- Mexico’s recent jump in inflation expectations implies that Banxico’s surprise policy-rate hike wasn’t a one-off signaling move and instead marked the beginning of a front-loaded tightening cycle.

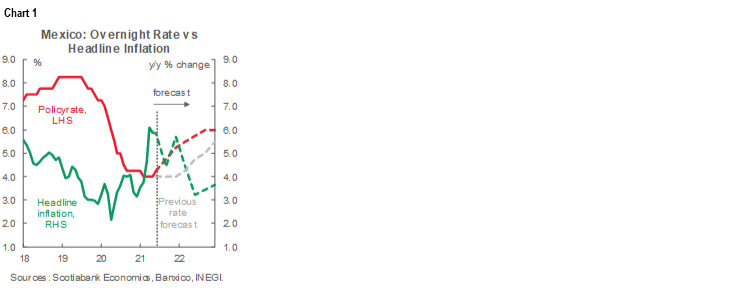

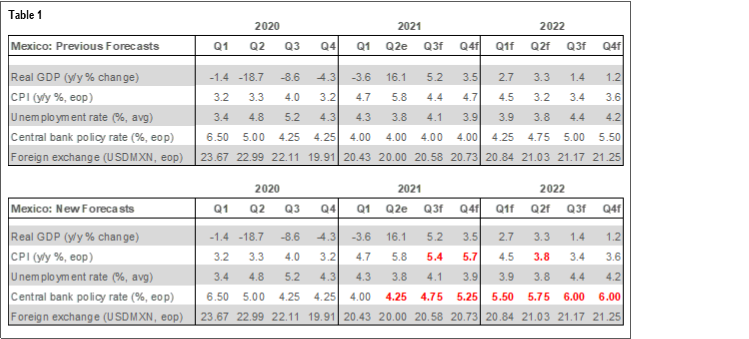

- We now anticipate 100 bps of further tightening in the remainder of 2021 to take the target rate to 5.25% by December, followed by another 75 bps during 2022 to reach a terminal rate of 6.00% in Q3-2022.

REVISED FORECASTS FOR FRONT-LOADED RATE HIKES

Recent events signal that Mexico’s central bank, Banxico, has taken its first steps into a tightening cycle that started with a surprise 25 bps rate hike by the Board on June 24 from 4.00% to 4.25%. Against a challenging inflation outlook and the impending change in leadership at Banxico, we now expect a further 100 bps of tightening coming in 2021 to close the year at 5.25% compared to our earlier 4.00% forecast for end-2021 (chart 1).

We have also adjusted our longer-term profile for monetary policy in Mexico to a 6.00% terminal rate by Q3-2022—essentially the neutral real policy rate based on our inflation forecasts—up from 5.50% in Q4-2022 in our previous forecast.

We expect to see a front-loaded tightening cycle where the Board will make increases of 25 bps at every meeting scheduled for the rest of this year (i.e., August, September, November and December). A front-loaded cycle should further ease the central bank’s leadership transition, as Governor Diaz de Leon’s mandate at the helm of Banxico will conclude at the beginning of 2022.

Our revised rate call reflects both a fresh assessment of Banxico’s stance and of Mexico’s macroeconomic outlook (table 1). Compared with our last published forecasts in the June 18 Latam Weekly, our projection for end-2021 inflation has been lifted from 4.7% y/y to 5.7% y/y, mainly to reflect substantially stronger actual price increases so far in H1-2021. Our forecast for the USDMXN is, however, unchanged despite our expectation of higher Mexican policy rates. While this may appear counterintuitive, we’ve kept our FX forecasts unaltered as our current path of cross-rates is already priced by markets in tandem with the rate cycle we now anticipate. Moreover, recovering domestic demand is shrinking Mexico’s trade surplus just as the specter of Fed tapering nears, both of which are curbing support for the peso.

JUNE’S SURPRISE HIKE LIKELY KICKSTARTED A TIGHTENING CYCLE

Banxico’s surprise 25 bps hike on June 24 caught the market off-guard, as previous communications from the central bank had signaled that inflationary pressures were perceived as temporary and ill-suited for monetary-policy fixes. Moreover, in its Quarterly Inflation Report (QIR), published three weeks prior to the surprise decision, Banxico had revealed an expectation that inflation would get back to the mid-point of its target range by June 2022, well within the policy horizon.

Recent inflation pressures, even where broadly seen as transitory, have, however, affected expectations for the 12 to 24-month horizon in which monetary policy operates. An angle that we, and the overwhelming majority of market watchers, may have missed earlier is that under Governor Diaz de Leon, Banxico appears to be placing increased weight on inflation expectations. In this sense, we note that over the past few months, private-sector expectations have increasingly diverged from Banxico’s target. For instance: according to Banxico’s latest survey of private-sector economists, expectations are for headline inflation to close 2021 at 5.80% y/y, with convergence to the 3% y/y target likely be achieved by Q3-2022 and not Q2 as the most recent QIR implied.

With the possibility that inflation expectations could become unmoored and transform a transitory spike in inflation into a more long-lasting phenomenon, we believe Banxico’s Board is now inclined to act to ensure this doesn’t happen.

