CANADA HOUSING MARKET: WARM WEATHER, COOLER MARKET!

SUMMARY

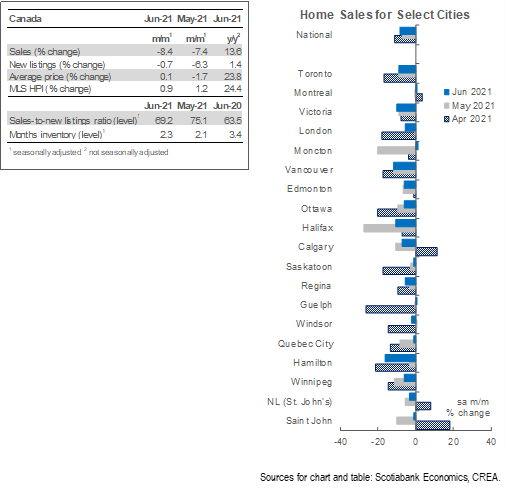

Canadian home sales declined by 8.4% (sa m/m) in June for a third decline in a row. Listings also fell, but by a significantly smaller 0.7% (sa m/m). With sales falling significantly more than listings, the national-level sales-to-new listings continued to trend lower since its January 2021 91% peak to 69.2% in June—its lowest level since August 2020, but still higher than its long-term average of 54.5%.This higher than average sales-to-new listings ratio indicates markets are still experiencing tight supply-demand conditions. As a result of this persistent tightness, the composite MLS Home Price Index (HPI) rose by 0.9% (sa m/m)—also continuing its trend of steadily decelerating after recording the biggest monthly price gains since 2000 in February and March of this year. Whereas in previous months the deceleration was mostly driven by the single-family homes and townhouses segments while apartments maintained momentum, the latter is now experiencing price deceleration too.

Movements in the market continued to be broad-based as they have been during the pandemic, with declines in sales spread out across much of the country. Of the 31 local markets we monitor, 26 witnessed sales declines in June compared to May, with the other 5 markets experiencing an average increase of a mere 1% (sa m/m). As in previous months, it is important to remember that June’s results are historically strong. Despite a retreat, the level of sales still set a record for the month, being 32% higher than the (sa) June-average level of sales from 2000 to 2019.

