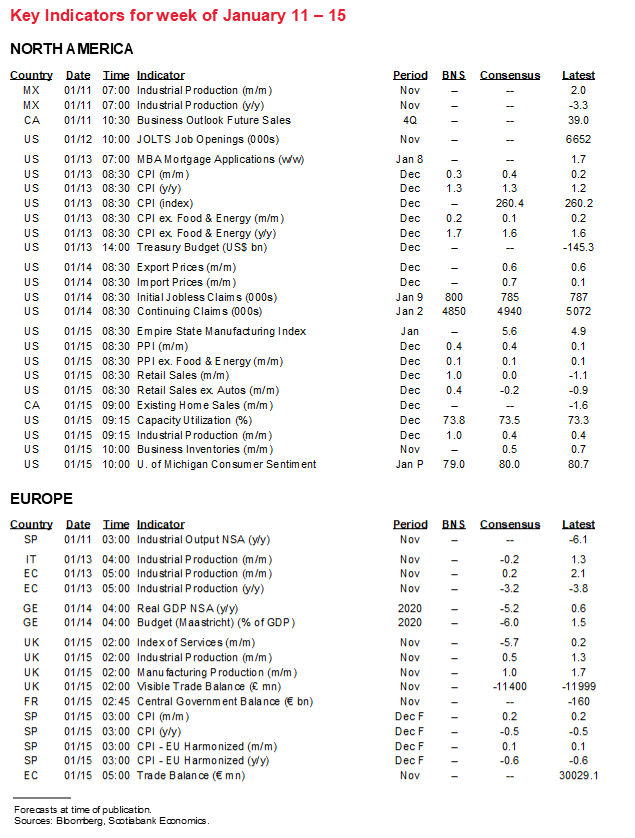

Next Week's Risk Dashboard

• Biden’s plan

• Fed’s Powell

• Impeachment theatrics

• COVID-19

• BoC’s surveys

• CBs: Peru, BoK

• CPI: US, China, India…

• …Brazil, Norway, Sweden, Argentina

• US, China and UK macro

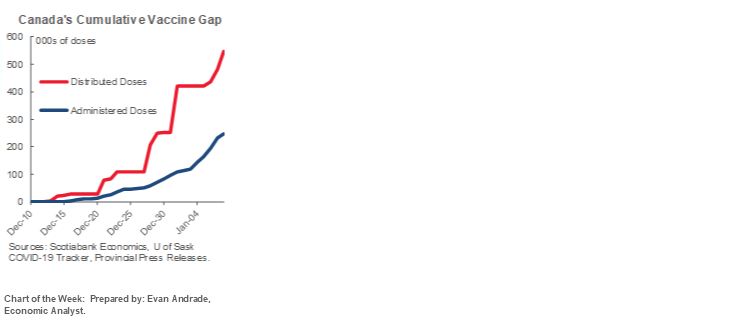

Chart of the Week

UNITED STATES—BE CAREFUL WHAT YOU ASK FOR

Next week promises plenty of fireworks as most of the global market attention will be centered upon US developments. They will include stimulus plans, freshened Fed guidance, monitoring COVID-19 cases and restrictions plus a few macro hits along the way. In addition there may be further impeachment developments.

A Reuters/Ipsos poll showed that 57% of Americans want Trump to be impeached, though based on the popular vote during the election that may imply that only a slim minority of Republican voters support such a step which is likely to guide the Senate’s GOP members against driving the requiring super majority. Still, the rhetoric may be rather loud.

President-elect Joe Biden has guided that he will announce the outlines of a stimulus plan on Thursday. Biden has guided that the price tag with be “high” and in the “trillions” and is expected to include plans for US$2,000 stimulus cheques, more generous unemployment assistance and enhanced aid to city and state governments. One issue is the degree to which the Democrats will support such an aggressive package. Senator Joe Manchin, for example, initially objected to stimulus cheques that high at about a US$400B price tag, but later indicated that he might be convinced if the amounts were to be targeted. Targeted means-tested assistance that doesn’t send cheques to millionaires might be the easy and generally sensible way of achieving agreement.

