- Financial markets around the globe continue to be buffeted by turbulence.

- Further commodity price shocks or additional supply-side disruptions, combined with US dollar appreciation could create strong headwinds going forward. But thus far, at least, there is little indication that high volatility is spilling over to growth prospects.

- In this respect, for Latam economies moving from recovery to expansion, the current conjuncture could be summed up as “so far, so good.”

Global financial markets continue to be subject to increased volatility as markets price-in higher inflation and the increase in advanced country interest rates that must ineluctably follow. To this point, however, there has been little sign of contagion from asset markets to the “real” economy (output and demand). That is probably as expected given the “orderly” adjustment process—or at least absence of a gut-wrenching dégringolade like March 2020 or October 2008—thus far. That said, the effects of US dollar appreciation on Latam economies, as investor risk appetite shifts, should be monitored closely. And further commodity price or supply chain shocks that propagate still higher inflation would clearly be worrisome. But, for now, the economic conjuncture can be summed up as “so far, so good.”

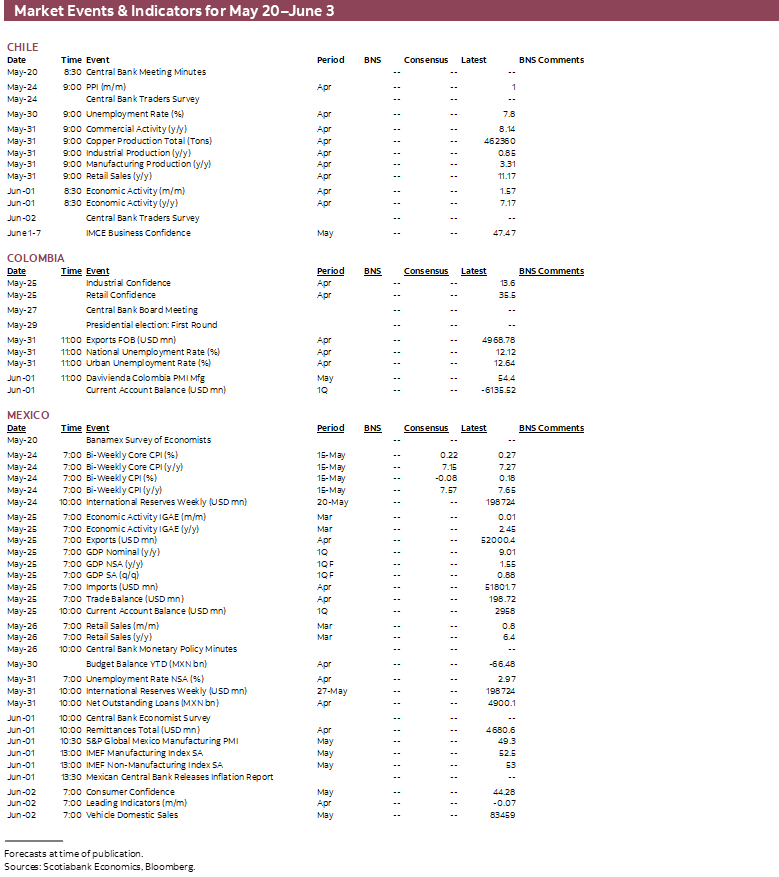

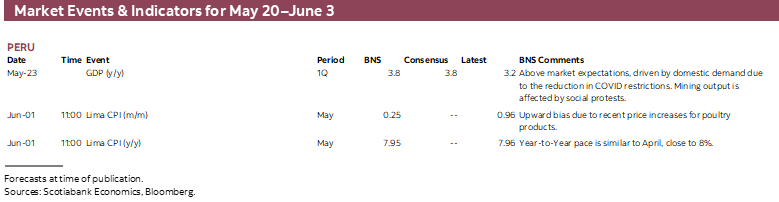

KEY ECONOMIC CHARTS

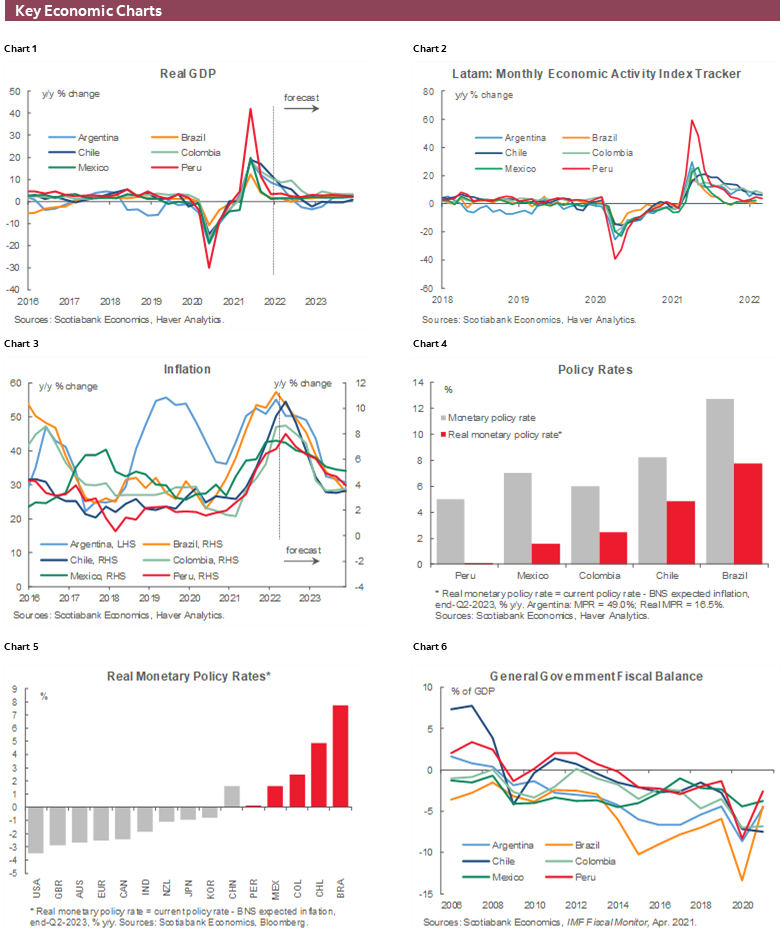

