CANADA HOUSING MARKET: 2022 WRAP-UP

SUMMARY

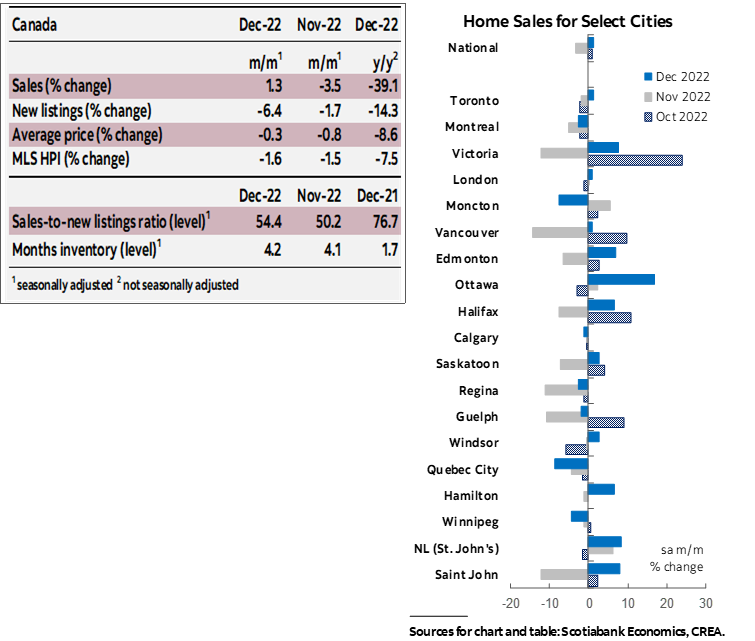

Canadian home sales rose 1.3% (sa m/m) in December, alongside a large decline in listings of 6.4%. This increased the sales-to-new listings ratio, an indicator of how tight the market is, to 54.4%, but it remained below its long-term average with the national housing market still in balanced territory. Months of inventory continued to climb up from record lows, reaching 4.2 months—a significant improvement from its all-time low of 1.7 months earlier this year, but still a full month below its long-term average.

The year as a whole recorded 25% less sales than in 2021, 1.7% less listings, and 5.5% higher average selling price.

