- Economic recovery continues. Growth forecasts continue to improve, though the pace at which output returns to pre-pandemic levels differs across the region.

- Inflation is higher—everywhere. Recent Fed signalling of a possible tapering of bond purchases and future rate increases highlights the challenges that Latam central banks face in their monetary policy rebalancing act. Meanwhile, financial uncertainties in China associated with Evergrande could trigger a “risk off” in global investor risk appetite.

- These developments underscore the potential effects of less benign global financial conditions. For Latam countries, large currency depreciations stemming from unexpected increases in global interest rates or capital outflows could unleash pass-through effects on inflation, further complicating central bank policy making.

- With growth on track and monetary policy targeting price stability, attention could shift to global factors and their effects on regional financial markets.

KEY ECONOMIC CHARTS

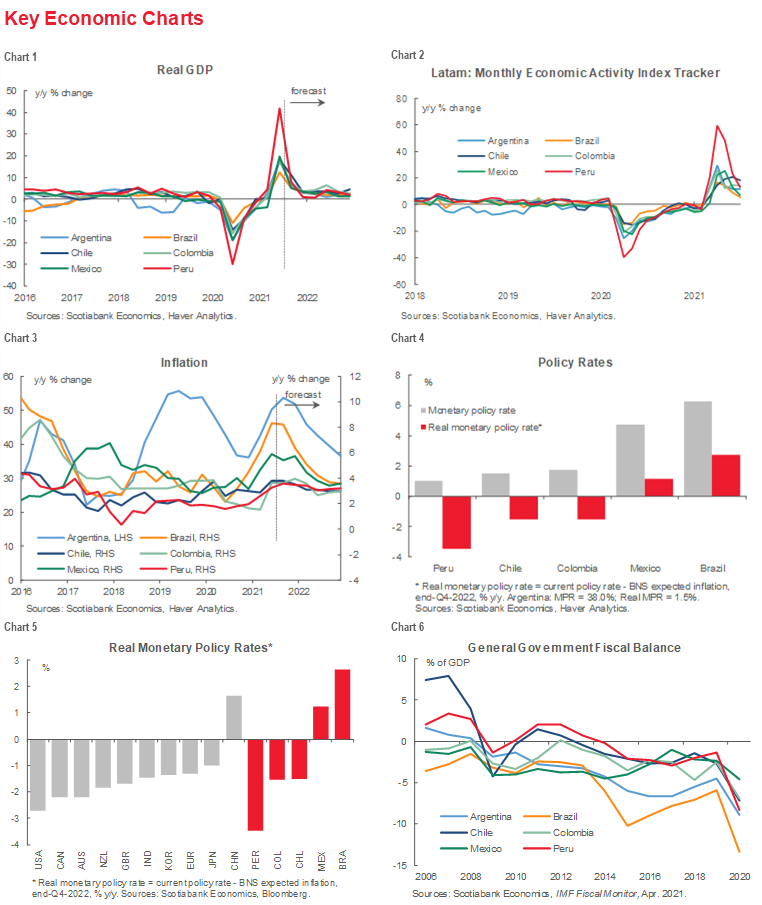

Economies across the Latam region continue to recover in the wake of the COVID-19 shock. GDP has bounced back following a sharp contraction in early 2020 as public health lockdowns around the globe took effect; growth rates are projected to gradually converge on longer-term levels over the near term (chart 1). Monthly activity indices highlight the sharp rebound in 2021, though high year-over-year growth rates are moderating as base level effects dissipate (chart 2).

Consistent with that narrative, private sector growth forecasts in Colombia have been revised up, with GDP growth expected to hit 8.26% in 2021, up from the previous consensus of 7.54%. In Mexico, meanwhile, the monthly GDP proxy showed a continued rebound from the COVID-19 shock in July, but the strength of recovery was below consensus. Our team in Mexico City does not see a return to pre-pandemic levels in real terms until early 2023, well behind regional standards.