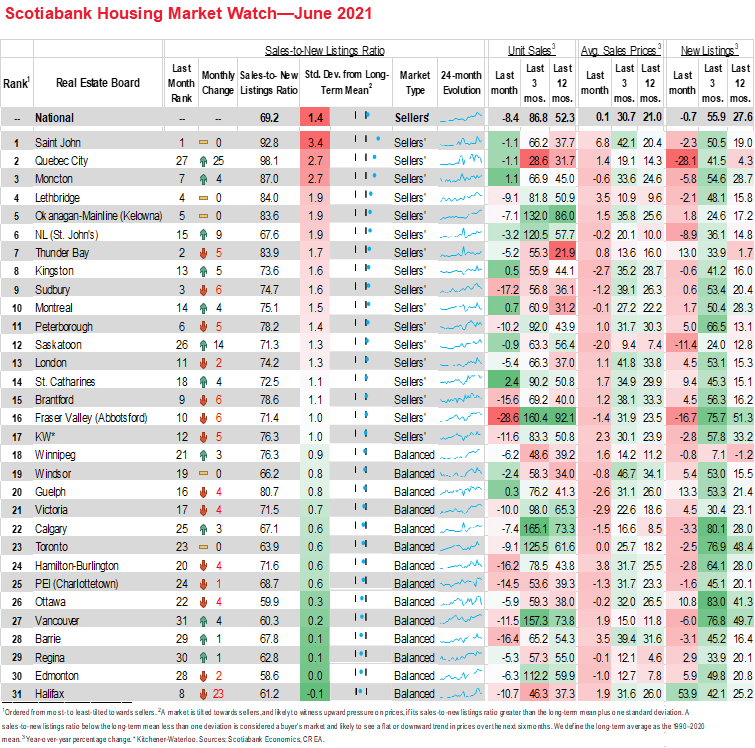

Listings dropped this month but at a much smaller pace than sales, bringing up months of inventory from record-lows for the third consecutive month. Relative to the drop in sales, listings were little-changed in June and declines were not as broad based, where as many as 15 of the 31 centres in our list experienced increases. While rising listings are a welcome change for buyers in these markets, the national result still shows a decline, and supply conditions remain tight. Indicative of this might be that 3 of the 5 markets that witnessed sales gains also saw listings increase. Nonetheless, the much smaller reduction in listings compared to sales further relaxed the sales-to-new listings ratio for the fifth consecutive month this year, reducing the number of centres in sellers’ market territory from 22 in May to 17 in June. Months of inventory continued to rise from their lowest level on record in March 2021 of 1.7 months, but remain lower than the long-term average of 5 months. At the current rate of sales activity, national inventories would be liquidated in 2.3 months.

