- Geopolitical tensions in the Middle East are a stark reminder that global fragmentation threatens not only stability but also the prospects for an orderly energy transition and societal wellbeing.

- At the heart of this challenge lies energy security. As global systems grow more complex and alternatives scale, energy resilience is becoming inseparable from economic resilience.

- Deepening global imbalances are impossible to ignore. Growing gaps between supply and demand, ambition and investment, generation and infrastructure, and availability and affordability signal a volatile path ahead.

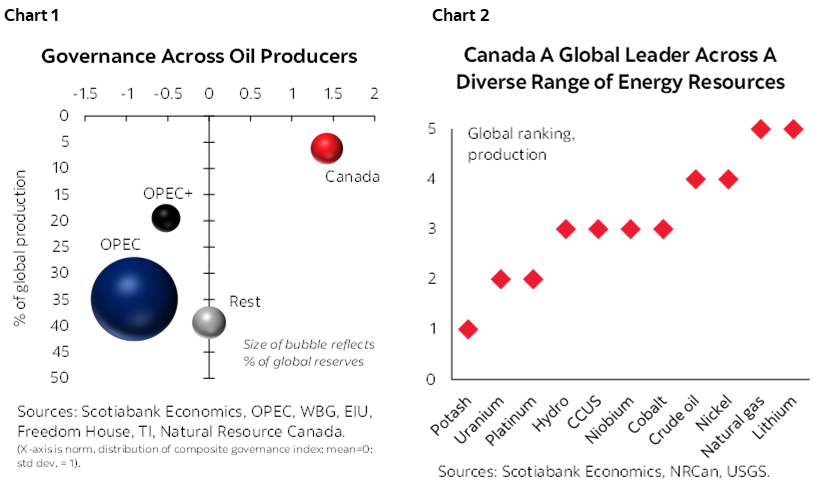

- Governance deficits among key resource players are compounding these risks. Nearly half of the world’s oil is produced in OPEC+ (chart 1). Over a third of natural gas comes from the Middle East and Russia. Nearly 75% of critical mineral processing occurs in just one country, and half of those essential to clean energy are intentionally restricted by export controls around the world.

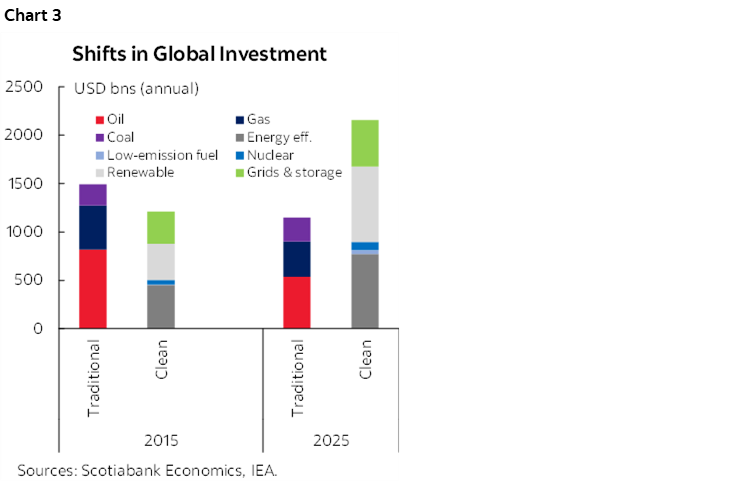

- Canada stands apart. It ranks high on the leaderboard across a wide range of energy resources, yet much of its potential remains untapped (chart 2). Years of underinvestment have eroded Canada’s competitiveness.

- A narrow window has opened. With strong governance and rich resource endowments, Canada is well-positioned to become a reliable, responsible energy superpower—serving both Canadians and trusted allies. But that promise must be earned.

- The federal government has a plan. It aims to unlock major new investments in the country’s most productive sectors. The ambition is bold—but success depends on restoring investor confidence and bringing business back to the table. That means addressing market failures—not by overriding markets, but by partnering with them to catalyze greater investment.

