THE CONTINENT’S ECONOMIC PERFORMANCE OVER THE LAST THIRTY YEARS HAS OUTPACED OTHER REGIONS, AND DEEP INTERCONNECTION IS A KEY REASON WHY

- North America has grown faster than any region globally save Southeast Asia over the last thirty years, and has contributed twice as much to global GDP growth as Europe in this time.

- Regional integration has been core to this economic success. Strong, open ties have deepened trade and capital flows, supported significant supply chain specialization, and is responsible for 17M jobs across the three countries.

- Countless studies from academic, think tanks and multilateral bodies show that interconnection has been an economic positive for wage growth, output, productivity and margins. Connecting automotive production with Mexico, for example, has likely supported US and Canadian manufacturing by preventing entire supply chains from departing to lower-cost Asian markets.

- Far from being substitutes, Canadian and Mexican participation mutually supports both nations directly (through trade/commercial ties, and helping balance compliance with rules of origin requirements and cost competitiveness) and indirectly (mutual strengthening of largest export market).

- Losing this interconnectivity would be an incredibly costly own goal. De-integration could see more jobs lost than created, and unbundling supply chains would almost certainly lead to inflation, decreased competitiveness and structurally lower economic growth. US consumers and small businesses, in particular, would lose out. Bluntly, there is no better future on the other side of autarky, save for global firms competing with North American companies.

- If the USMCA is renegotiated, remaining a three-party agreement should be the fundamental priority for all. It would be in Canada’s (and Mexico’s) national interests to advocate for this.

- The future of the USMCA should not be in doubt, given its role in supporting North American growth since the signing of NAFTA. If this fails, the three countries will almost certainly end up worse off.

A WONDER OF THE ECONOMIC WORLD

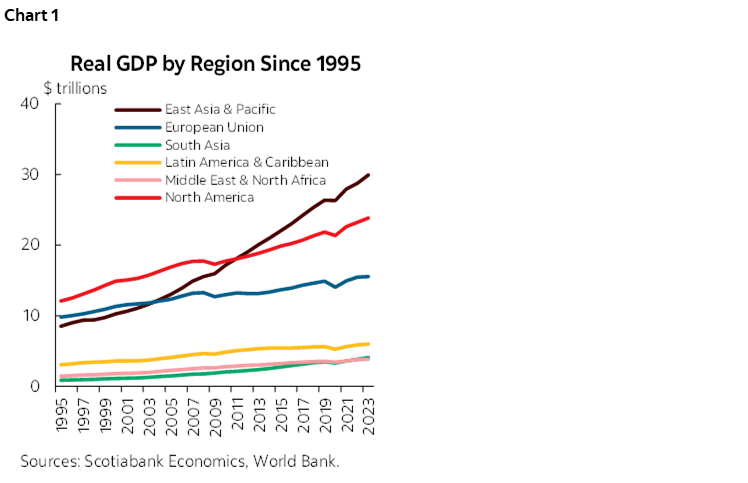

North America’s economic performance over the last three decades has been the envy of the world. The three economies represent the second largest economic bloc globally, accounting for only 6% of the global population, but roughly 30% of global GDP. Since 1995, North America has experienced greater economic growth than any other region globally, save East Asia (chart 1). The continent was responsible for roughly 22% of real global GDP growth over this period, while Europe provided only 11% over the same timeframe.

High performance results from a growth recipe that creates a whole greater than its ingredients. As a regional trading bloc, North America’s advantages are enviable. Canada, the US and Mexico account for 15% of global lithium reserves, 15% of oil reserves, 12% of global arable agricultural land, and substantial quantities of fresh water. Human capital is also abundant, and highly complementary. Low-cost labour in Mexico enables for the distribution of supply chains across borders, and Canadian know-how around resource production provides relatively cheaper inputs for American manufacturers. The US, in turn, has leveraged these advantages to further specialization, leading to significant innovation and productivity growth, all while each benefits from tariff-free access to supply chain partners and consumers.

This economic potential has translated into strength captured in three broad components, each contributing to a virtuous cycle of growth: Trade linkages, cross-border supply chains, and complementary investment flows. Trade flows offer lower-cost goods and robust markets for states and provinces in all three countries. Cross-border supply chains have strengthened competitiveness for key sectors like automotive, and likely kept jobs in Canada and the US that would have otherwise departed. Capital flows allow each country’s firms to invest in the others, creating further jobs and directing capital to fuel productivity and wealth creation. These self-reinforcing interconnections make all three countries richer, and any attempts to shrink it should be understood as a grievous act of self-harm for all of the continent’s nearly 600M residents.

