Very strong post-COVID rebound underway in Q3, leading to upward revisions to growth forecasts in some countries.

There remains much economic damage to repair, and a return to pre-COVID levels of economic activity is still several quarters away for many sectors.

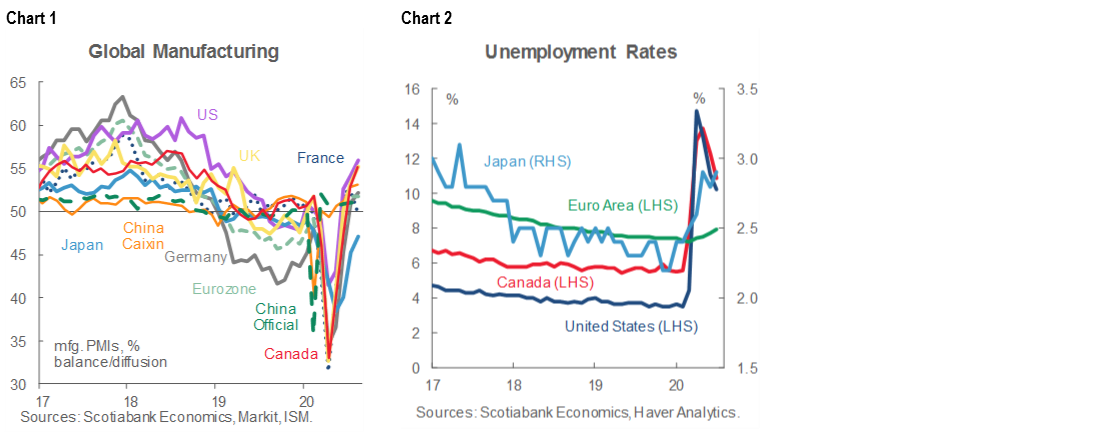

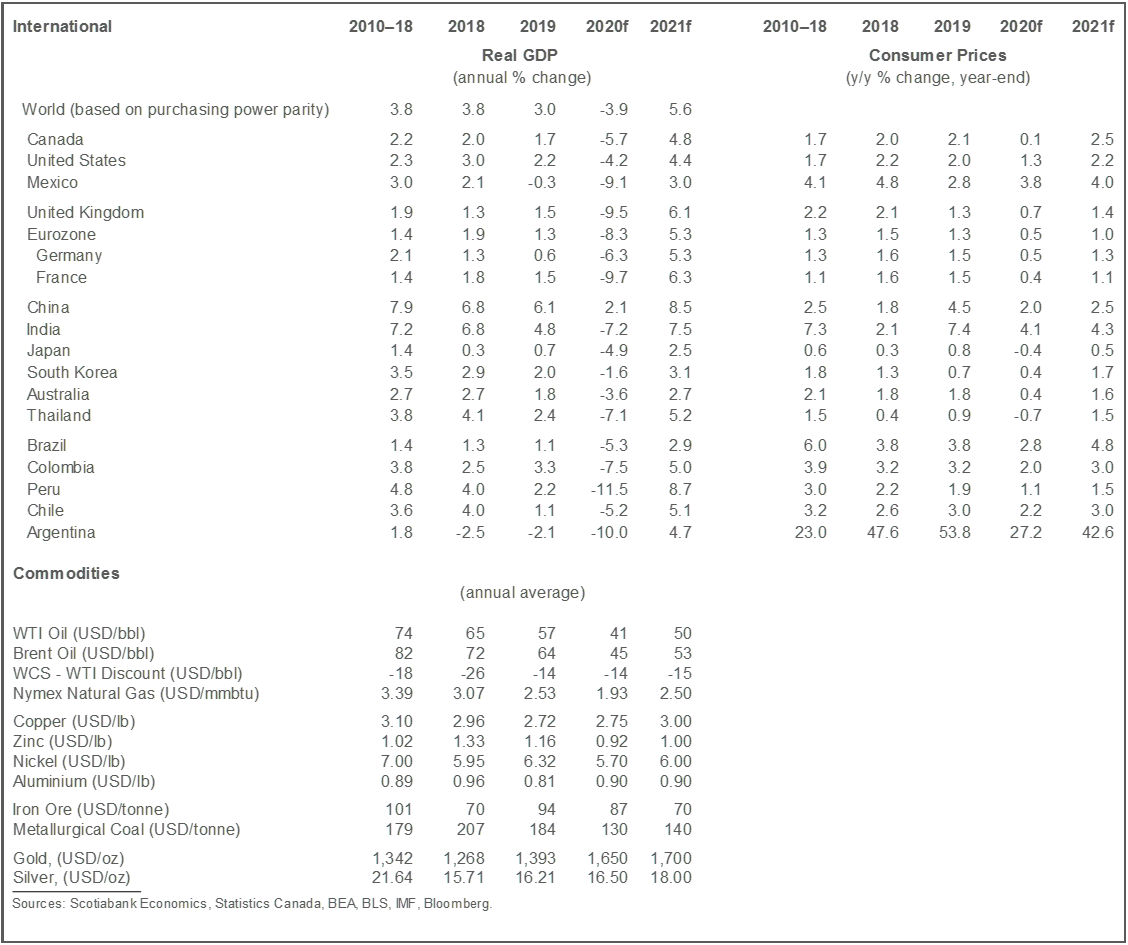

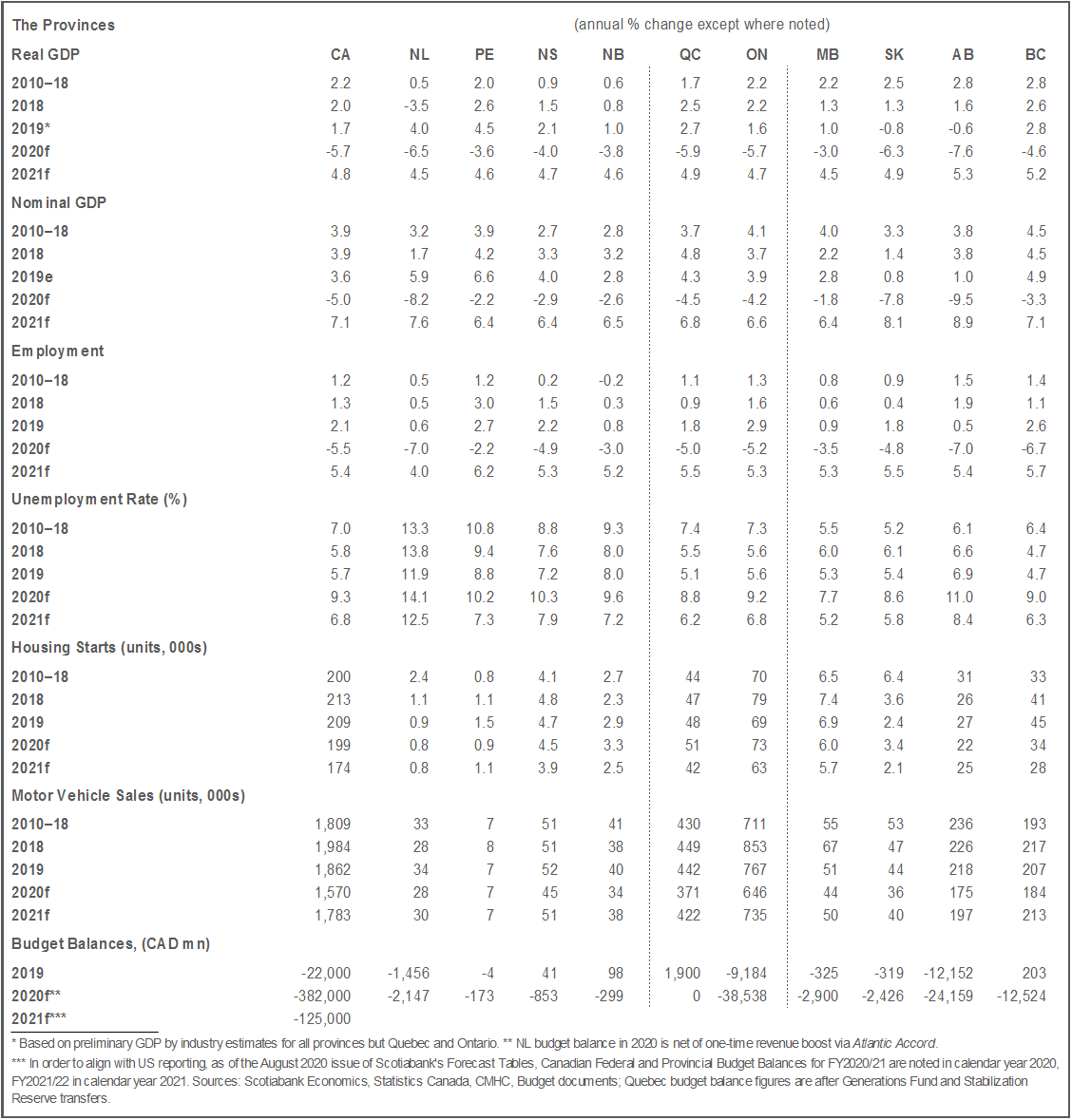

The global outlook for 2020 has improved markedly from the forecasts made at the peak of the pandemic earlier this year. Indicators of household spending and business activity (chart 1) continue to point to a more rapid and substantial rebound than earlier anticipated. Equity markets, facilitated by seemingly multi-year commitments by central banks to keep policy rates low, have reflected this strength, though gains tend to be concentrated in a few sectors. Despite this more positive turn of events, there remains real economic damage to undo, and this is perhaps most evident in labour markets where unemployment rates continue to be much higher than pre-COVID levels (chart 2). Economic activity remains well below pre-COVID levels and we still expect it will take a few quarters to recoup those losses. As this occurs, the economic adaptation will continue for sectors hit hard by the impacts of a more socially distant way of living. It is far too early to declare victory on this battlefront.

