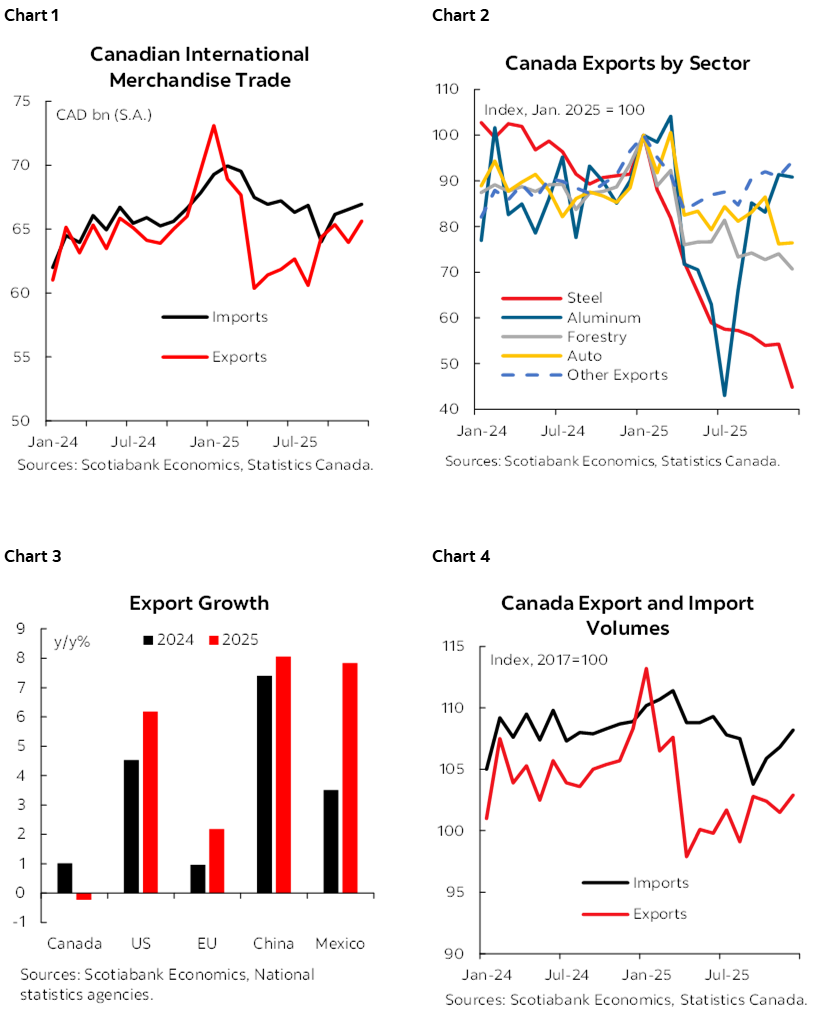

- Canada’s goods exports rose 2.6% in December and imports increased 0.6% (chart 1)—resulting in a deficit of $1.3 bn for the month. As has been the case for several months, unwrought gold was the main driver in changes on the export side—though higher exports of aircraft and other transportation equipment also contributed to the monthly rise. Gold imports also drove much of the rise in imports in the month, along with increased imports of motor vehicles and parts.

