- Mexico: Inflation surprised lower, markets pay attention to the non-core component; Q4-23 GDP confirmed an economic slowdown at the end of the year, highlighting decreases in construction and manufacturing; Banxico’s minutes show a further discussion on inflation and policy rates

MEXICO: INFLATION SURPRISED LOWER, MARKETS PAY ATTENTION TO NON-CORE

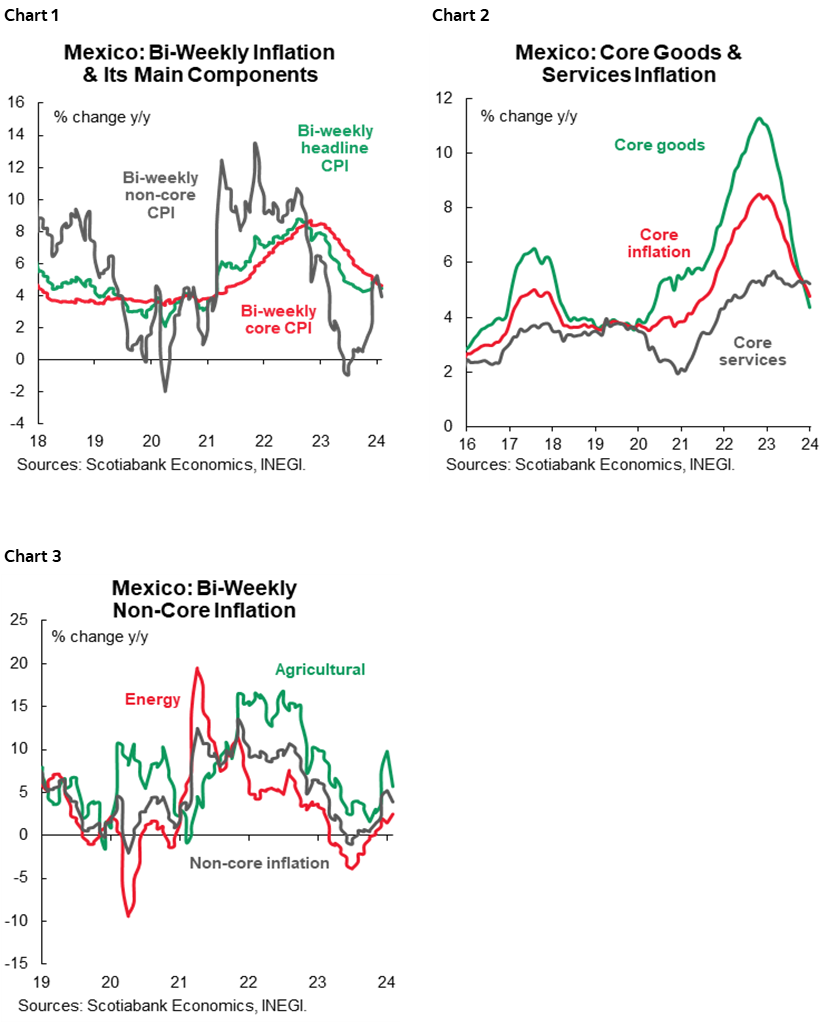

In the first half of February, inflation surprised as it moderated to 4.45% from 4.87% (vs. 4.70% consensus, chart 1), while core inflation slowed from 4.75% to 4.63% (vs. 4.67% consensus, chart 2). Merchandise decelerated 4.09% (4.28% previously, chart 2 again) and services decelerated 5.28% (5.31% previously). On the other hand, non-core inflation fell to 3.93% (5.25% previously, chart 3), highlighting agriculture, which moderated its pace to 5.69% (9.77% previously). In its biweekly sequential comparison, headline inflation fell -0.10% (0.32% previously, 0.18% consensus), while the underlying component slowed down 0.24% (0.32% previously, 0.27% consensus) and non-core fell -1.10% from 0.32 %.

Core inflation has exceeded 4.0% annually for 16 fortnights (although below 5%), due to the fact that services are the component that has most resisted moderating its pace, with 38 fortnights exceeding 5.0%, while merchandise show a faster deceleration.

Regarding non-core inflation, it has registered 13 fortnights of consecutive annual increases, mainly due to agriculture, which reached its lowest level in October 2023 (standing at 1.61% y/y), in addition, energy products remain with low variations. We expect that in the next prints the non-core component may increase, and it will be important to monitor any relevant weather events, as well as issues in the global supply chain. The non-core component will continue with volatility, which will bring uncertainty for the next Banxico meetings, so its best indicator will be the core component.