For now, Latam economies continue to recover from the pandemic-induced collapse in output, with the region’s economies on track to return to pre-COVID-19 growth paths (chart 1). In Chile, the transition to long-run growth may entail a technical recession, reflecting the remarkably vigorous bounce-back in 2021, but elsewhere in the region recession risks are low. Nevertheless, as noted above, it will be important to watch monthly activity indicators (chart 2) for signs of incipient weakness.

The biggest risk to the outlook is inflation, which has risen steadily across the region (chart 3). Latam central banks have tightened monetary conditions, raising key policy rates (chart 4) to keep inflation expectations firmly anchored to inflation-targeting ranges. In this respect, the region’s central banks have led most of their international peers in terms of generating positive real policy rates (chart 5); they have certainly been proactive as compared to advanced economy counterparts.

Economic recovery has led to improvement in fiscal balances (chart 6), as growth has raised GDP, while the extraordinary support provided throughout the pandemic has been scaled back. A return to fiscal targets consistent with long-term fiscal sustainability would help address investors’ concerns. Doing so would also bring down gross debt as a share of GDP (chart 7) as well as external debt as a share of GDP (chart 8). And fiscal probity would help contain burgeoning current account deficits (chart 9), though there is no automatic adjustment process between the two, and bolster external resilience. Going forward, while there is no immediate cause for concern, large current account deficits in Colombia, Chile, and Peru warrant monitoring, along with external reserves (chart 10), for signs of deterioration.