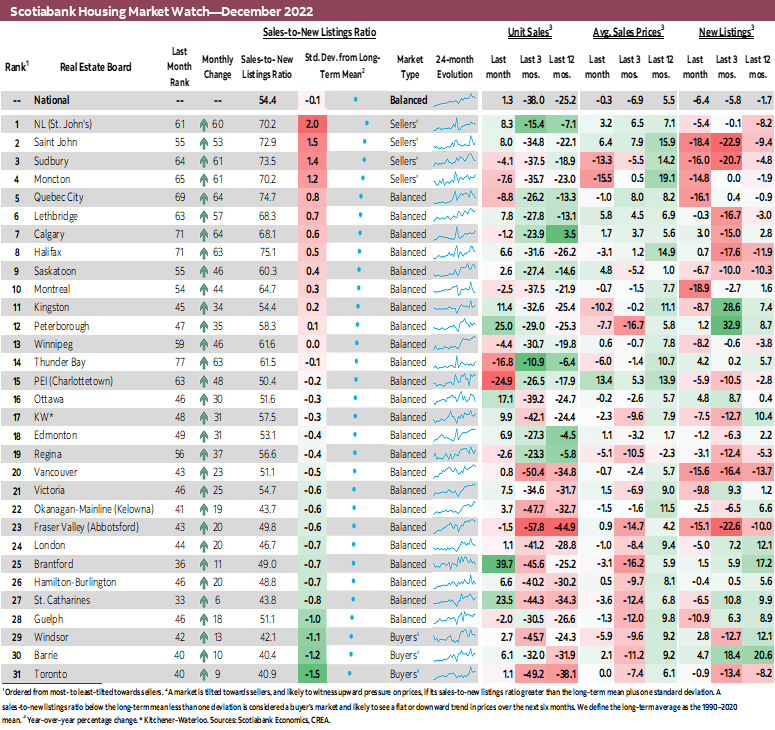

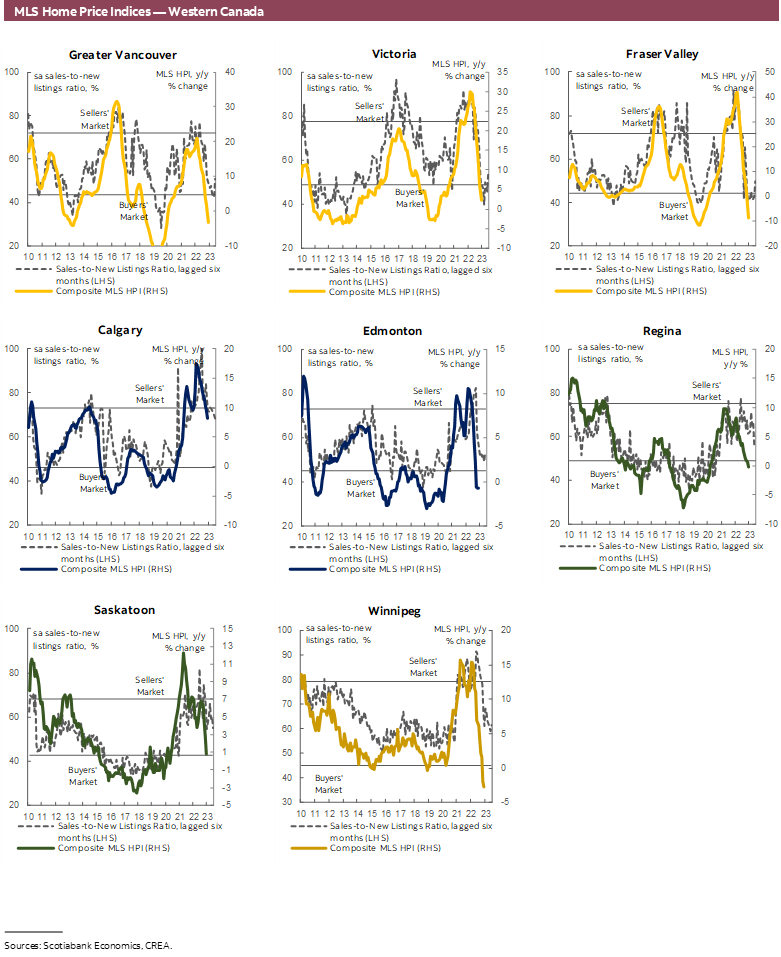

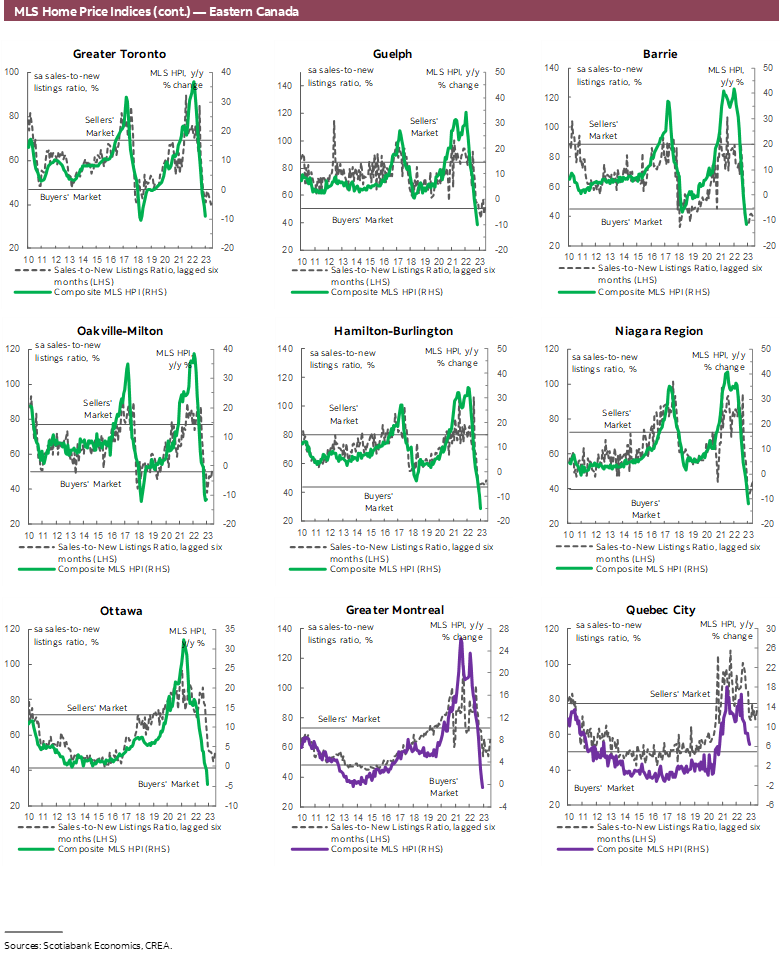

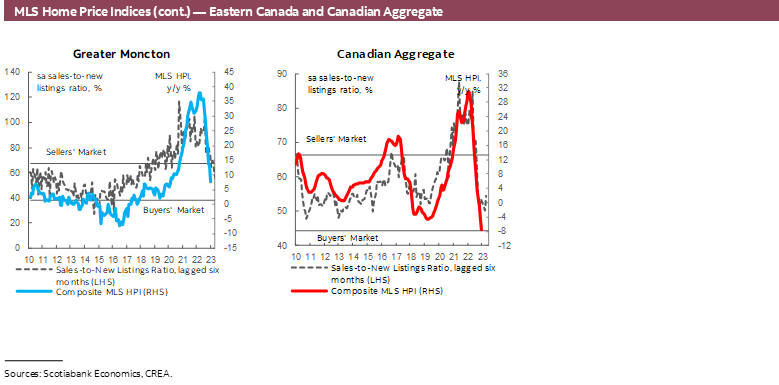

Of the 31 local markets we track, 24 ended the year in balanced territory compared to 28 starting the year in sellers’ territory. Cities in Atlantic Canada, St. John's, Saint John, and Moncton, as well as Sudbury in Ontario, remained in sellers’ territory, while buyers had the upper hand in Windsor, Barrie, and Toronto.

Prices declined again in December in line with more balanced market. The composite MLS Home Price Index (HPI) edged down 1.6% (sa m/m) in December, ending the year 13% below its February 2022 peak. Single-family homes continued to lead monthly price declines, falling by 1.8%, compared to only 0.9 decline for apartments. Relative to December 2021, the composite MLS HPI (nsa) was 7.5% lower, with single family homes 9.2% lower and apartments relatively the same, 0.1% higher.

The annual average MLS HPI was 12% higher in 2022 than in 2021, with that of single-family homes around 11% higher while townhouses and apartments almost 15% higher.

IMPLICATIONS

Canada’s housing market ended 2022 on a different note than the one it started on.

The year started with historically tight market conditions. The sales-to-new listings ratio was at record high levels, so were monthly and yearly price gains, while months of inventory was at its lowest. Demand for homes was largely fueled by low borrowing rates and the housing ‘FOMO’ that was dominating the market psychology. Demand in February was rather boosted by a rush to lock in lower rates as expectations were mounting of an overnight rate hike in March as signalled by the Bank of Canada in its efforts to fight historically high inflation. At the same time listings were performing relatively poorly, stalled by wide-ranging factors. Among them are older and retired Canadians’ staying longer in their owner-occupied housing; the erosion of affordability and aggressive bidding wars which made listing and entering the market as buyers less appealing; expectations