- The weaponization of energy is a tangible risk. The greatest policy failure may be the persistent reluctance to fully internalize this reality. Canada must act decisively—before the next disruption rewrites the rules.

HISTORY RHYMES

The 2022 Russian invasion of Ukraine shattered the illusion that energy affordability and climate goals could be pursued in isolation from geopolitical risk. Europe’s overreliance on a single supplier exposed deep vulnerabilities, while global energy markets reeled under price shocks. As Scotiabank Economics warned at the time (and again in 2023), geopolitical polarization is not a passing risk—it is a structural shift.

That warning has unfortunately proven prescient. Russia’s aggression continues into its fourth year, now complicated by tacit political support from the US. Instability in the Indo-Pacific persists, while escalating conflict in the Middle East is once again roiling markets. The human toll is immense. These dynamics are unfolding against a backdrop of an erratic policy landscape that has paralysed global investment activity.

The near- and long-term consequences of today’s ever-evolving global landscape may be deeply uncertain, but the urgency of bolstering energy security is not.

FADE THE DICHOTOMY

The once-polarizing divide between “alternative” and “conventional” energy is giving way to a more pragmatic consensus. The energy shock of 2022 exposed the fragility of global systems, prompting a shift toward an “all-of-the-above” strategy—one that prioritizes stability, affordability, and responsibility.

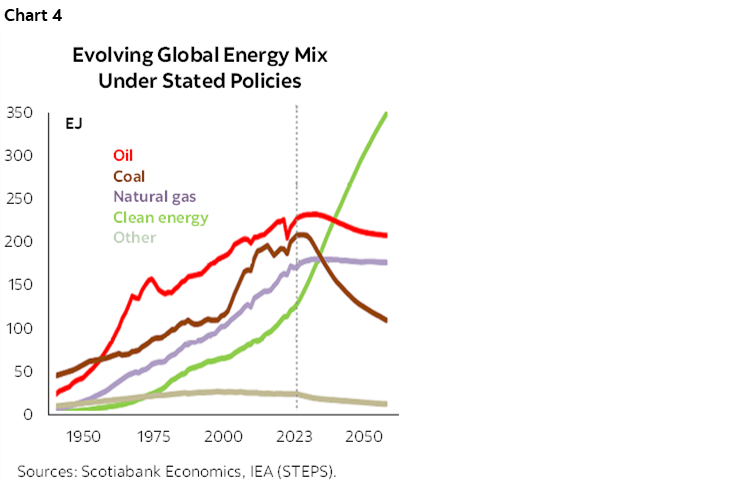

Clean energy is no longer niche. Major economic blocs like the EU and US embraced industrial strategies to accelerate clean energy investments—driven both by geopolitical and geoeconomic motives—as China cemented its lead. Technologies once considered nascent—such as solar, wind, and battery storage—are now being deployed at scale. According to the IEA, global investment in clean energy is expected to double that of fossil fuels in 2025 (chart 3).

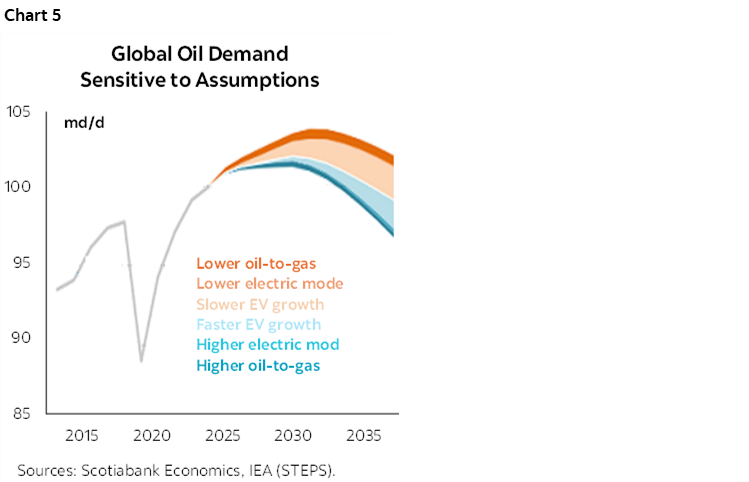

Still, conventional energy remains foundational. Fossil fuels accounted for roughly 80% of global energy demand and 60% of electricity generation last year. Under the IEA’s “current policy” path (i.e., Stated Policies), they are projected to remain a significant part of the mix over the next decade (chart 4). The sustainability conversation is shifting from energy type to production method—"abated” versus “unabated” is increasingly a key differentiator.