Inflation has risen steeply (chart 3), mirroring the economic recovery. Higher inflation poses a challenge to Latam central banks balancing the need to anchor inflation expectations consistent with price stability commitments and the importance of monetary conditions supportive of sustained recovery. Central banks across the region have raised key policy rates, which nevertheless remain negative in real (inflation-adjusted) terms in several countries (chart 4). Brazil and Mexico have moved most aggressively, with policy rates positive in real terms. In this respect, they are well ahead of the tightening cycles of most central banks in the region and around the world (chart 5). Twin rate hikes of 25 bps by BanRep in Colombia and Banxico in Mexico on September 30 are just the latest developments in the Latam monetary tightening cycle. They won’t be the last.

Fiscal balances deteriorated significantly in the pandemic as governments adopted a range of measures to attenuate the effects of the pandemic and support the most vulnerable (chart 6). Accordingly, general government gross debt as a percentage of GDP rose across the Latam region (chart 7). Sustained increases in public debt burdens could animate concerns with respect to sustainability. Latam governments have therefore introduced fiscal reforms or announced plans to ensure long-term debt sustainability. External indicators, including external debt (chart 8), current account balances (chart 9) and total reserves (chart 10), which likewise reflect the effects of the pandemic, remain within comfortable margins.

KEY MARKET CHARTS

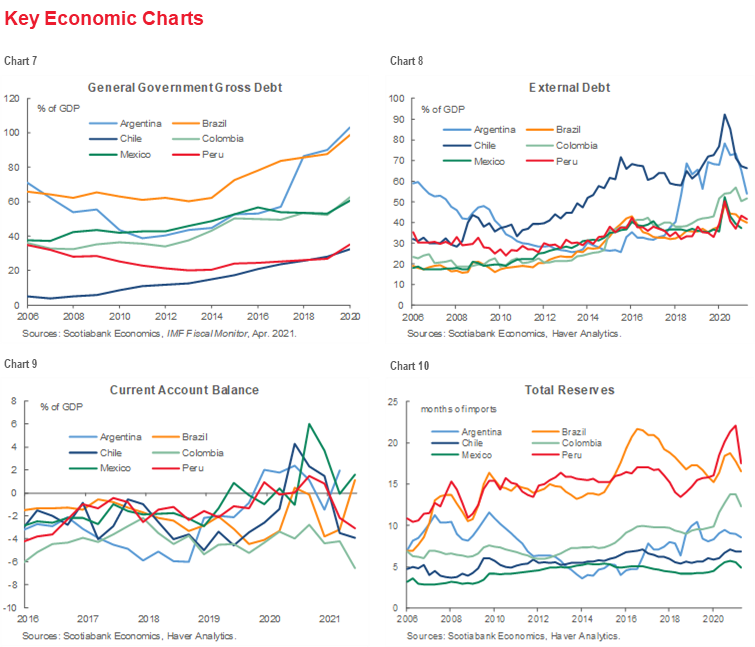

Financial markets in the Latam region have responded to two developments in recent weeks. The first is the Fed’s signalling that it could begin tapering its bond purchases as early as this month and dot plots of Fed governors’ expectations showing that interest rates may go higher, sooner. The second piece of “news” is the financial difficulties of the Chinese developer Evergrande. These developments underscore the potential challenges facing Latam central banks targeting price stability should external financial conditions turn less benign. Unexpected increases in global interest rates or a “risk off” shift in investor risk appetite could trigger currency depreciations with pass-through effects on domestic inflation. While regional markets have smoothly priced-in these developments, the possibility of such effects underscores the need to eschew policy or political actions that could erode investor confidence going forward.

Latam currencies have depreciated against the US dollar since the start of the year (chart 3). The Mexican peso and Brazilian real have depreciated by less than other currencies, reflecting the proactive monetary tightening cycles of their central banks. Elsewhere in the region, currencies have depreciated between 10–15 percent. The Peruvian sol has been under sustained pressure, which is evident in a longer-term perspective (chart 5).

Likewise, the equity market in Peru has shown the worst performance in the region (chart 4), reflecting protracted uncertainty surrounding the outcome of the presidential election and the interregnum that followed. Recent potential expropriation threats with respect to the Camisea gas project are unlikely to assuage investor concerns. Argentine and Mexican equity markets, in contrast, have performed strongly in the year to date.

Bond markets reacted strongly to the onset of the pandemic but have slowly recovered. 10-year CDS spreads, which spiked higher in March 2020, have gradually fallen over the past 18 months. However, they remain above the compressed levels prevailing prior to the pandemic. Increases in spreads on Brazilian, Colombian and Peruvian assets since the start of the year reflect a range of considerations, including political uncertainties.