A BOARD THAT HAS BEEN HARD TO READ

There remains lingering uncertainty over the policy bias going forward, given the mixed signals that followed the June 24 hike and what is likely to be a more dovish tilt under the new Governor who takes over at the start of 2022. Banxico’s Board statement had noted the 2–3 split-vote decision behind the hike, but in the minutes released on July 8, the Board’s mixed views became even clearer as at least one Board member was decidedly against an abrupt change in the narrative.

From the minutes we have now also confirmed our earlier speculation about the vote-split: Governor Diaz de Leon, alongside Deputy Governor Espinosa supported a more hawkish stance and backed the start of a formal tightening cycle. On the opposite side, Board members Esquivel and Borja were not yet ready to tighten rates and continued to support a dovish bias. The tiebreaker vote sat with Deputy Governor Heath, who backed the June 25 bps hike to anchor expectations.

Although Deputy Governor Heath is perhaps less committed to a full-blown tightening cycle than the two Board members with whom he voted, we infer a change in tone from previous statements based on the June 24 meeting comments. If indeed it was Mr. Heath who opined that less monetary stimulus was now needed given the strong economic recovery, a change in perspective by this “swing voter” could hint that indeed more hikes are on the horizon, as we now expect.

RISKS COULD DRIVE FEWER OR MORE RATE INCREASES THAN WE NOW FORECAST

Even though we have adjusted our forecasts to reflect a much more aggressive and earlier tightening cycle from Banxico than we previously thought, there remain some material risks that the Board could raise rates by a bit less or a bit more.

The possibility of fewer and/or slower rate hikes is tied to the pandemic. Evidence is mounting that Mexico is at the start of a third wave of COVID-19 and the new virus variants are triggering a fresh bout of stricter movement restrictions that could dampen recent increases in activity. It seems unlikely that the impact of this new lockdown will be as severe as earlier ones, but it still adds some downside risks to growth and inflation. Even before any new lockdowns were raised as a possibility by the government in early July, Banxico’s Report on Regional Economies, published June 17, had already pointed toward restrictions pushing parts of the country back into activity decline.

Nevertheless, the dominant risks are to the upside—with the possibility of an even more hawkish path than the new forecasts we’ve laid out here. Mexico’s weak monetary transmission channels accompanied by the possibility of pending inflation shocks with rising expectations now augur for more action rather than less. Mexico’s shallow monetary-policy transmission channels are due to:

- A very low credit to GDP ratio (i.e., credit to the private sector sits at a modest 36.6% of GDP) means higher interest rates affect only a narrow share of the Mexican economy; and

- A relatively long average debt maturity also means that rate resets happen gradually, which also slows the transmission of policy tightening.

THE SIGNIFICANT IMPACT OF INFLATION

According to the June 24 meeting minutes, Banxico’s Board members broadly agreed that inflation has been affected by transitory, supply-side pressures. While we agree that the recent commodity-price surges and supply-chain disruptions are temporary, we also see important forward-looking price risks that warrant caution from Banxico. We lay out the key risks below that underpin our revised forecasts for the policy-rate path.

- Potential evidence of contamination. At this point almost all components of core inflation are rising materially above the top end of Banxico’s inflation target. Additionally, the correlations between different rising price components also seem to be increasing. This is further supported by comments from the June 24 meeting, where a hawkish Board member underscored recent data that showed considerable additional pressures for headline and core inflation.

- Services-sector price pressures. Up to Q2-2021, the services sector has been the hardest hit by pandemic-related mobility restrictions, with sub-sectors such as tourism and entertainment still operating materially below pre-pandemic levels. We anticipate that three things will lead to material inflationary pressures from the services sector: (1) unfavourable base effects as services inflation was near 2% y/y at end-2020; (2) a rapid deployment of vaccines in Mexico and abroad will drive a gathering increase in demand for services, including tourism and entertainment; and (3) with the services sector hard-hit by the pandemic, the spike in demand will provide an opportunity for companies to raise prices to help recover from pandemic-inflicted losses.

- Cost pass-through. The past two years have been marked by a combination of economic contraction accompanied by material producer cost increases for almost all economic sectors. These cost pressures have included the elimination of the outsourcing regime; the close to 40% increase in minimum wages during 2019–20; increases in energy costs; and the recent pension reforms, which mean employer pension contributions will increase from 5.15% to 13.875% of workers’ salaries. In this environment, companies’ margins and balance sheets have been under pressure. Given a relatively strong rebound in demand during 2021, we expect that producers will take the opportunity to transfer some cost pressures over to consumers.

SUMMING UP: OUR REVISED CALL

In this complex environment, and mindful of the uncertainties behind any new rate decisions, our sense is that inflation risks imply that Banxico’s Board has indeed kicked off a tightening cycle.

Given lingering slack in important parts of the economy and the labour market, we believe that Banxico’s Board is, however, reluctant to move by more than 25 bps at a single meeting unless there is a further deterioration in inflation expectations. Hence, our forecast is for a front-loaded cycle to finish the year at 5.25%, with hikes at every upcoming meeting between now and end-2021. We note, though, that Banxico remains concerned about a vulnerable economic recovery and pauses could happen in its tightening path as the impact of hikes are evaluated.

Still, as in any tightening cycle that takes place in an upward inflationary spiral, front-loading policy moves should permit a lower terminal rate, which Banxico will likely take into consideration. Our terminal rate forecast for 6.00% by Q3-2022, compared with our earlier call for 5.50% by Q4-2022, keeps the nominal target rate heading to a neutral level.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.