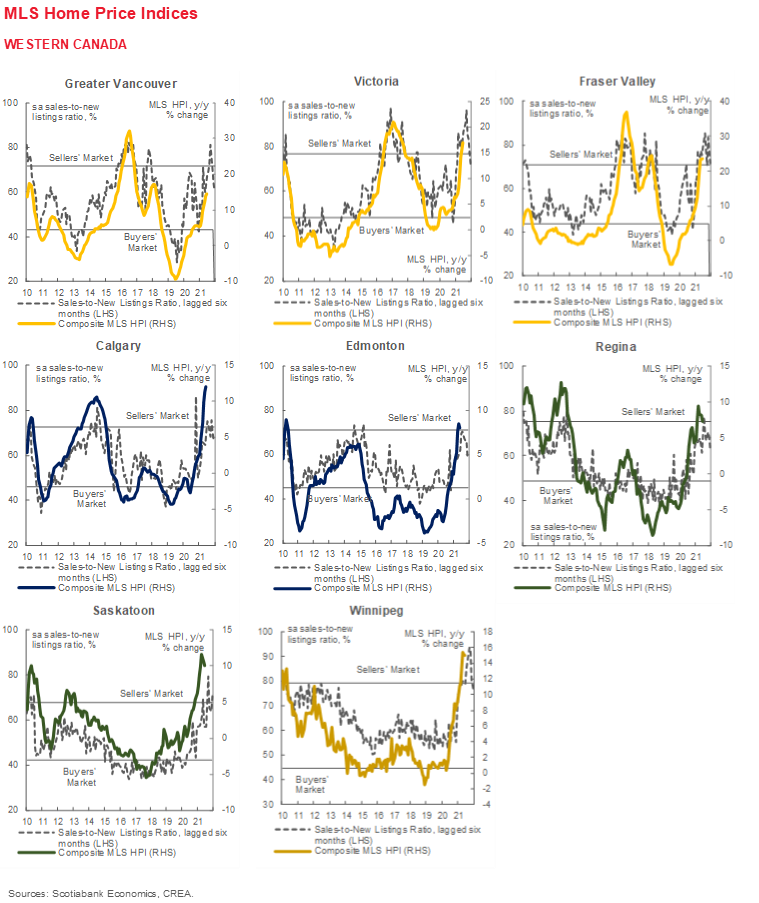

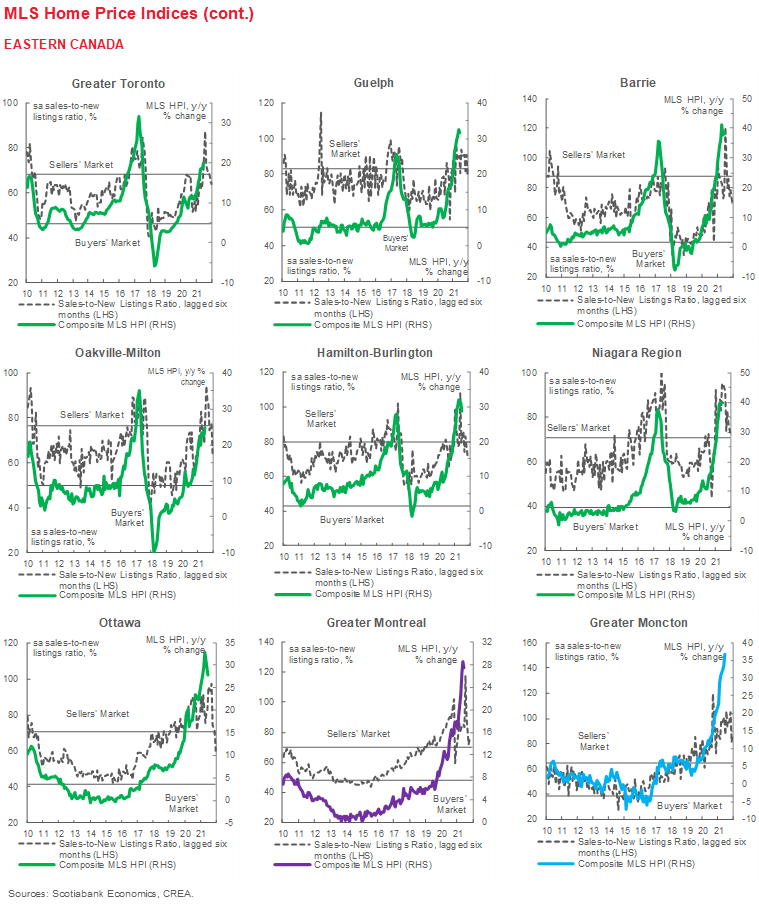

Apartments and townhouses experienced the largest deceleration in price gains, after 3 months of single-family homes leading the deceleration. The composite MLS HPI for all homes in Canada increased by 24.4% (nsa y/y) in June 2021—the biggest year over year increase on record since 2005. While all types of homes recorded their biggest year over year increases in June 2021, they all (except for apartments) recorded their smallest monthly price gains since January 2021.

IMPLICATIONS

The housing market has softened for the third consecutive month since its record breaking levels in March 2021. While the market remains very strong relative to historical standards, with June 2021 results setting an all time record for the month, it is displaying signs of fatigue, with sales, listings, and price gains slowing down after months of going full steam ahead. Don’t mistake this for a finish line to the rally, however, as persistent tightness in the market, despite the decline in sales, continues to push prices upward, albeit at a slower pace.

No one single factor emerges as the clear driver of the slowdown in June and the preceding two months. Some may point to OSFI’s new and tighter stress test, which came into effect on June 1st—but the extent to which this impacted the market is unclear, and seems negligible, as it likely only impacted buyers on the margin who have already been priced out of the market. Instead, we look to the erosion in affordability after months of unsustainable price increases and persistent shortages in supply—the latter exacerbated by listings dropping simultaneously with sales, even if at a much smaller pace in June, as the market has already been in sellers’ territory. Moreover, market participants are likely shifting their focus toward enjoying a double-vaccinated summer and vacationing, particularly as travel is returning and threats of a fourth wave due to the delta variant are looming in the background.

The need for more space suddenly doesn’t seem as crucial as it did a few months ago, when we were all locked inside our houses during the winter months, with no return to offices in sight. With herd immunity looking closer than expected, likely late July or early August, the story has changed.

This shift in preferences might be apparent in the divergence of activity between apartments and other market segments. In Toronto for example, while larger units continue to drive the year-over-year price growth, sales activity and average selling prices fell for all types of homes relative to May except for apartments, where sales and prices increased. This shift is likely exacerbated by the widening price differential and relative unaffordability of larger units. Moreover, it is likely that those who have been priced out of the market for these larger units are now turning to renting after giving up on the idea of owning them. And this could be driving the recent activity in the rental markets, where now there are nascent indicators of bidding wars, which plagued the resale market during much of the COVID-19 pandemic.

All in all, it seems that the circumstances that fueled the housing rally over the past year or so are dissipating as expected, with affordability weakened and immigration continuing to be muted. This will most certainly change with the influx of immigration upon opening our borders which will increase demand for housing while the long-standing shortage in supply remains unchanged. Significant efforts need to be put in place to relieve the imbalances that existed in the Canadian housing market long before COVID-19 hit, and the recent slowdown in the market does not reduce the urgency of these efforts. The housing market in Canada is traditionally slower in the summer compared to spring, and this year may be no different. The only difference this year seems to be that much of the spring activity was brought forward, with March being the peak, followed by the summer slowdown. It is likely that the upcoming couple of months will resemble June in levels of activity before those pick up as the new school year begins. As domestic and global conditions simultaneously improve, jobs-recovery and population growth will continue to support housing prices—which are more likely to go up than down, further weakening affordability, until we achieve a better supply-demand balance.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.