TRADE HAS BENEFITTED ALL THREE COUNTRIES

Trade ties have become foundational to North American regions and sectors. Total trilateral trade between Canada, Mexico and the US was $1.9T CAD in 2023 (chart 2 and 3). Estimates of NAFTA’s impacts on trade flows find that the removal of trade barriers was potentially responsible for roughly doubling trade above pre-agreement levels. Despite the uncertainty associated with renegotiating NAFTA, the average annual growth rates in exports between the three countries increased following the ratification of the USMCA (from 4.8% to 5.8%). This exchange is critically important for all three economies. CAN-MEX-US exports to each other accounted for 27% of Mexican GDP, 24% of Canadian GDP and 3% of US GDP in 2023. Although these shares have not significantly changed over time, the total value of trade has continued to grow in absolute terms, indicating all three countries are growing alongside one another. Trade in goods also support millions of jobs. Trade between USMCA countries was reportedly responsible for 17M jobs in 2023, with the majority of these roles created in the US. Nearly 8 million US roles were supported by trade with Canada alone, with 2.6M Canadian jobs supported through goods headed in the other direction.

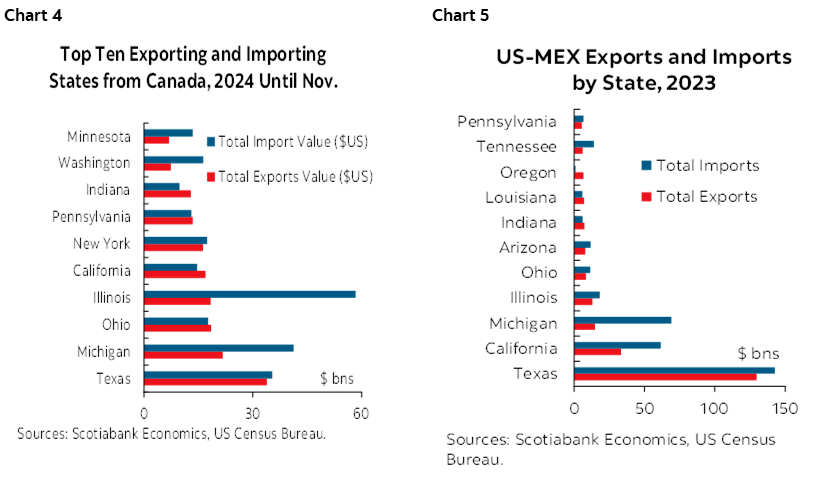

Industries and regions across the US rely heavily on Canadian and Mexican markets, beyond just border states. 49% of total US GDP is generated from states on the border with Canada and Mexico, many of whom benefit from deep interconnection with neighbouring countries. Roughly half of all US states sell at least one third of their goods exports into Mexican and Canadian markets. Canada alone is the top export market for 34 US states, and the top country of origin for imports for 24 states. A 2019 review of the agreement identified that these trade flows disproportionately originate from US small-to-medium sized businesses, who account for the majority of exports to Canada and Mexico, given the (historic) lack of tariffs relative to international markets. States and firms that benefit most are typically part of cross-border supply chains, including in energy, automotive, electronics and machinery manufacturing, although many non-border states rely on Canada and Mexico for a significant share of their overall imports and exports as well (chart 4 and 5).