Q4-23 GDP CONFIRMED AN ECONOMIC SLOWDOWN AT THE END OF THE YEAR, HIGHLIGHTING DECREASES IN CONSTRUCTION AND MANUFACTURING

The final GDP estimate for Q4-23 confirmed an economic slowdown at the end of the year, going from 3.3% to 2.5%. By sector, industry slowed to 2.8% y/y (vs. 4.4%), derived from a slowdown in construction, to 20.2%, after the vigorous advances observed since the end of 2022, the trend is expected to continue to moderate to finish the emblematic projects of the current public administration. Additionally, manufacturing fell -1.0% (0.1% previously), affected by a slower pace in most of its components, except for transportation equipment, which continues with a favourable outlook thanks to the phenomenon of relocation of production chains, as well as a solid demand, both in Mexico and in the United States. On the other hand, services also moderated, from 3.0% to 2.4%. Primary activities also showed less progress, from 5.6% to 0.3%. In seasonally adjusted quarterly terms, GDP slowed down to 0.1% q/q, from 1.1% previously, below the consensus of 0.4%. Industry decreased -0.1% q/q (1.0% previously), the services sector fell to 0.3% (0.9% previously) and the primary sector fell -1.0% (2.6% previously), see table 1.

Derived from the slowdown observed in the period, the consensus slightly revised downwards the growth expectation in the last Citibanamex Survey, from 2.5% to 2.4%. At Scotiabank, we maintain the perspective of greater pace in economic activity during the first half of the year, encouraged by greater public spending (concentrated on social spending), by the solidity of household income (thanks to a labour market with a lower-than-average unemployment rate, and at a historically high rate in remittances), as well as the optimism surrounding nearshoring. However, we do not rule out the risk of a further slowdown due to weakness in the industry, which may not be offset by the strength of services.

BANXICO’S MINUTES SHOW A FURTHER DISCUSSION ON INFLATION AND POLICY RATES

Banxico’s minutes from February’s meeting showed further discussion around the inflation trajectory and future policy decisions. Although most members signaled that they would opt to adjust the rate downward at the next meeting, members agree that the balance of risks has shifted slightly upwards, mainly due to the non-core component of inflation, so we do not rule out the chance that they will keep the rate at the same level, depending on the next inflation prints. In this regard, the members noted that, despite recent increases in inflation, the core component has been observed to be slowly on the downside during 2023. The Board of Governors’ guidance on possible cuts remains in line with market expectations, as analysts still expect the first cut in March to be 25bps, and the curves have also discounted this. However, given the details in the minutes, we believe that the next decision may not be unanimous.

On the more dovish side of the Board, we find the following remarks from three of the members. In general, one of them pointed out that “shocks like the recent ones tend to reverse relatively fast” predicting that headline inflation will resume its downward trend soon, after surging during the last few months. Another member highlighted the speed with which inflation has decelerated since its peak in late 2022; mentioning that the ex-ante rate has remained in restrictive territory since then. He noted that “given the expected disinflation and the passive increase in the real interest rate, if the reference rate is not adjusted, the ratio between both gaps could increase significantly and above what is necessary.” However, they acknowledged the possibility of changes in the inflation forecast, which implies a short window for rate adjustments, under its previous argument. A third member also pointed to the “passive tightening” that the target rate has registered, posing that “when inflation has been at similar levels, nominal and real interest rates have been well below current levels.” Overall, we note that the arguments of the dovish board members are based in the expectation of a slowdown in headline inflation in the coming months, which would implicitly lead to a higher real rate in the absence of policy rate adjustments.

On the side of the two members who showed a more cautious tone, they highlight concerns about inflation dynamics. One of the members warned that “the fact that it may be necessary to maintain the current level of the reference rate longer than anticipated by market consensus cannot be ruled out.” The other member considered that the inflation forecast is optimistic, as it assumes that the increase in non-core inflation is temporary, although there is no certainty about this. This member commented that “it will be necessary to make sure that the rebound in non-core inflation does not spill over to core inflation, that monetary policy has its expected impact on aggregate demand and that shocks to non-core inflation are effectively reversed.” He also considered that monetary policy in Mexico is not as effective as it is in other countries, and therefore requires more lasting monetary restriction.

In conclusion, we believe that the Board of Governors recognizes some concerns on the recent rebound in inflation, although it expects that it will quickly resume its downward trajectory, which would give room to cut the rate in March. The inflation print for the first half of February supports this argument, as it came in below expectations, owing to a slower pace in both core and non-core items. However, it will be necessary to maintain this trend until the next meeting (March 21st) to ensure a cut in the rate. Some events such as the El Niño phenomenon and recent global chain disruptions complicate this outlook. Therefore, we maintain our stance of a first cut in March; although, like Banxico, we remain attentive to the upcoming data, and we do not rule out the risk of a sufficiently high rebound in inflation, which would take away the space for an adjustment at the next meeting.

—Brian Pérez & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.