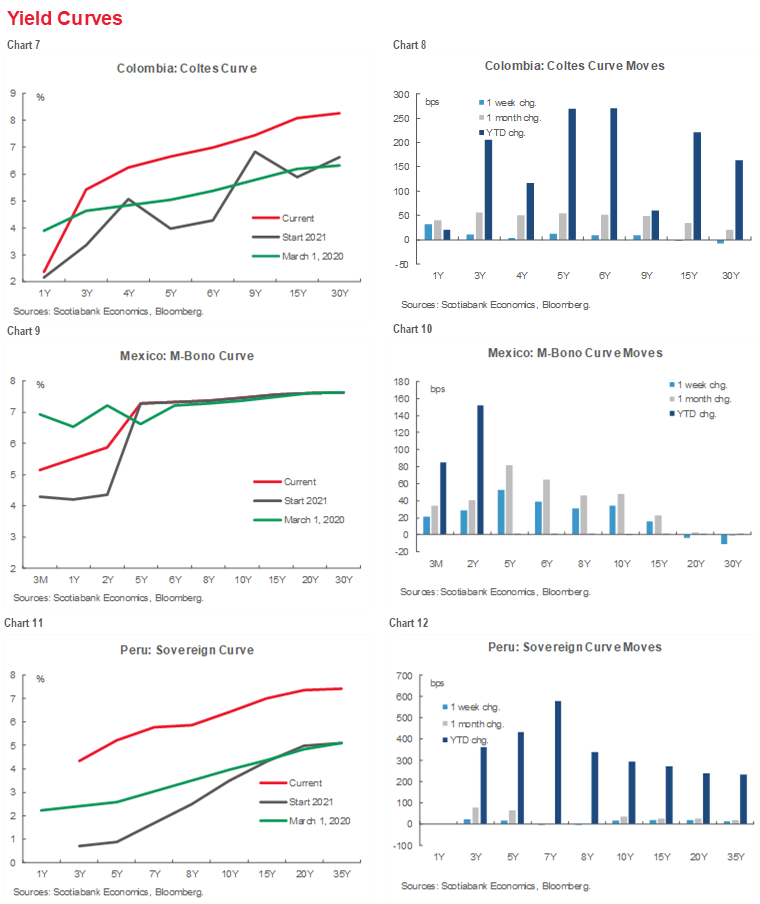

YIELD CURVE CHARTS

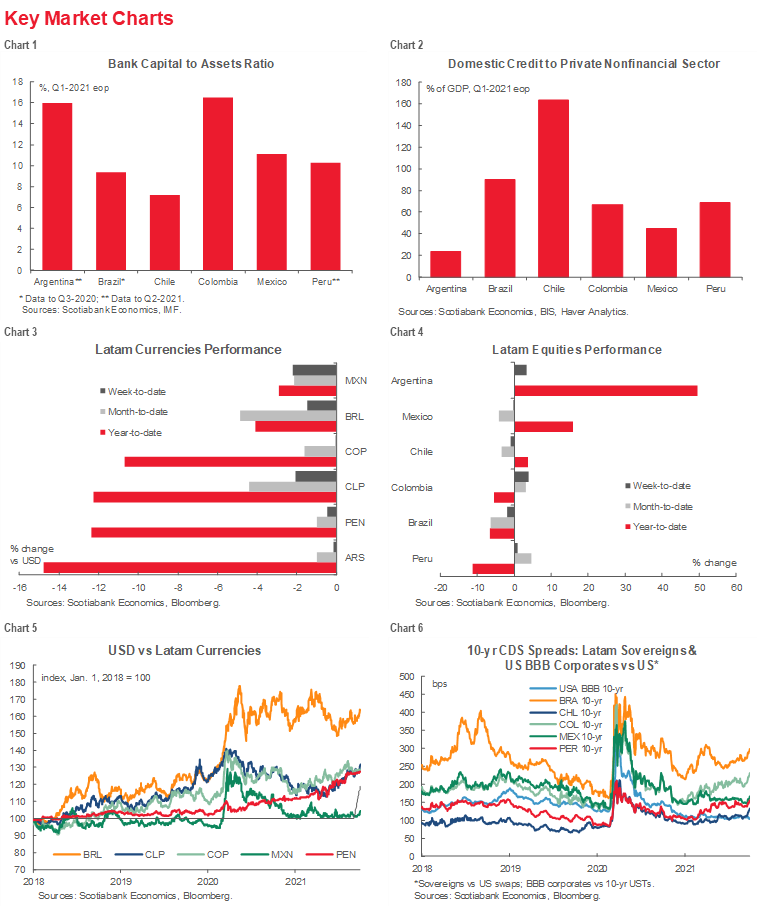

Sovereign yield curves have shifted up more or less uniformly across the maturity spectrum in most Latam countries since the start of the year (charts 1–12). Argentina, which has seen a marked steepening at the short end of the curve, and Mexico, which has a yield curve firmly anchored over the medium- and long-end, are exceptions.