As systems grow more complex, so too do their vulnerabilities. Energy security is no longer just about barrels and pipelines. It includes complex critical mineral supply chains, sophisticated grid infrastructure, secure trade routes (and partners), and access to frontier technologies. Emerging demand drivers—such as AI data centers and climate-driven cooling appliances—are also placing nonlinear stress on electricity systems. Meeting this challenge requires not just more generation, but smarter, more resilient infrastructure and reliable supply chains.

Energy security is no longer just a utility concern—it is a prerequisite for sustained economic growth, industrial competitiveness, and social stability.

UNCERTAINTY IS THE NEW NORMAL

Forecasting the global energy outlook is increasingly fraught. In 2024, global energy demand rose by 2.2%—nearly a full percentage point above the historical average. Yet the IEA projects this will slow to just 0.5% annually over the next decade. But demand trajectories diverge sharply by source. Electricity demand is expected to grow at 3% annually through 2035, driven by electrification and digitization. In contrast, demand for conventional fuels may plateau—or decline—depending on the pace of clean energy deployment and efficiency gains according to the IEA.

But these projections rest on increasingly tenuous assumptions. The IEA’s scenarios—from current policies to net-zero pathways—reveal wide-ranging outcomes. Even in its current-policy scenario, the range of possible outcomes is significant. For instance, electricity demand in 2035 could exceed baseline forecasts by 5% in high-growth scenarios, depending on EV adoption, coal-to-gas switching, and appliance efficiency. Oil demand could be 2–3% lower—or 2–3% higher. LNG demand could swing from 4% below to 3% above baseline (chart 5). In high-demand cases, peak fossil fuel use could be delayed by years and occur at higher absolute levels—in the best-guess baseline before considering other policy settings.

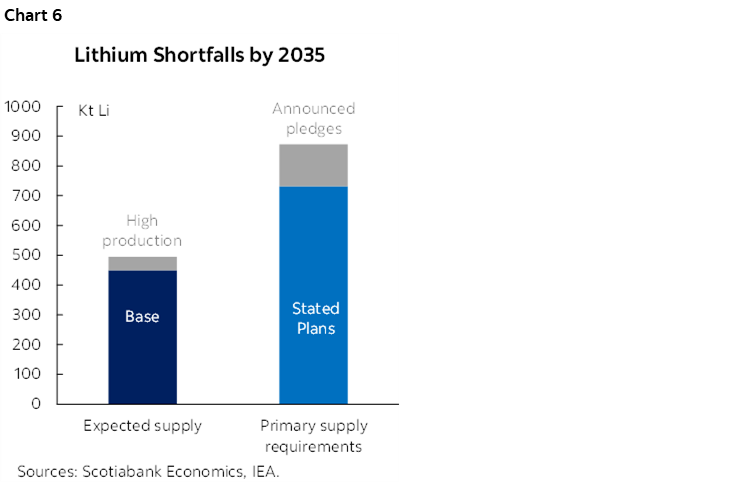

Structural mismatches are also widening—not just between supply and demand, but between ambition and investment, generation and infrastructure, extraction and production, availability and affordability, to name a few. Grid investment is lagging generation capacity. EV charging infrastructure is falling short of adoption targets. Critical mineral supply—including lithium, nickel, and rare earths—remains well below clean tech demand (chart 6). Systemic imbalances are exhaustively documented in the IEA’s annual tomes.