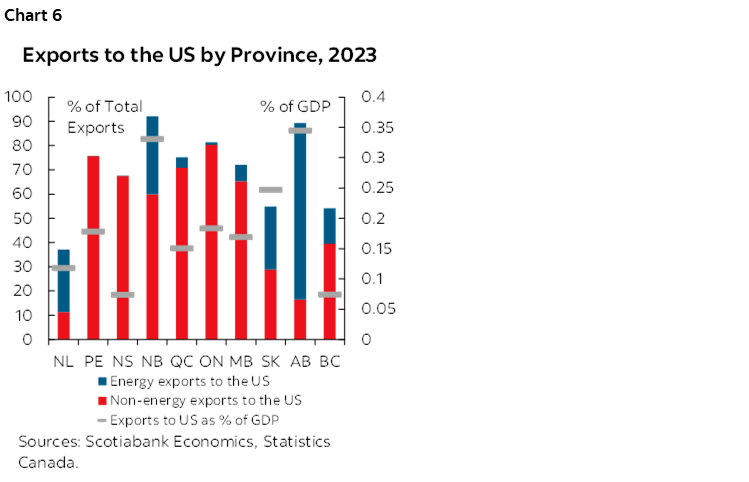

Canadian provinces and Mexican states rely even more heavily on the US. The US is the primary export destination for over half of all goods for nine out of ten Canadian provinces. US exports are responsible for 7%–34% of GDP across each province, with some of Canada’s largest provinces (Ontario, Alberta, Quebec and Saskatchewan) benefitting most (chart 6). Similar to US states, the presence of cross-border supply chains in energy and automotive are key determinants, but the US also represents critical markets for Canadian exports of aluminum, lumber and potash. Mexican states with the highest export volumes into the US are primarily border states (Baja California, Chihuahua, Nuevo Leon), although Mexico City tops the list, accounting for 19% of overall exports. Mexican states who count for a large share of total exports to the US have established industries in either automotive/parts manufacturing or electronics/machinery parts manufacturing, which constitute the bulk of export flows.

LINKS IN THE (SUPPLY) CHAIN

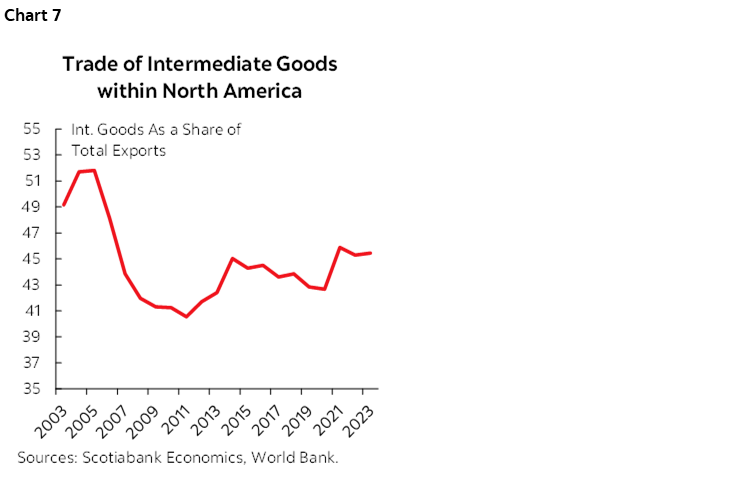

The primary source of value for the US has not been in aggregate trade flows, but what is being traded—and how it contributes to their world-beating economic performance. Even if trade with USMCA partners account for a small share of US GDP, the country benefits through imports of low-cost Canadian energy and Mexican manufactured goods that serve as inputs into US industries. These inputs are often relatively lower-cost, and frequently contain high volumes of US-made content, ensuring trading partners serve as both markets for US manufactured goods, and contributors to its comparative advantage in a range of sectors. These advantageous relationships are most clear when considering trade in intermediate goods (i.e. inputs), which are high within North America (chart 7). The tripartite trades inputs with each other at levels roughly comparable to EU countries (45% within North America, to 49% in EU countries), despite different regulatory standards and the lack of a continental customs union. Sectors that import the highest volume of intermediate goods are typically manufacturing sub-sectors with high degrees of interconnection, including automotive and parts, chemicals and textiles. It stands to reason that these sectors are the primary beneficiaries of the continent’s interconnected supply chains, although each country’s economy has also benefitted in the aggregate. One 2015 study on NAFTA’s effects identified that inter-NAFTA trade in intermediate goods accounted for substantial welfare gains in all three countries, largely as a result of increases in real wages for workers across sectors. These average wage gains were largest in the US, given the role of increased specialization has played in focusing on higher-value components of supply chains.