KEY MARKETS CHARTS

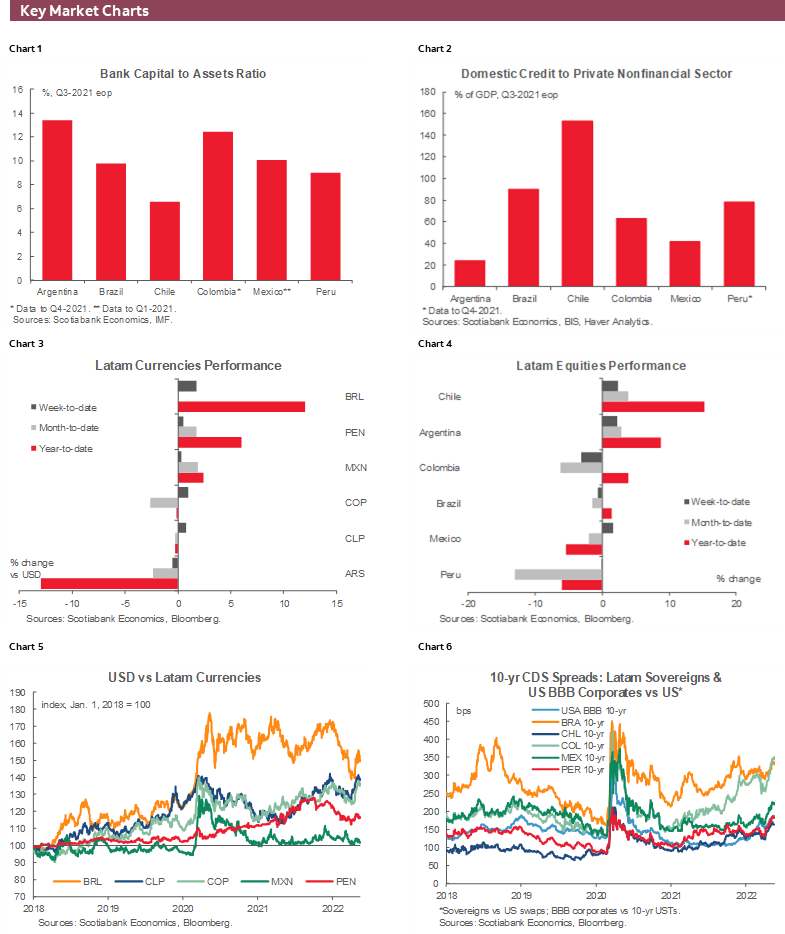

Financial markets in the Latam region have not been immune to the volatility affecting advanced economy markets. Despite the enormous uncertainty that clouds the near-term outlook, however, most markets have performed reasonably well. Currencies which had appreciated vis-à-vis the US dollar through the first couple of months have retreated somewhat in the wake of Russia’s invasion of Ukraine and heightened geopolitical risks (chart 3). The currencies of Brazil, Peru, and Mexico are all up on the dollar since the start of 2022; other regional currencies have depreciated. Similarly, the strong performance of regional equity markets earlier in the year is now more mixed. While most markets are still up on the year, Mexican and Peruvian markets have fallen back. In part, these markets may be affected by uncertainty with respect to investment climate; a factor that is also visible in a longer-term perspective on currency markets (chart 5) in the case of Peru. At the same time, increased economic risks associated with higher inflation may be contributing to a widening of CDS spreads on regional sovereign bonds (chart 6).