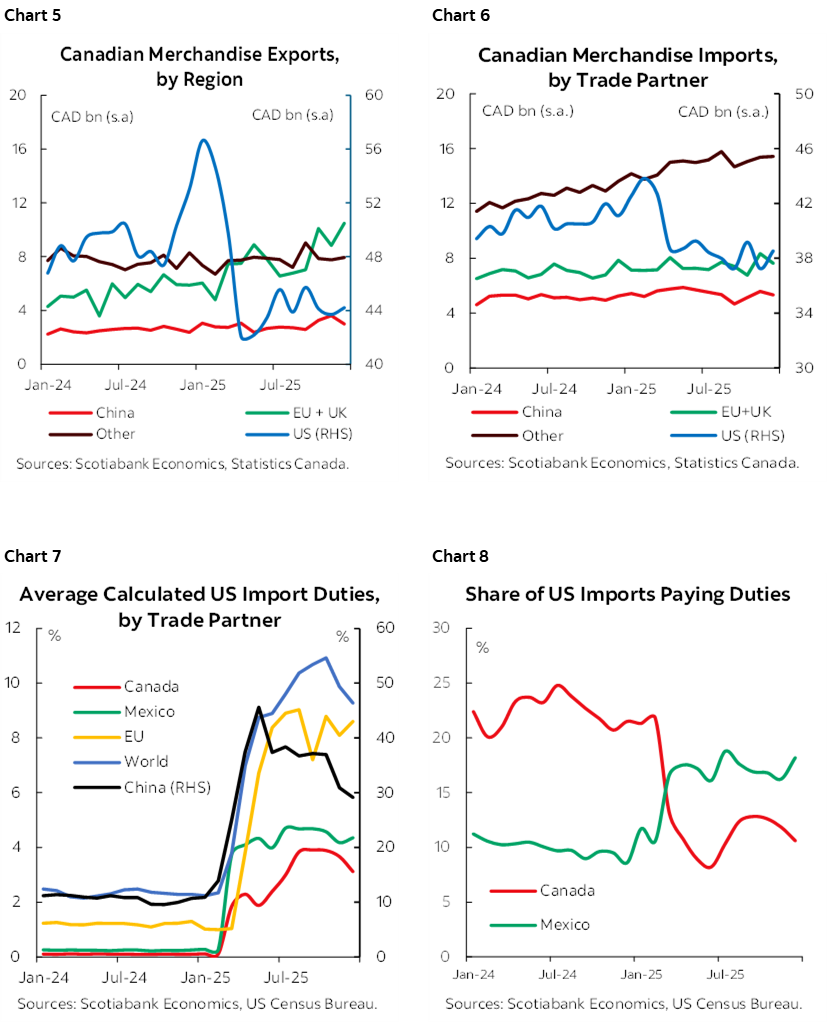

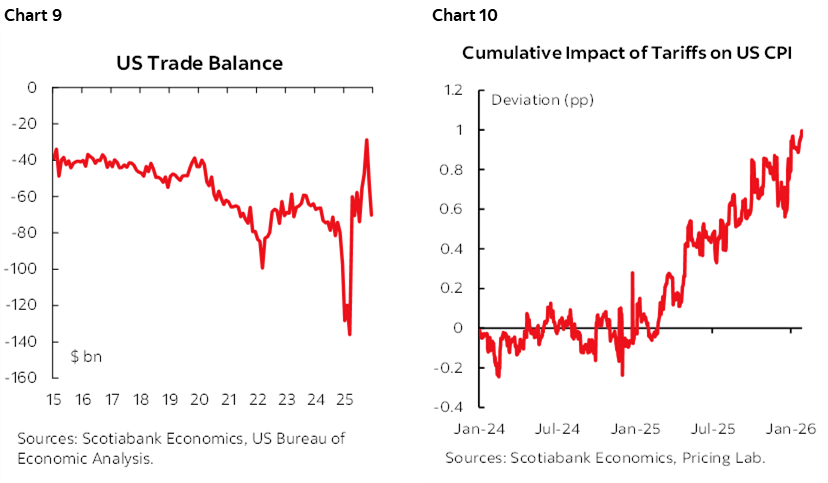

- Looking at 2025 as a whole, nominal Canadian goods exports were down 0.2%, as significant increases in gold exports were not enough to offset declines in most other product categories (chart 2), notably steel (-31%), aluminum (-7%), forestry (-10%), and motor vehicles and parts (-3%). This was weaker than many other countries (chart 3).