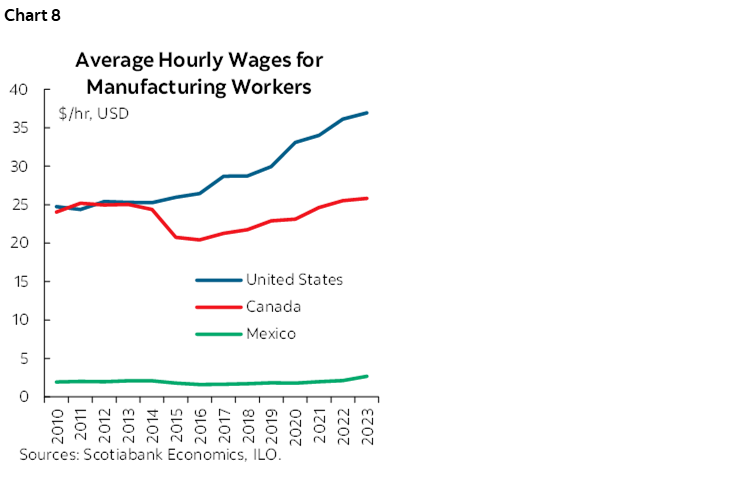

The reality of cross-border supply chains means a share of each country’s manufacturing output and employment can be attributed to maintaining ties with the others, whose proximity has likely prevented supply chains from fully decamping outside North America. High wages for US manufacturing workers have contributed to increased rates of automation and departures for lower-cost jurisdictions (chart 8). Yet NAFTA/USMCA’s presence may have served as a factor to preserve at least a portion of US manufacturing roles that otherwise would have decamped. Had producers not been able to shift lower-value supply chain segments in lower-cost markets (i.e. Mexico), while still maintaining tariff-free access to US markets, they may have opted to fully depart the continent to other markets in lieu of maintaining any US-based production presence. This is difficult to prove authoritatively, given the degree of variables at play, but it is clear that cross-border trade currently supports a share of US manufacturing employment. Analyses from academics and the Peterson institute for International Economics have identified US-made content accounted for 74% of foreign-made content in US vehicle imports from Mexico, and 38% of total value-added in imports of these same cars, highlighting the previously detailed benefits of interconnection. One study looking at Mexican customs data estimates figures are higher still, identifying there may be twice as much US-made content in highly integrated sectors than originally reported.

The automotive sector is the clearest example of these benefits in action. Total automotive trade (imports and exports of vehicles & parts) is responsible for roughly 22% of overall trade within the continent. A New York Federal Reserve Study identified that between 2010–2017 in the US, one in three manufacturing jobs created was in automotive production. In 2023, roughly half of US imports of motor vehicles and parts came from USMCA peers, making these trade relationships critical to supporting the sector responsible for this growth, and for 8% of US private sector jobs in 2022. Benefits are even higher for Canada and Mexico. 91% of Canadian automotive/parts exports and 84% of Mexican automotive/parts exports were bound for the US in 2023. One oft-cited statistic that vehicle parts cross the Canada-US border up to eight times before ending up in a finished product, making clear the realities of cross-border supply chains, as well as highlighting the risks posed by threatening tariffs on inputs. A 2019 study from the Centre for Automotive Research estimated that previous 2018/2019 steel and aluminum tariffs cost US light vehicle manufacturers nearly $500M USD per year. Given that those tariffs affected only two category of inputs, a blanket tariff that applied to every individual re-import and re-export could have effects that were larger by orders of magnitude.

DOLLARS AND SENSE

Significant interconnection has also led to significant investment, as indicated by foreign direct investment (FDI) flows. Integrated supply chains are a significant driver of FDI into each country, with studies indicating trade liberalization as the catalyst for the development and continuation of cross-border capital flows (chart 9). Geospatial mapping from MSCI indicates that over 800 US companies and over 500 Canadian companies operated in Mexico in 2023. For US firms, Canada and Mexico are the first and fourth largest global destination for industrial operations respectively, both ranking ahead of China. To continue with the automotive example, 185 US-headquartered automotive and parts manufacturing firms operate in NAFTA partner countries, with hundreds more operating or involved in subsidiaries. This interconnection offers strong benefits to US firms, with the Cato Institute identifying that half of all Mexican automotive exports in 2023 were made by US automakers. Additionally, while there have been limited studies assessing financial performance from cross-border firms, one 2012 study identified NAFTA had positively impacted profit margins and valuations for firms in all three countries, indicating these firms are key contributors to US economic performance.

Much of the US current account deficit—a source of grievance—is a byproduct of high volumes of foreign investments into productive, pro-growth US assets. Relative to other countries, it is true that the US holds significant net liabilities to foreign creditors. Yet, as the former Chief Economist at the IMF identifies, over half of these liabilities take the form of portfolio equity and FDI investments into American firms, illustrating a link between deficits and direct financial investment into high-producing American firms. Canada and the US have one of the largest investment relationships, with over $1.1 tn USD in direct investment positions between the two countries. Canada was the second largest investor in the US in 2023, and the US was the top investor in Canada in the same year, although it should be noted that Canadian firms invested roughly 74% more into the US than US firms invested in Canada in dollar terms. US direct investment into Canada is primarily in services and financial sectors, while US investment in Mexico is largely in automotive manufacturing. Mexican investment flows do not compare in total value terms, but US and Canadian positions in Mexico have increased by 53% and 294% respectively over the last ten years.