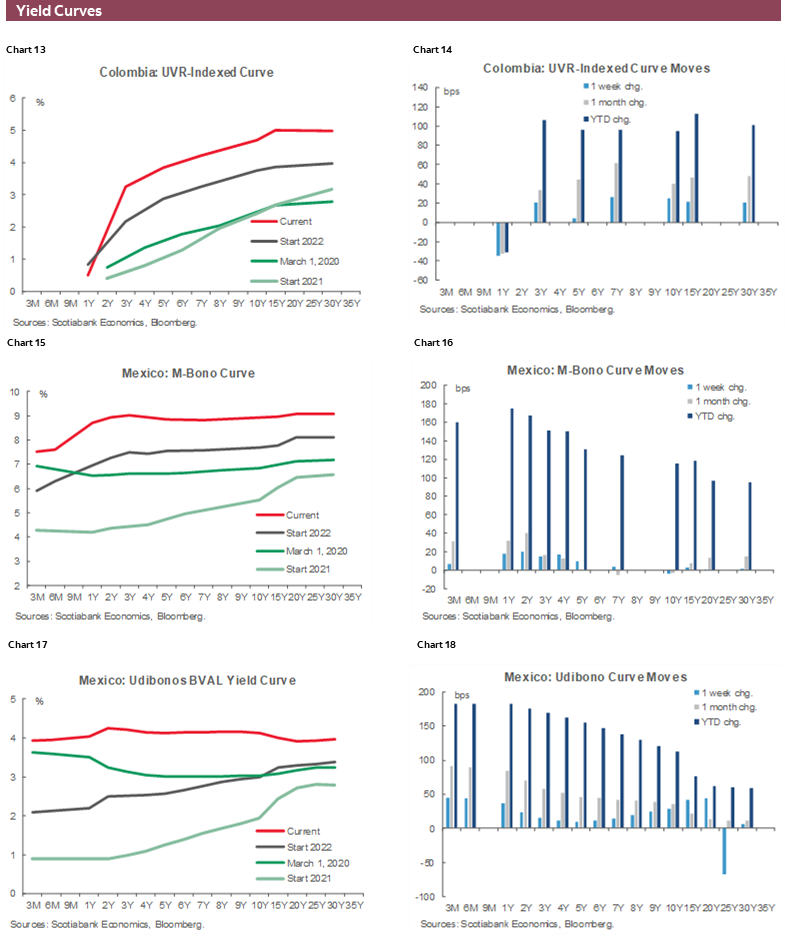

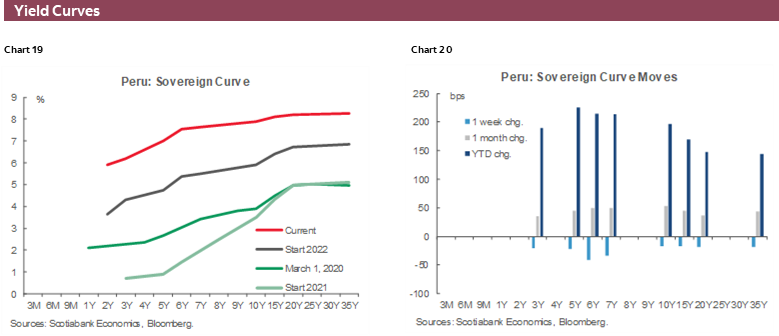

YIELD CURVE CHARTS

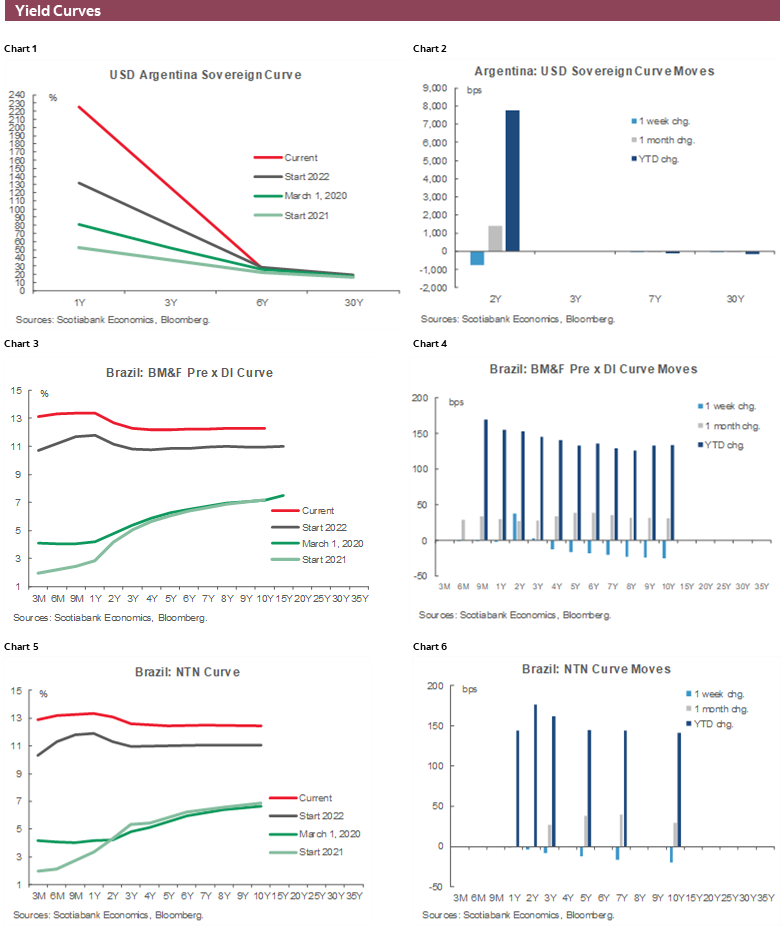

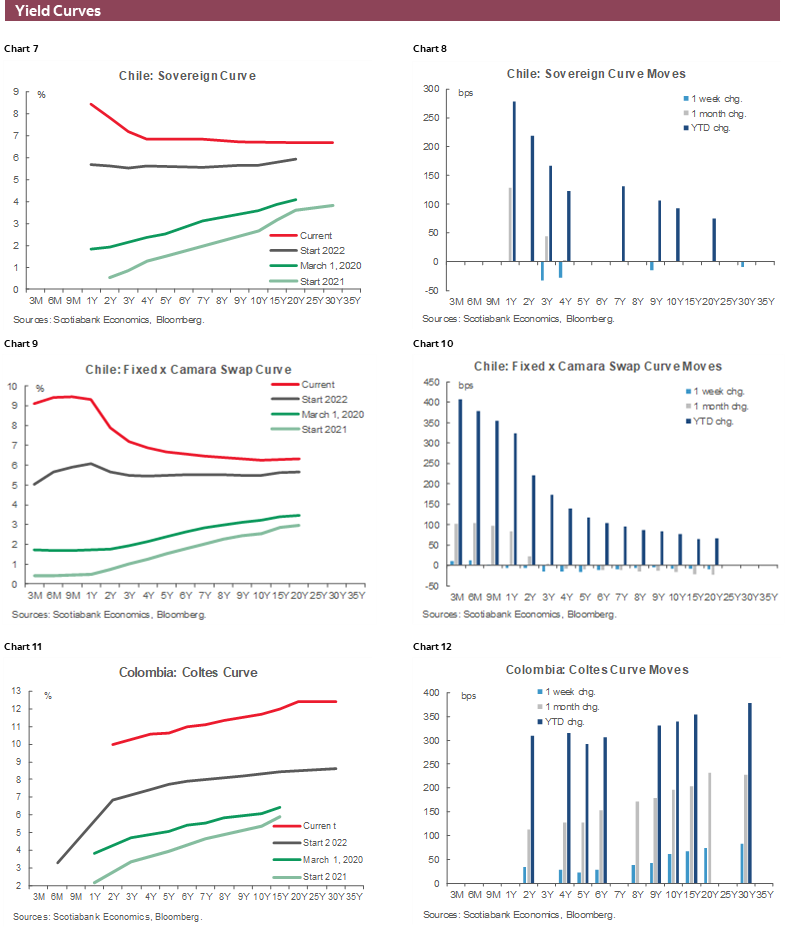

Yield curves across the Latam region are now largely inverted or flat. Colombia and Peru are exceptions here. Given that inverted yield curves can be a signal of a possible recession—though not a foolproof one—increased attention may be put on these indicators in the weeks and months ahead.