of continued future price appreciations which enticed homeowners to postpone listing to maximize return; and accommodative rates where the cost of borrowing was quite low making it more attractive and affordable to buy a new home and keep the old one as a rental investment property, especially given the structural supply shortage and expected future capital gains.

While economic indicators were pointing to strength in the economy at that point, measures of consumer sentiment had generally been on the decline and households were suffering from bad-news fatigue after two years of the pandemic. The Russian invasion of Ukraine put further pressure on already rising prices, with daily expenses increasingly taking up a bigger share of households’ incomes. We began to see a shift in market psychology with buyers increasingly embracing a wait-and-see approach as uncertainties mounted and hopes of a normalization in prices in response to the expected higher future borrowing rates took hold.

The Bank of Canada began its hiking cycle in early March, and while a single hike wasn’t going to have a material impact, it was the expectation of more to come along with heightened rate sensitivity and worsening economic conditions, such as loss of purchasing power, fall in stock markets, and rising costs of inputs that drove movements in the market over the next few months. With ever increasing mortgage sizes required to afford the hefty price tags on homes after two years of unsustainable appreciations, marginal increases in borrowing rates translated into relatively larger increases in mortgage payments and reduction in affordability. This increased the response of housing demand to the Bank’s rate hikes and ensuing increase in mortgage rates and stress-testing thresholds. Additionally, while Canadian households increased their net wealth to record high levels during the pandemic, they also increased their liabilities, encouraged by record low rates and “cheap” debt. This increased indebtedness made debt servicing ratios more sensitive to the renewal of these loans at higher rates.