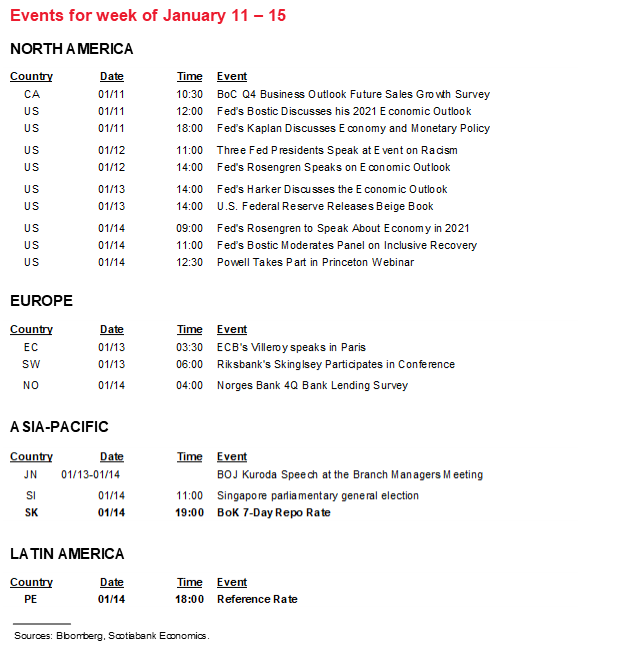

On that same day, Fed Chair Powell will speak in a fluid conversation format at a Princeton University event (12:30pmET). He’s likely to generally reinforce the more upbeat take offered by Vice Chair Clarida in published (here) and verbal remarks, but he may have a greater sense of Biden’s fiscal plans by then. In play is the shift in the policy balance more toward fiscal policy relative to monetary policy and how the Federal Reserve may react over time. The Fed spent years beseeching Congress to apply more fiscal stimulus and it may be getting it in spades now. Bond markets are already reacting with persistent curve steepening. Still, the 10 year Treasury yield has only risen toward 1.1% from about ½% at last summer’s low.

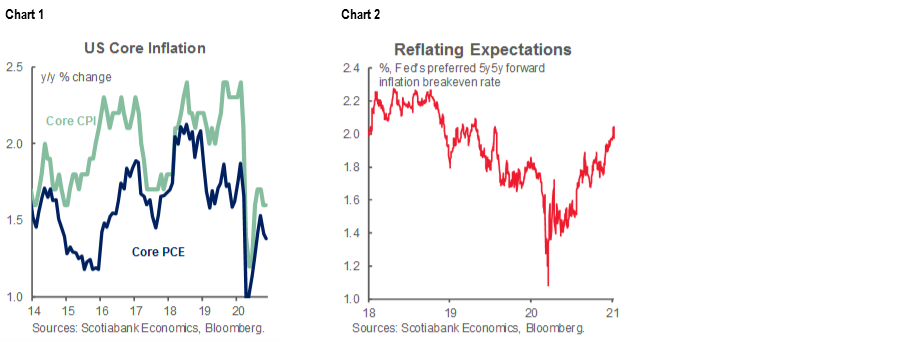

Wednesday’s CPI inflation figures could bring out marginally higher pressure in terms of both headline and core ex-food and energy measures. I’ve gone with a one-tick rise in overall CPI inflation to 1.3% y/y and ditto for core CPI at 1.7% y/y. That’s based upon a combination of stronger contributions from gas prices, seasonal influences and a shift in year-ago comparison periods. If this estimate is on the mark, then it might feed expectations for the Fed’s preferred core PCE gauge to tick higher while probably nevertheless remaining marginally softer (chart 1). Still, core PCE inflation at 1.4% y/y the prior month has averted the deflationary risk that sparked concern in markets in the earliest stage of the pandemic while market-based measures of inflation expectations have sharply risen of late (chart 2).

Friday’s retail sales will cover off the rest of the holiday shopping season when December’s figures land. I’ve gone relatively high compared to consensus. We already know that new vehicle sales were up by 4.6% m/m in December at a seasonally adjusted rate and that gas prices were up by 4.4% m/m which would combine to contribute over one percentage point to retail sales growth. Weekly chain store sales have been volatile but on the softer side in December, though they don’t capture on-line sales.