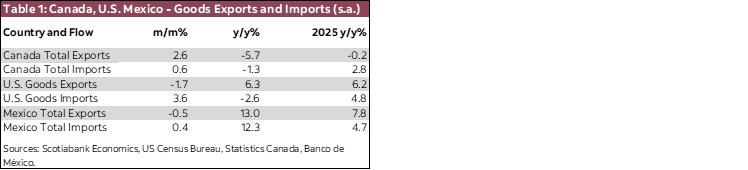

- Trade volumes tell a more negative story. After adjusting for prices, goods exports were down 2% on the year and imports were roughly flat (chart 4). As a result, trade is expected to have dragged on overall GDP growth for 2025. However, Q4 export volumes were 2.1% stronger than Q3, with imports up only 0.3%. This is a stronger contribution to growth than we assumed in our January economic outlook. We expect the drag from trade to continue to gradually decline though 2027.

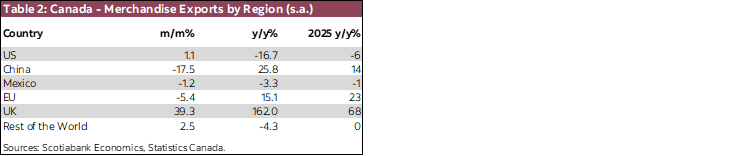

- The share of Canadian exports bound for the U.S. declined from 76% in 2024 to 72% in 2025 and is trending lower. This has been driven by a decline in exports to the U.S. and increasing exports to other regions—mainly Europe (chart 5). In December, exports to the U.S. rose 1.1% m/m but were down 16.7% y/y. Exports to other countries rose 5.8% m/m and were 30% higher y/y—though much of this has been driven by elevated overseas exports of gold. A similar dynamic is playing out on the import side (chart 6), as the share of Canadian imports from the U.S. fell from 62% in 2024 to 59% in 2025.

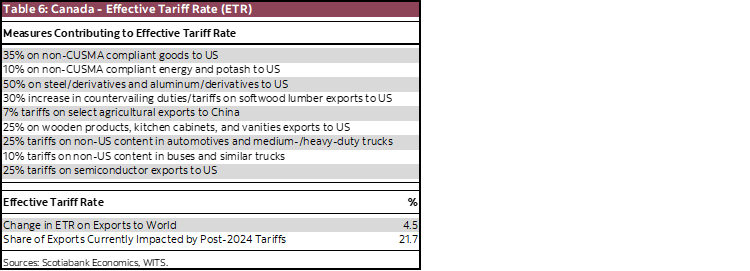

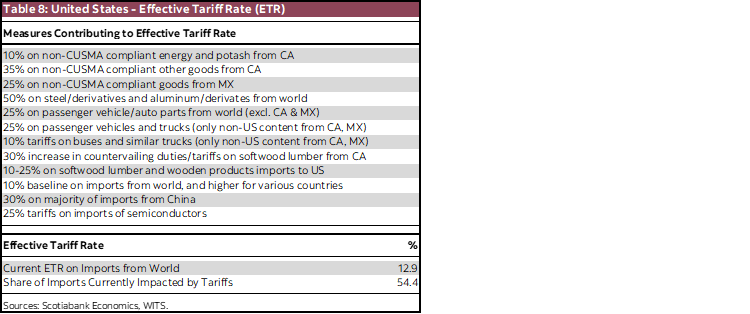

- Canada continues to benefit from a (relatively) low effective tariff rate on exports to the U.S. 6.3% is our current estimate (based on pre-tariff trade flows), thanks to most of our trade continuing on a tariff-free basis under CUSMA. The best estimate of the average actual duties paid on U.S. imports from Canada has fallen in recent months, dropping from 3.9% in September to 3.1% in December (chart 7). The proportion of Canadian goods imported into the U.S. facing tariffs has settled around 10% (chart 8).

- The U.S. trade deficit returned to its pre-tariff level in December (chart 9). U.S. trade saw significant volatility in 2025, with its trade deficit spiking early in the year due to high imports driven by tariff-front-running, then reaching its smallest level since 2009 in October, before normalizing at the end of the year.