Risks remain tilted to the downside. The virus remains challenging to control as can be seen by the resurgence in many countries. We’ve incorporated some of these downside risks in our forecast, but there simply is too much uncertainty over the evolution of the virus and what measures may be put in place to deal with a rebound in the virus to properly account for that in a forecast. It is also increasingly obvious that non-virus risks remain important, notably in the US as we approach the final stretch of the election campaign. Civil strife, trade tensions and other, yet unknown but sure to happen, efforts by President Trump to sow discord in the hope of being re-elected all pose downside risks to the US and global economies.

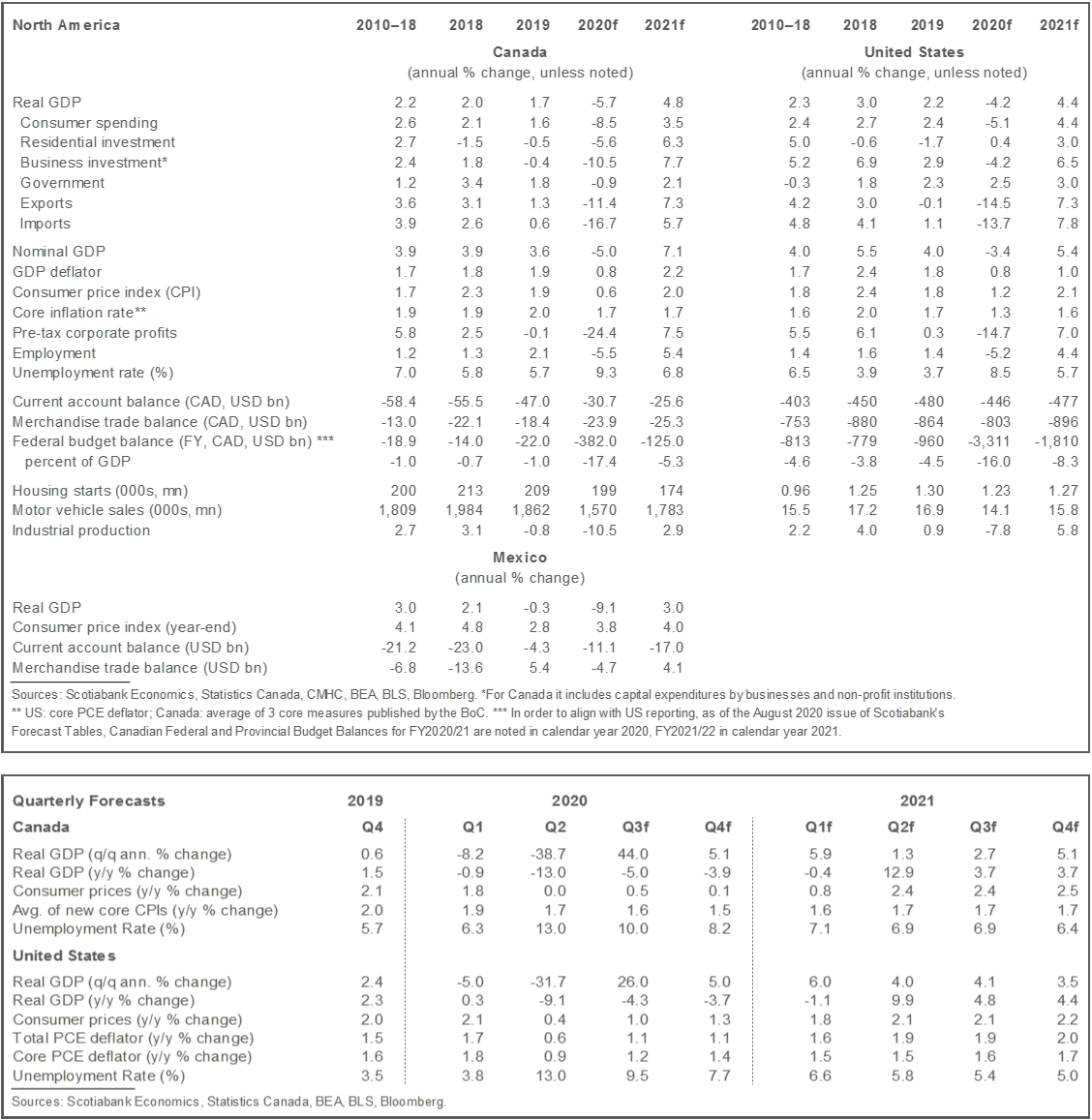

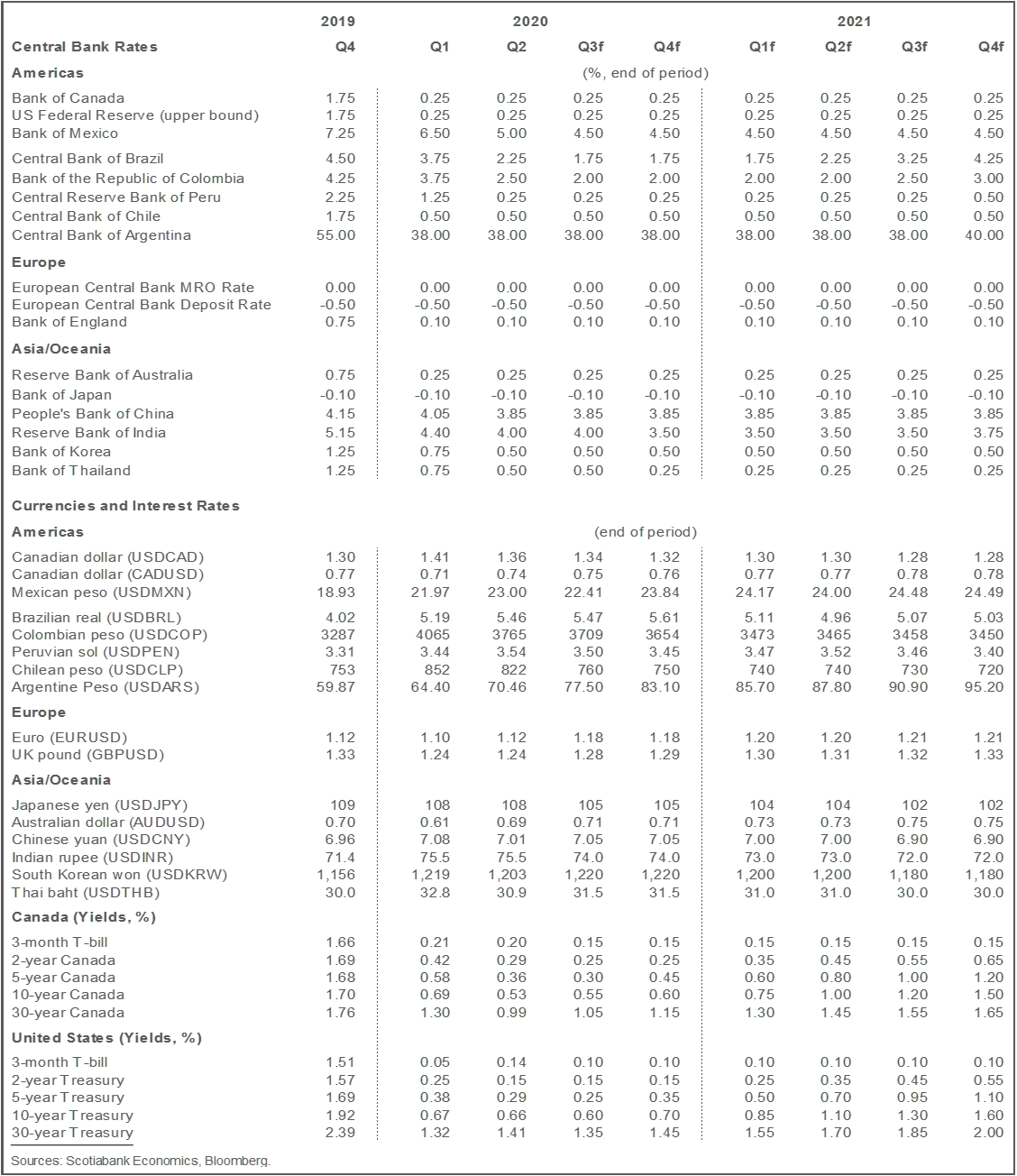

Incorporating recent data points and events into our view, the outlook for 2020 is a bit less gloomy than in our last forecast. The rebound in economic growth in the second half of 2020 is now expected to be stronger than we thought last time around, particularly in Canada and the US. In those countries, Canada looks set to experience more rapid growth than the US for the remainder of the year, though that reflects in large measure the rebound from more stringent lockdowns north of the border. While the inflationary impulse from the pandemic is still expected to be negative, some aspects of the supply shock’s impact on inflation are starting to come into view. Unit labour costs, for instance, increased sharply in Canada and the US (in Canada’s case, the most rapid increase in almost 35 years). As we await additional fiscal resources that might be deployed in a number of countries to further support firms and households, or to facilitate the post-COVID transformation of economies, it is clear central banks will, at a minimum, keep policy as stimulative as it is now for many quarters.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.