SALES, LISTINGS EASE AS SECOND WAVE LOCKDOWNS TAKE EFFECT

SUMMARY

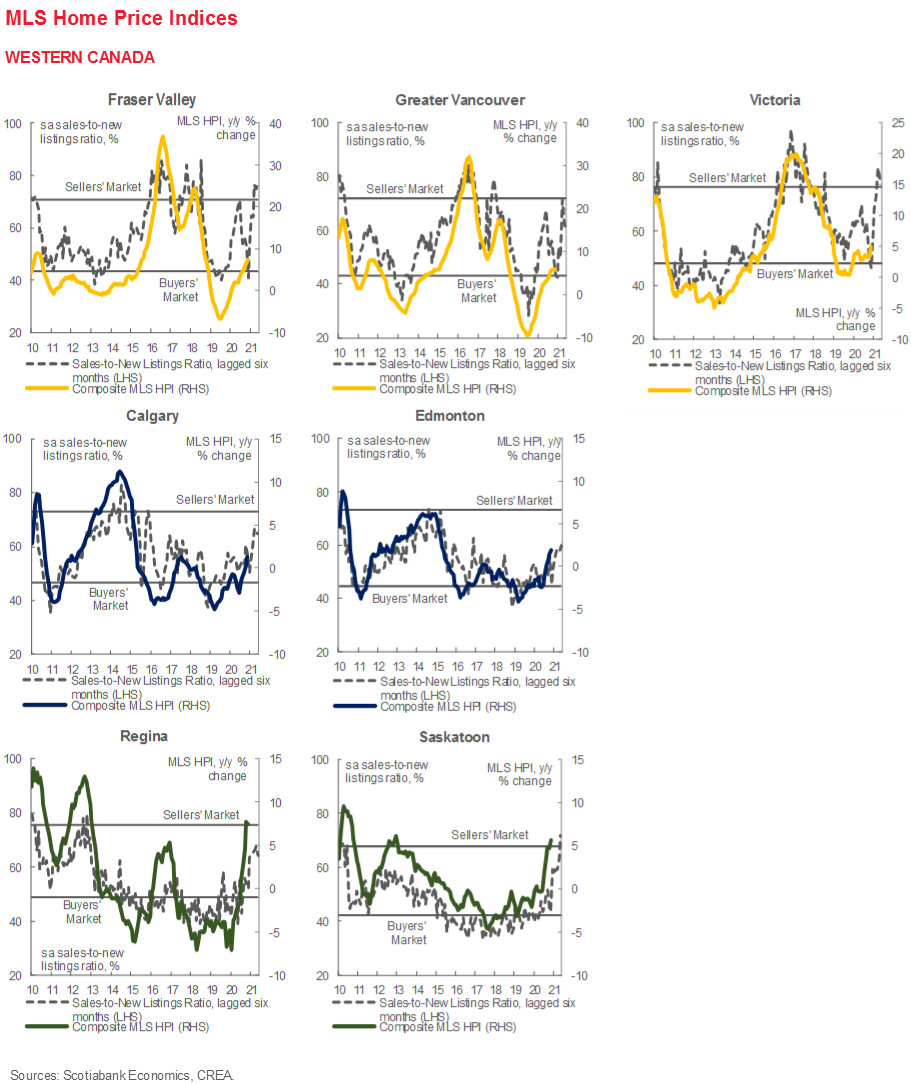

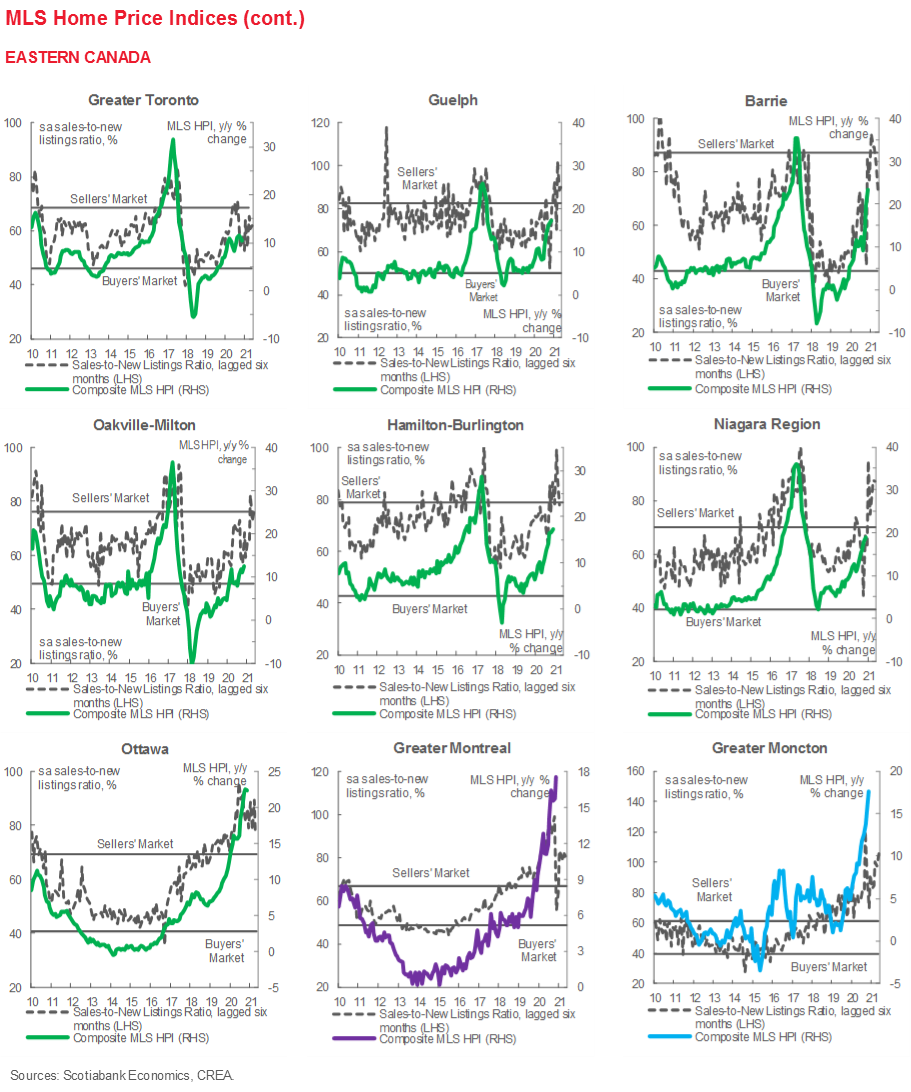

Canadian home sales fell 1.6% (sa m/m) in November 2020. It was the second successive national decline, but last month was nevertheless the strongest November on record. New listings also dipped by 1.6% (sa m/m) to keep the sales-to-new listings ratio at 74.8%—consistent with supply-demand balances strongly favouring sellers—and the 11.6% (nsa y/y) climb in the composite MLS Home Price Index (HPI) was the steepest since 2017. Single-family homes again underpinned that price appreciation, rising 14% nsa y/y.

National-level sales and listings trends were broad-based. Sales decreased in 21 of the 31 local markets that we track, while new listings decreased in 19 centres. For the second consecutive month, the largest sales declines tended to come from Ontario’s Greater Golden Horseshoe region—now in its second month of second wave restrictions. Consequently, sales-to-new listings ratios were steady in most jurisdictions in November, with the majority continuing to report supply-demand tightness consistent with sellers’ markets and accelerating MLS HPIs. Relative to February—the last full month before COVID-19 lockdowns took effect—sales and listings are up in 26 and 20 local markets, respectively.

By-unit type price movements were also similar across Canada’s largest centres. In Toronto, Vancouver, Calgary, and Edmonton, HPI gains among single-family homes continued to significantly outpace those in the townhome and apartment categories; in Calgary and Edmonton, growth in single-family home prices offset declines across other unit types. They also led torrid price advances in Montreal, though townhomes and apartments are also in the midst of hefty value appreciation. Ottawa continued to witness HPI growth in excess of 20% nsa y/y in all unit types.

IMPLICATIONS

Nine months since the pandemic’s arrival in Canada, homebuyers continue to demonstrate a preference for housing units with more space and, in some cases, that are further away from city centres. Outsized MLS HPI growth in the larger, higher-cost single-family home category persisted across a range of cities. Data from the Toronto Regional Real Estate Board—released earlier this month—also indicate stronger sales growth in the regions surrounding the City of Toronto than in the city itself.