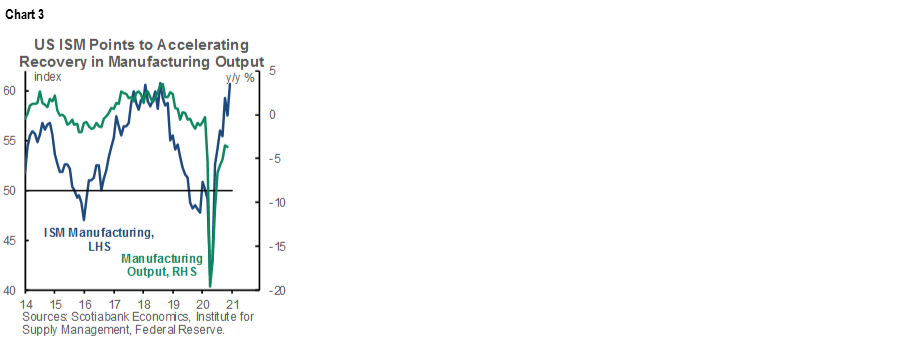

Other releases will include JOLTS job openings that probably softened (Tuesday), Wednesday’s Beige Book of regional conditions, and weekly jobless claims on Thursday. Friday brings out a likely gain in industrial production and particularly manufacturing output after ISM-manufacturing recently surprised higher (chart 3), as well as the Empire gauge to start off another month of manufacturing surveys, and the University of Michigan’s consumer sentiment reading plus producer prices for December.

CANADA—SURVEY SAYS!

Canadian markets are likely to be primarily driven by developments abroad given a very soft domestic calendar.

The Bank of Canada will update survey-based evidence of business and consumer conditions and expectations on Monday just before going into communications blackout the next day ahead of the January 20th decision. The survey results don’t necessarily carry the day by way of the policy bias but can at times reveal new information quicker than hard data. Whether they will be fresh enough is potentially in dispute. The Business Outlook Survey’s sample period will be roughly from mid-November to early December and the Survey of Consumer Expectations would have been conducted over the latter half of November.

Still, among the considerations are whether businesses have materially changed their inflation expectations (chart 4) to match the rise in market-based measures (chart 5), as well as sentiment toward hiring, the magnitude of labour surpluses, the amount of slack in their operations and capital investment plans. The consumer survey may offer additional insights into distributional matters such as where excess savings reside and what consumers plan to do with them. Recall that the prior survey in September indicated that most of the excess overall savings had been ramped up by relatively upper income households who had planned on retaining at least some of their stockpiles (charts 6, 7). Still, the survey defines upper income earners as households earning above C$100k/yr. Compared to some of the political rhetoric, that hardly qualifies as millionaires and billionaires especially in some of the country’s most expensive cities.

Canada also releases existing home sales for December on Friday. They had fallen for two consecutive months but results like we’ve seen from Toronto for the month could push the tally higher this time.

LIGHT DEVELOPMENTS ELSEWHERE

With the US hogging the global market spotlight, developments will be fairly light elsewhere.