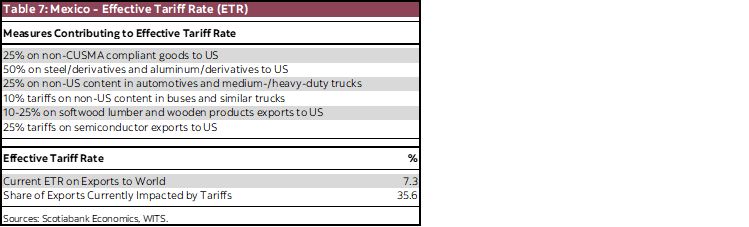

- U.S. trade flows have seen compositional changes. Comparing 2025 to 2024, U.S. imports were significantly lower from China (-29%) and Canada (-7%), but higher from the EU (+5%), Mexico (+6%), and the rest of the world (+19%).

- The U.S. import tariffs continue to create inflationary pressures in that country, with the latest estimate of the cumulative impact of the tariffs on U.S. CPI reaching a full percentage point (chart 10)—clouding the outlook for U.S. interest rate cuts.

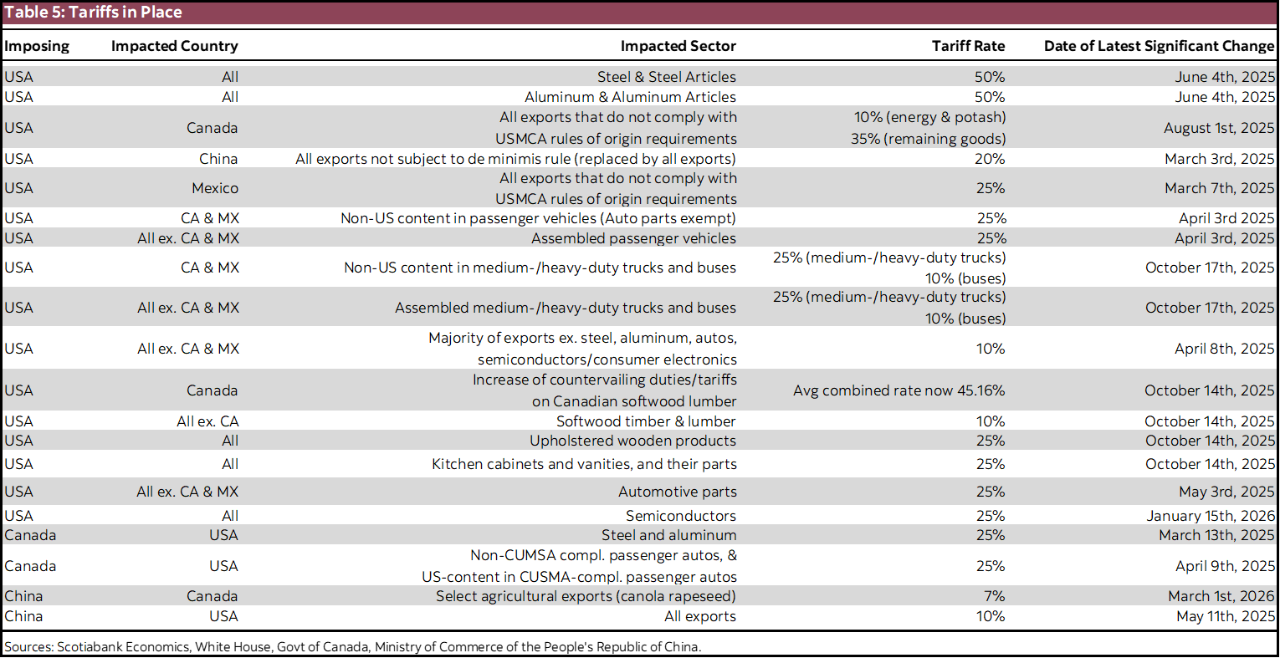

- With the U.S. Supreme Court expected to rule on the legality of the IEEPA tariffs soon, there could be renewed turbulence in the ongoing U.S. global trade war. If these tariffs are struck down, these could be replaced under a new mechanism—which would likely again be challenged, leading to renewed uncertainty. For Canada, the sectoral tariffs are by far the most impactful, and will continue to weigh on the Canadian economy as long as they remain in place.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.