NOT JUST A TALE OF TITANS

Notwithstanding their potential to be competitors for US market access and capital, both Canada and Mexico benefit from the other being involved in the USMCA. Although the share of trade each represents to the other is small, Mexico was the 5th largest purchaser of Canadian goods in 2024, and the 3rd largest source of Canadian imports. The primary path for benefit accrual for both parties arises from their mutual roles in strengthening the US through the suite of channels detailed above, which indirectly supports domestic consumers and firms in turn. Canadian manufacturing has also experienced many of the same challenges as US sectors, but has likely similarly benefitted in many of the same ways as well (increased rates of specialization, distribution of efficient cross-border supply chains, stronger FDI attraction, etc.) from greater Mexican participation.

Attempts to remove either party from the agreement would almost certainly have adverse effects for Northernmost and Southernmost neighbours. A 2020 paper identified that Canadian and Mexican participation in the USMCA may have enabled coordination on key issues that likely generated stronger outcomes for the two countries, relative to a scenario where either individually attempted bilateral negotiations with the US. Attempting to renegotiate future bilateral trade agreements would risk worse outcomes for both countries. Additionally, it may be challenging for either Canada or Mexico to individually fulfill rules of origin as they are currently written into the USMCA. Lower-cost Mexican labour allows products that meet domestic content requirements to remain internationally competitive, relative to potential costs for the same fully Canadian or US-produced product. Additionally, the chances of any one country being able to achieve full compliance are lower than they once were. Rates of non-compliance with USMCA rules have climbed in some sectors, including automotive, even with today’s continental coordination. In future, this may be accompanied by higher tariffs. Finally, breaking up a trade agreement would risk worsening economic performance. This could occur indirectly, as slowing US growth would likely have adverse spillover effects on both Canada and Mexico through reduced demand for their exports. It would also occur directly, if changes to the trade agreement reduced Canadian access to Mexican markets and commercial opportunities moving forward, which the OECD estimates could experience the highest GDP per capita growth of the three countries out to 2050.

TO SPITE YOUR FACE

What is true for two is also true for three: Growing closer offers economic benefits, and growing apart is accompanied by a suite of adverse costs. Categories of consequences can be thought of in two camps. The first is challenges associated with abandoning the USMCA, raising tariffs and affecting extensive marginal investment and production decisions. The second is consequences associated with attempting to proactively unbundle economies through coercive action and threats, which could have substantially larger impacts by shaping intensive margins. These two categories differ, as repealing the USMCA tomorrow would see many of the benefits remain in place in the near-term. For example, manufacturing would still be concentrated in border towns, and many products would still be developed in accordance with USMCA-originating IP and regulatory requirements. Yet, over time, these trends would shift, integration’s benefits would likely begin to unravel, and the adverse effects would become more visible. Attempting to proactively unbundle the three economies, by contrast, could create significant near-term shocks with a rapid onset of consequences.

In the first category, abandoning the trade agreement would likely lead to decreased near-term competitiveness for US manufacturing. One 2017 review of North American supply chains explicitly found that cancelling NAFTA/erecting tariffs would see increases in US automotive production costs, loss of manufacturing jobs, and reduced productivity. These outcomes would surface over time as byproducts of the US attempting to produce components of value chains in which it has little to no comparative advantage, eroding existing efficiencies. This decline in competitiveness would subsequently affect margins, with the same 2017 study estimating every 2% increase in average production cost for Mexican manufactured goods could see net margins decline by up to 30% for certain sectors.

Walking away from the USMCA and imposing tariffs would also be bad for jobs, particularly in manufacturing, given the downstream effects of tariffs. A 2019 study from the US Federal Reserve estimated that for every 1000 jobs created in US steel production by the 2018/2019 tariffs, higher downstream costs saw 75,000 fewer manufacturing jobs created in subsectors reliant on steel as an input. Other studies, including the United States International Trade Commissioner’s own analysis of the economic impacts of 2018/2019 steel and aluminum tariffs, have identified the small positive employment benefits generated by tariffs were more than offset by job losses as a result of rising input costs, retaliatory tariffs, and uncertainty.