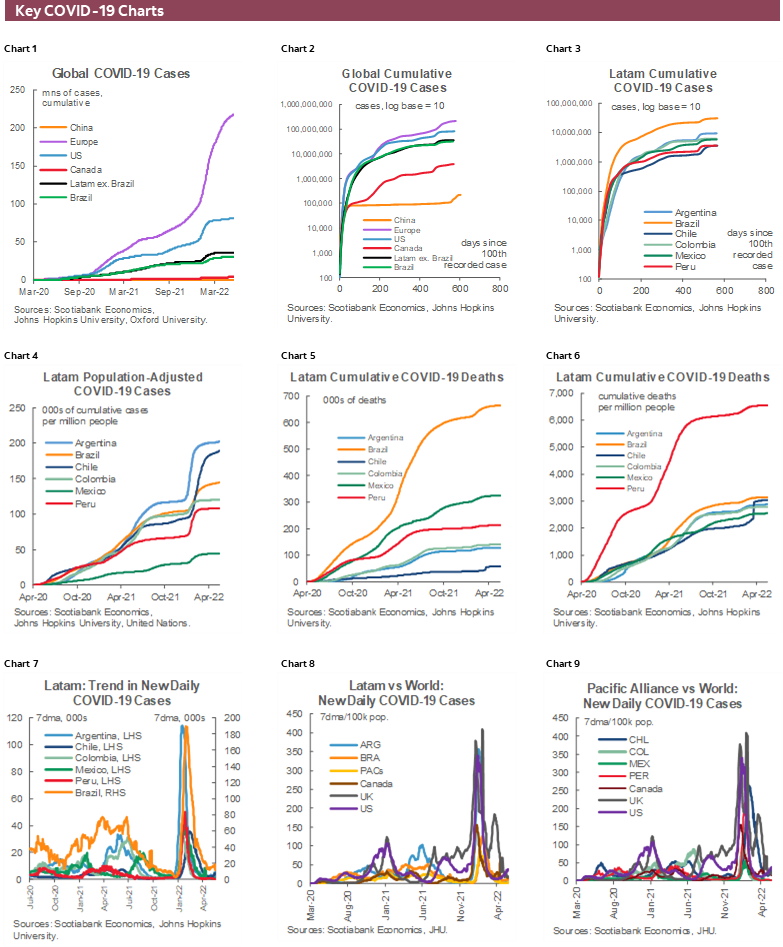

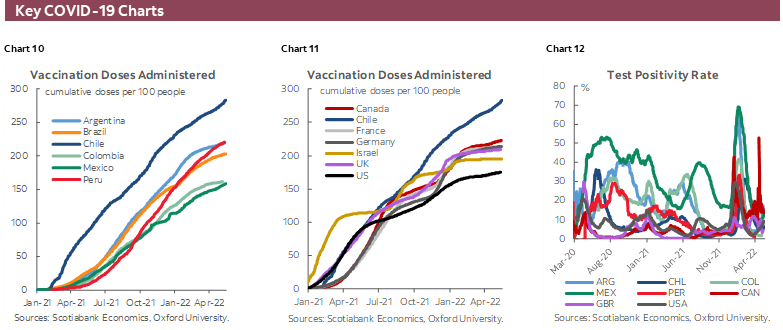

COVID-19 CHARTS

While much of the world seems to be operating “as if” the pandemic is past, the situation in China is a reminder that, while we may be through with COVID-19, it may not be finished with us. Rising caseloads in many countries highlight the possibility of another wave, with the potential economic implications that could entail. Key indicators are provided in charts 1–12.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.