A weaker global economic outlook may temper near-term energy demand, but that is cold comfort. US policy volatility is distorting both short- and long-term demand signals. This is not merely a cyclical downturn but reflects deeper structural shifts as the world’s largest economy redefines its energy—and more broadly isolationist—agenda. The IEA’s October baseline is already outdated as US policy reversals have cast doubt on EV timelines and clean energy deployment.

This is not an environment that rewards complacency—especially not those that fail to internalize energy security risks.

POLARISATION IS PERMANENT

Geopolitical fragmentation is accelerating. Trade and investment are increasingly shaped by politics over efficiency. Energy systems lie at the heart of this risk.

The concentration of conventional fuel reserves remains a critical vulnerability. Almost 60% of global oil reserves are held by just four countries: Venezuela, Saudi Arabia, Iran and Iraq. Over 60% of natural gas reserves sit in the Middle East and Russia. On a production basis, the picture looks only marginally better. OPEC+ continues to shape oil supply, while new LNG capacity is clustered in a few Gulf states.

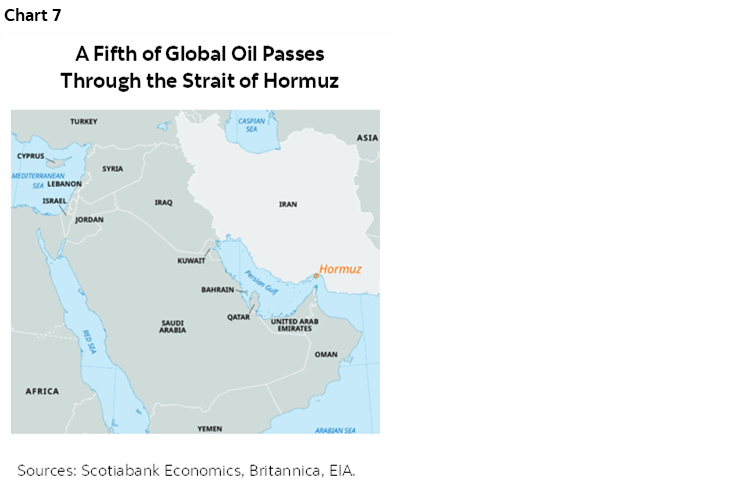

Rising instability in the Middle East has brought chokepoint risks into sharper focus. About 20% of global oil and LNG supplies transit the Strait of Hormuz, while the Strait of Malacca handles roughly 55% of global seaborne oil trade and over 10% of LNG shipments (chart 7). Given the volume of energy moving through these narrow, politically tense corridors—with limited alternatives— disruption could send shockwaves through global markets. This is largely considered a tail risk, but that tail is getting crowded by the day.

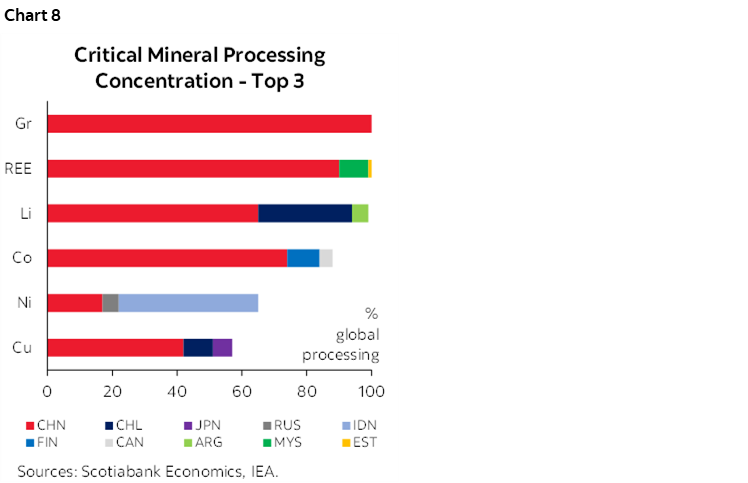

Clean energy supply chains are no less exposed. The three largest suppliers account for 70% of global supply of key critical mineral extraction, and more than two-thirds of cobalt, graphite, and rare earth output comes from a single country according to the IMF. Refining is even more concentrated: nearly all refined lithium, graphite, and rare earth elements come from just three processors. And China mostly holds the cards: it refines 19 of the 20 critical minerals tracked by the IEA and controls about 70% of global processing capacity—including over 80% of graphite and a near-monopoly in rare earth refining (chart 8). Concentration has only grown more entrenched since 2022, with few signs of easing.