Signs of slowing economic momentum showed up in the real estate transactions data once again. November was the first full month of second wave restrictions in several provinces, and corresponded to a second consecutive monthly decline in home purchases at the national level and in 21 of the 31 cities we cover. Meanwhile, new listings activity has now retreated in two of the past three months—likely a consequence of easing reopening effects and new lockdown measures.

Still, the 10.5% y/y ytd growth in sales as of November highlights what has been a truly remarkable 11 months for Canadian housing markets. A near 20-year best in home sales was almost unthinkable at the height of the first wave lockdown when sales witnessed a record drop of more than 50% sa m/m. Yet, as it stands, for national-level purchases not to experience their strongest annual percentage increase since 2002, they would have to decline in the order of 40% nsa y/y in December. The trend exists across major metropolitan areas: 24 of the 31 centres we track have witnessed y/y ytd sales gains in excess of 5% as of November, with 26 having recouped March–April losses by July.

Our updated economic outlook guides our expectations for Canadian housing markets over the coming year. We suspect that reduced mobility and economic activity related to COVID-19’s second wave will translate into further slowing of residential real estate transactions momentum in the next few months. The effects of the softer population growth witnessed this year due to border closures may also contribute to more modest real estate activity in 2021. Prospects look rosier in H2-2021, when we expect widespread inoculation to drive a boost to economic growth, with more demand-side support from rock-bottom interest rates and extended federal fiscal measures. The present supply-demand tightness will likely bolster home prices over the near-term as well.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.