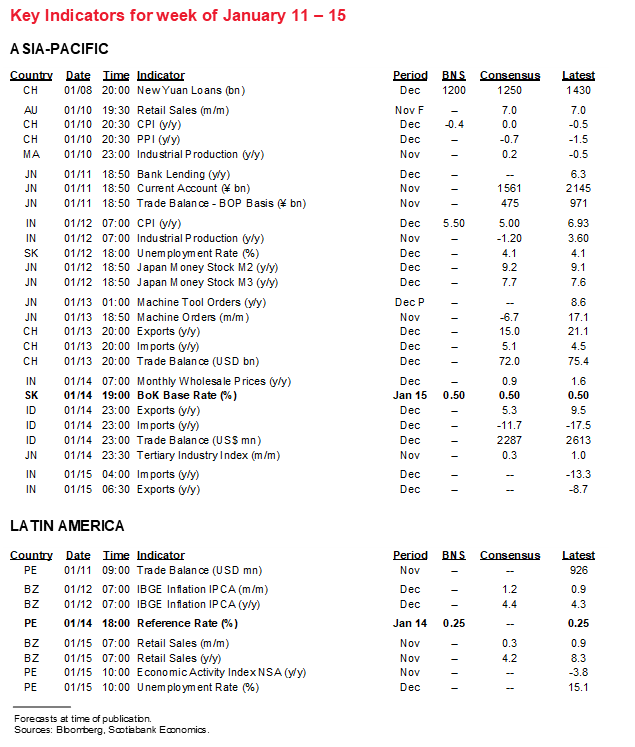

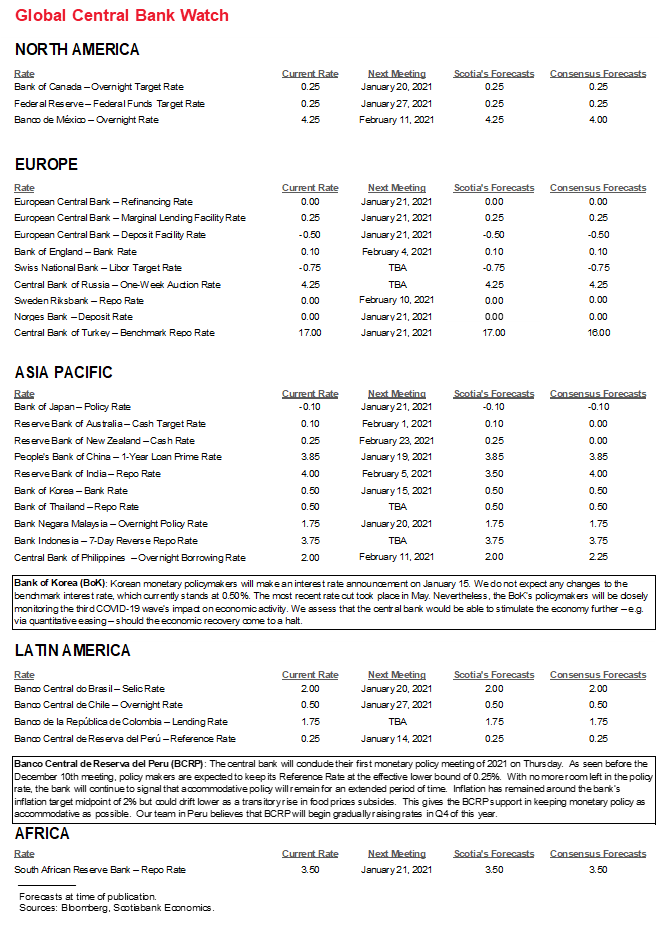

Only two central banks will deliver policy decisions and they are not expected to influence local markets let alone global risk appetite. The Bank of Korea is universally expected to stay on hold at 0.5% on Friday and so is Peru’s central bank at 0.25% on Thursday.

Further insight into how Q4 ended for the UK economy will arrive on Friday with industrial production, a services index, trade and monthly GDP. The UK economy is expected to register a large lockdown-induced hit on the order of +/- 5% m/m.

China updates inflation for December to start the week and it could showcase the first bottoming evidence since diving into freefall after July (chart 8). The country will also update monthly aggregate financing and trade figures while the PBOC is likely to keep the one-year Medium-Term Lending Facility rate unchanged at 2.95%.

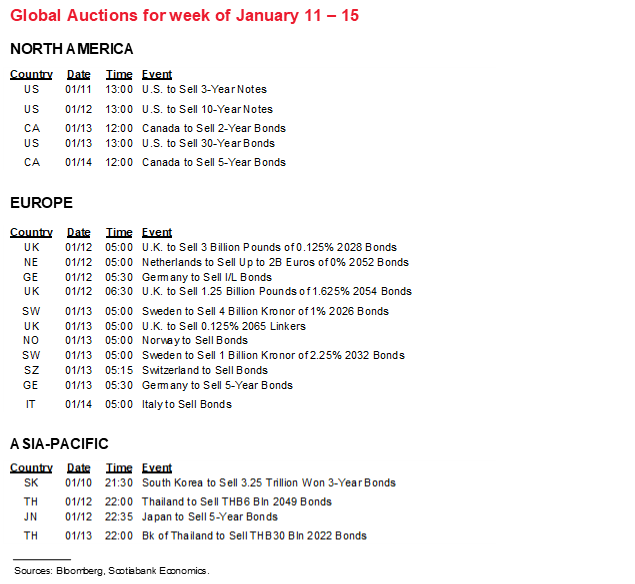

Latin America’s calendar will otherwise be rather quiet with just inflation figures out of Brazil (Tuesday) and Argentina (Thursday). Ditto for Europe with just inflation figures out of Norway (Monday) and Sweden (Friday) alongside the Eurozone add-ups for industrial production and trade (Wednesday). Asia-Pacific markets receive Indian industrial output and CPI (Tuesday) and trade figures (Friday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.