Governance risk compounds these challenges. Nearly three-quarters of global oil reserves—and half of production—are in jurisdictions with governance scores one standard deviation below the global average according to our updated composite governance indicator (chart 1, front, see original publication for methodology). Natural gas and critical minerals display similar governance deficits. Over 80% of rare earths and 60% of cobalt come from high-risk jurisdictions, for example.

Meanwhile, the US—once the world’s swing producer—is becoming increasingly unpredictable. Shale output is constrained by capital discipline, low prices, and policy uncertainty. Institutional volatility is eroding investor confidence. Its energy trade balance, though still positive, is softening from recent highs. While forecasts suggest the US will remain a net energy exporter for the foreseeable future, compositional imbalances within its energy ecosystem expose underlying vulnerabilities. And beyond its conventional energy position, many speculate that recent territorial threats towards Canada and Greenland could stem from the nation’s limited reserves of critical minerals.

Economic fault lines between regions are also deepening. Developing Asia is heavily reliant on fossil fuel imports from Middle Eastern and Russian suppliers, a corridor set to deepen further. India—where per capita consumption is just one-tenth of US peers and roughly 10% of the population still lacks access to energy—plans to double coal production over the next decade to meet this demand. Together, India and China account for roughly two-thirds of global coal demand, even as China’s renewable capacity has surpassed its fossil fuel-based thermal generation.

The risk of energy weaponization is no longer hypothetical. Nearly half of all critical minerals essential to clean energy technologies are now subject to export restrictions according to the IEA. The chip shortage of 2022 exposed how vulnerable complex supply chains are to disruption. China’s tightening grip on rare earth exports—and signals that India might follow suit—offers a pointed reminder: supply shocks can now be deliberate, not just collateral.

CANADA’S ENERGY EDGE

Canada sits atop a geopolitical goldmine of diverse and strategic energy resources. It ranks third in global oil reserves and fourth in production, while it is the fifth largest producer of natural gas. It is the world’s third-largest producer of hydroelectricity and the second-largest of uranium—both key to low-emissions power. Wind energy comes in at a decent ninth, but with considerable untapped potential. Additionally, the country ranks in the top three for key critical mineral reserves such as nickel, cobalt, and rare earth elements. Canada also podiums on both current and planned carbon capture and storage (ccus) capacity. With this breadth of secure, low-emissions, and high-abatement potential energy assets, Canada is uniquely positioned to anchor global energy security.

There is a growing national consensus that Canada must lean into this advantage. Threats to economic security and even sovereignty from south of the border have shifted the domestic dialogue. Strong institutions, rule of law, (relative) fiscal discipline and financial stability uniquely position Canada as a trusted energy supplier in an increasingly fragmented world.

But its window is narrowing. Over a decade of underinvestment, policy uncertainty, and regulatory gridlock has weakened Canada's competitiveness. Capital has flowed elsewhere. Despite shifting sentiment at home, US policy volatility is casting a long shadow over investment decisions.

Canada must act decisively before the next crisis forces its hand.

THE PACE OF AMBITION

Canada’s new federal government has adopted a pro-growth agenda with the aim of becoming the fastest‑growing G7 economy. It would leverage its balance sheet—running annual capital-related deficits in the order of $50 bn (1.5–2% of GDP) to derisk private investment—mobilizing half a trillion in fresh outlays over five years. This would be broadly consistent with the 2% real GDP per capita “pace of ambition” Scotiabank urged earlier.