Notwithstanding the above factors, a normalization of housing market activity was expected from the elevated levels in 2021. The year recorded the highest ever level of sales despite having been the weakest in Canada’s modern history in terms of population growth, which was effectively zero. Therefore, the softness in 2022 was also partly the outcome of an advancement in purchases to 2021 that would’ve otherwise taken place later.

Supply-demand conditions eased in many parts of the country and the national housing market entered balanced territory as the housing market reacted to a slew of factors. The pace of the recalibration initially seemed alarming but progressively slowed down in line with expectations as limited supply and demand fundamentals provided an offset. Indeed, subsequent monthly declines in sales were getting smaller each month, and October and December even saw sales edge up.

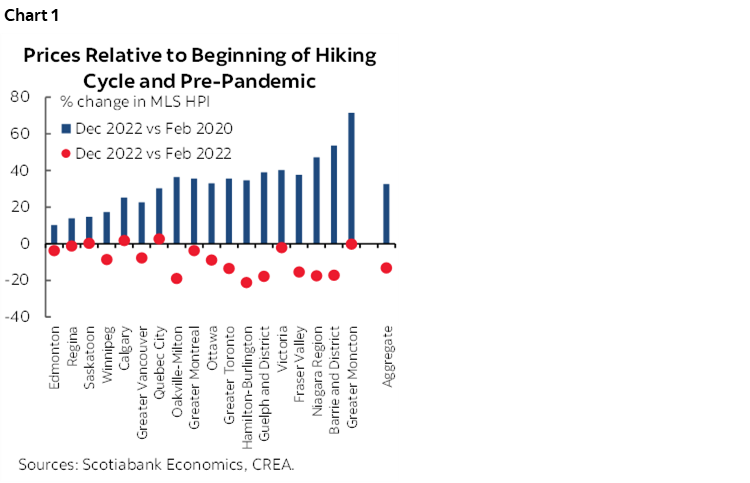

The year ended with sales activity below long-term averages, over 25% below the record set in 2021 and almost 38% below February 2022 levels. Both sales-to-new listings ratio and months of inventory were more in line with historical levels. The MLS HPI ended the year 13% below its February 2022 peak, but remained 33% above pre-pandemic levels (chart 1).

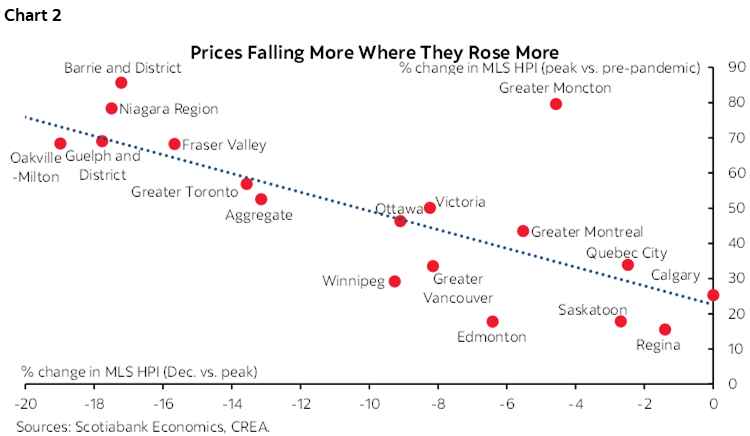

Therefore, we still see some room for prices to decline in 2023, but by how much and for how long varies significantly across cities. So far, we have seen bigger price adjustments down from peaks in cities where prices climbed more during the pandemic (chart 2). On the other hand, some cities’ prices have barely fallen since last year, if at all. Calgary, for example, is seeing prices rising still and they are now higher than February 2022. Alberta had seen a record-breaking increase in population over the past year, reflecting in part cheaper costs of living, including housing. Similarly, the share of new international immigrants settling in Atlantic Canada has been on an upward trajectory, which is likely why we see very little price declines in Moncton despite having had increased by a baffling 80% since the pandemic.

As we look ahead, population dynamics are likely to continue playing an important role. We are currently experiencing the most rapid pace of population growth in 50 years. The federal government continues to set higher immigration targets with an increasing commitment towards more economic immigration, which translates onto higher population growth and demand. This means recent easing in supply-demand imbalances in Canada’s housing market may reverse if no progress is simultaneously made on increasing the stock of housing supply.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.