The second category’s consequences are yet starker, as a fulsome attempt to de-integrate would have far higher costs that were felt much more rapidly. Specialized supply chains and agglomeration effects that have driven strong economic performance thus far could unravel, with a 2017 study estimating US automotive and agricultural sectors would be particularly impacted. US manufacturers would face dual headwinds of reduced efficiencies as cross-border supply chains disappeared, and reduced market access due to retaliatory trade barriers. Their competitiveness would likely decline, as firms operating in the US would face an “all-in” or “all-out” choice that reduced flexibility required to compete with firms benefitting from regional integration in Europe or Asia. Protectionism would also make the region as a whole a less attractive FDI destination. One 2020 study estimated that losses for Mexico from slowing FDI, if the USMCA were cancelled, could outweigh gains accrued over the last three decades. Additionally, the same study identified benefits to Asian automotive producers if North American auto sectors became less integrated. Historically, FDI flows from Japan into the US were partially predicated on compliance with rules of origin requirements, a justification that would become irrelevant if Canada and Mexico saw tariffs imposed. Millions of jobs linked to cross-border trade could be lost, along with a potentially far larger number of roles reliant on export income. Growth could be structurally lower for all three parties. Some of the worst impacts would be felt by US SMEs, whom—as noted earlier—are responsible for the majority of export flows to Canada and Mexico. There would also likely be spillover effects from decline. For example, a Mexican government facing protectionism may see priorities shift away from managing immigration flows cooperatively, potentially exacerbating or worsening Southern immigration challenges. If rapid unbundling were attempted, many of these consequences would not be felt over a decades-long time horizon, but may begin to become apparent within a period of months or years.

Beyond this list of adverse effects, the promised benefits of autarky would also be unlikely to materialize in the US. As just one example, previous analysis from Scotiabank Economics has identified that fully repatriating manufacturing would stretch US labour markets beyond their means. Given that Mexico and Canada accounted for 28% of goods imports in 2024, a rough estimate is that replacing imports from North American countries would require an additional 1.1–2.2M US manufacturing workers (varying depending on productivity), largely concentrated in sectors like automotive, food and beverage production, and electronics manufacturing. Current labour shortages within manufacturing, reduced immigration, and unfavourable demographic trends would all serve as headwinds likely to dramatically limit upside risk. These headwinds could actually see promised benefits turn to costs, with inflationary impacts, reductions in consumption and downside risk to growth proving likely in an environment of elevated labour demand relative to supply. This is partially due to large market effects, which indicate a tradeoff between consumer welfare and margins for input producers that structurally reduce welfare for both, absent greater trade openness. This trade-off is yet another reason why continental exchange is so advantageous for Canada and Mexico, and why the US could face stark trade-offs/constraints that structurally lower growth in its pursuit of closed-economy aims.

IT WON’T WORK IF WE DON’T WORK IT

The trade war is unlikely to disappear, but the best-case scenario is still one that sees this period conclude with the USMCA in place, and all parties remaining committed to it. That requires ensuring it remains in the interest end benefit of all parties to do so. The upside of remaining integrated remains clear, but the future of the USMCA is currently less so. Current realities suggest a growing deficit of trust between trade partners, which risks reducing the belief that parties will adhere to the text or spirit of any future agreement. For example, a scenario exists where Canada and Mexico are asked to sign onto an agreement that would leave them in worse positions than they are today, coerced by threats of permanently high tariffs, without faith that benefits like tariff-free access will remain in place going forward. This outcome would be best to avoid. A future that maintains an agreement on paper, but not in practice or spirit, would see the benefits of integration rapidly erode, bringing about consequences similar to those detailed above. In the absence of trust, a new approach to managing continental trade may be required, although any shifts towards reduced integration will almost certainly offer worse economic outcomes than have been experienced in the last three decades. Yet for Mexico and Canada, change is likely preferable to coercion and continuous looming threats of cancellation.

It would be a genuine tragedy for the continent to willingly sacrifice its drivers of prosperity in pursuit of goals that are likely to leave all parties worse off. Disruptive and protectionist rhetoric are likely to continue (or increase) in the coming period, but the ultimate costs of reduced interconnection will likely be borne by North American consumers, firms and workers who benefit from and rely on cross-border flows of goods, capital and products. The region’s dynamism has been shaped by its interconnection, and pushes to reduce that are likely to generate high volumes of self-imposed costs. A better approach would be for all three countries to remain tightly integrated, and continue leveraging potential and know-how to drive forward growth in all three countries. Hopefully, the path forward can begin to pull in that direction once again.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.