The federal government’s plan signals “urgency and determination”. Bill C-5 would streamline permitting, reduce regulatory friction, and prioritize projects of national interest. The framework embraces an expansive definition of energy security and provincial counterparts are sidling up. First Nations are central to this agenda, with dedicated funding and partnership models. Growing equity ownership opportunities are critical but do not replace constitutional rights. The “pace of ambition” must be matched with the “pace of trust”.

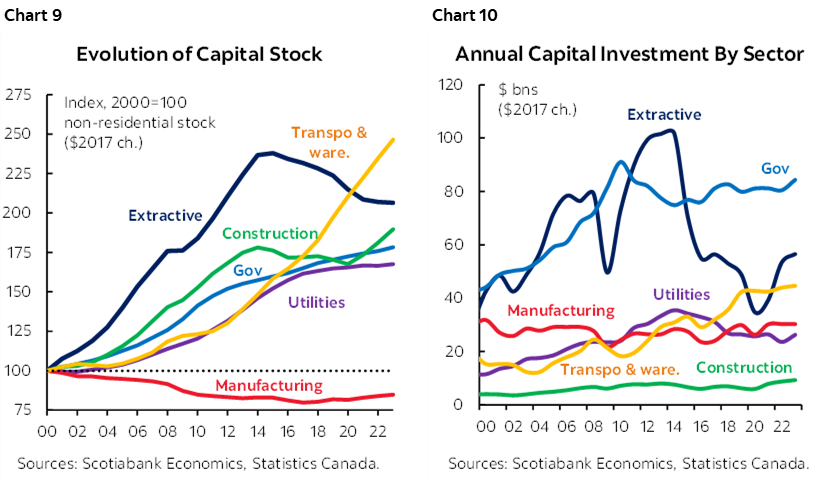

Meaningful results hinge on tapping the nation’s energy edge. The energy sector—defined broadly to include conventional and clean energy as well as related supply chains—accounts for over 10% of Canada’s GDP, while comprising almost 40% of its capital stock. But capital accumulation in the extractive sector has pulled back sharply since 2015, while investment in utilities has stalled over the past decade despite clear need (charts 9 & 10). The share of annual investment in the wider energy sector currently stands just shy of 25%. Promisingly, there is more than $580 bn in the project pipeline over the next decade according to Natural Resources Canada. At an average $50 bn annually, this could make material inroads towards the government’s growth goals. Not all will come to fruition, but this pre-dates recent policy momentum, talk of nation-building projects, and promises of hefty fiscal support.

But ultimately, markets must do the math in deciding where to put that incremental dollar.

HARNESSING MARKET FORCES

Success hinges on aligning market forces with national goals. C-5, coupled with the provision of risk capital, has the potential to significantly lower the cost of capital and hurdle rates for businesses. However, the federal government—and other orders of government—could go further to enhance Canada’s investment landscape.

Canada’s expanding array of clean investment tax incentives could benefit from greater coherence and accessibility. Over the past few years, the federal government has introduced more than $100 bn in targeted tax credits with the potential to unlock nearly half a trillion dollars in eligible investments over the next decade, according to the PBO. However, the rollout has been slow, and the complexity of the programs—particularly for smaller firms and some Indigenous partners—has drawn criticism. The upcoming federal tax review presents an opportunity to streamline these incentives and enhance their effectiveness. The government could, for example, improve the monetization of these tax credits, enabling firms to formally leverage their projected value to secure more favourable financing terms—something the US has pioneered.

The government should also take a sober look at its full policy suite to identify potential distortions to the efficient allocation of capital. The Parliamentary Budget Officer (PBO) is the latest to point to the possibility that sector-specific emissions caps could pose de facto emissions caps in the oil and gas sector. Those calculations hinge on wide-ranging assumptions—many highly unpredictable, as noted earlier—but they unnecessarily risk distorting investment signals. A neutral, sector-agnostic framework would improve coherence and preserve market efficiency in allocating capital and reducing emissions.