KEY COVID-19 CHARTS

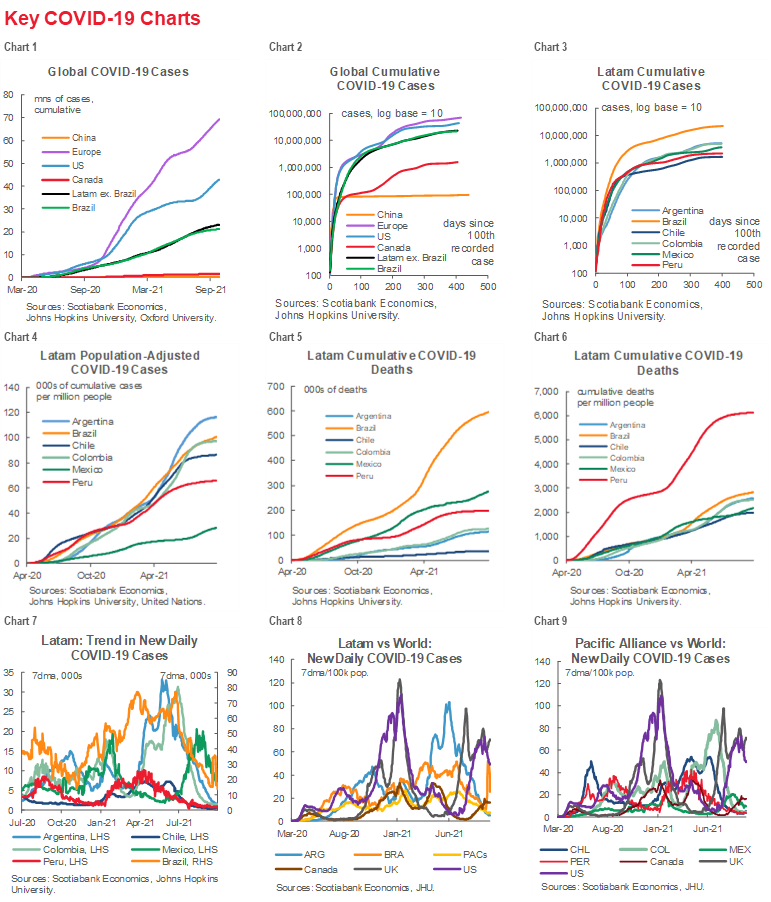

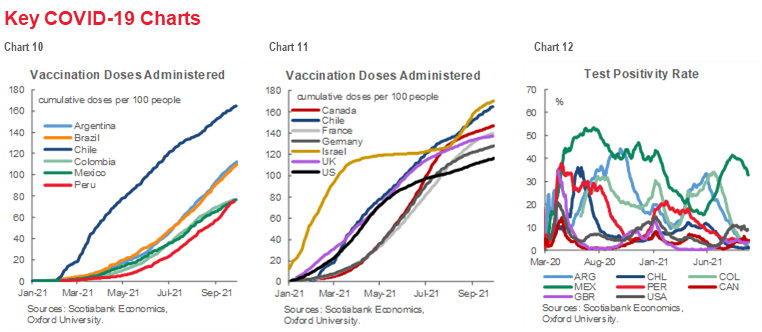

Economic recovery remains dependent on the course of the pandemic (charts 1–12). Chile’s high vaccination rate should provide effective protection against additional pandemic shocks, while the recent decline in the test positivity rate in Mexico is a much welcome development.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.