knows this, and we do not expect it to modify its monetary policy.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.