None of this is an abdication of climate goals. The industrial carbon pricing system—while not perfect—remains an effective market-based tool for reducing emissions. The pace and stringency of its implementation are democratic decisions, but governments can reduce uncertainty by using instruments like carbon contracts for difference, which offer the long-term clarity needed to attract private investment. The federal government has already begun experimenting with these guarantee-type mechanisms and will likely need to further expand their use to complement other more traditional financing tools. It also provides a credible signal to international partners—particularly those in regions like the EU implementing carbon border adjustment mechanisms—that Canada is serious about decarbonization, thereby supporting stronger trade relations and reducing the risk of future tariff-related frictions.

The federal government could also play a stronger role in catalyzing greater policy coordination across jurisdictions within the country to reduce investor uncertainty. Harmonizing industrial carbon pricing across provinces—potentially with fiscal incentives to encourage alignment—could improve cost-effectiveness while respecting provincial autonomy. The Canadian Climate Institute has underscored that aligning large-emitter trading systems across provinces could improve competitiveness and reduce emissions at lower cost. More broadly, companies often cite the complexity of “policy stacking” that puts yet more sand in the gears.

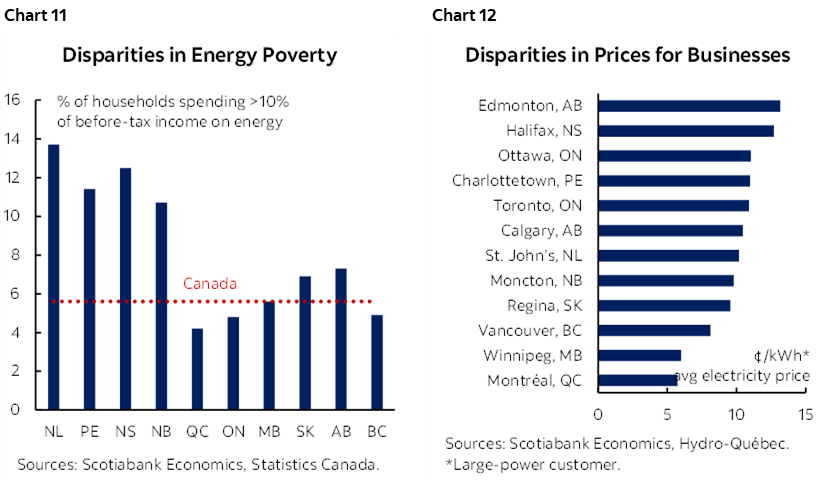

At the same time, federal policies must recognize the deep regional diversity in Canada’s energy landscape. Disparities in energy costs for households and businesses are shaped both by natural resource endowments and provincial policy choices. For example, energy poverty affects 5.6% of households nationally, but rises to over 13% in parts of Atlantic Canada, according to Statistics Canada (chart 11). Similarly, electricity prices for businesses vary widely—with Quebec offering some of the lowest industrial rates in North America, while Alberta and Ontario face significantly higher costs (chart 12). These differences fuel regional tensions, shape public sentiment, and increase political risk around national energy and climate policies. Federal programs and regulations that account for these regional realities can help reduce friction and build broader support for the energy transition.

Internationally, Canada can play a more strategic role in critical minerals. Even with rich endowments, no country can go it alone. Coordinated trade, infrastructure, and investment strategies are essential to long-term supply chain leadership. The recently-announced G7 Critical Minerals Action Plan is a step in the right direction.

These suggestions are not exhaustive, but they push the bar higher by ensuring governments are willing to correct market failures—not by overriding markets—but by working with them to responsibly unlock even higher levels of investment.

RESPONSIBLE AND RELIABLE ENERGY. PERIOD.

In this new era, energy policy must be grounded in realism, resilience, and diversification. Governments and investors are navigating a landscape shaped by the convergence of geopolitics, heightened security risks, climate imperatives, and rapid technological change. The path forward is not linear—but it is navigable with foresight, policy flexibility, and strategic international cooperation.

Canada is uniquely positioned to lead. By anchoring its energy strategy in long-term economic resilience and domestic well-being—while projecting itself globally as a secure, reliable, and responsible energy superpower—Canada can shape the future of energy on its own terms.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.