Global growth has been modestly marked down as COVID-19 roars back, but a solid recovery is still expected in 2021.

A more targeted approach to virus management should dramatically reduce the impact of the virus relative to the first phase.

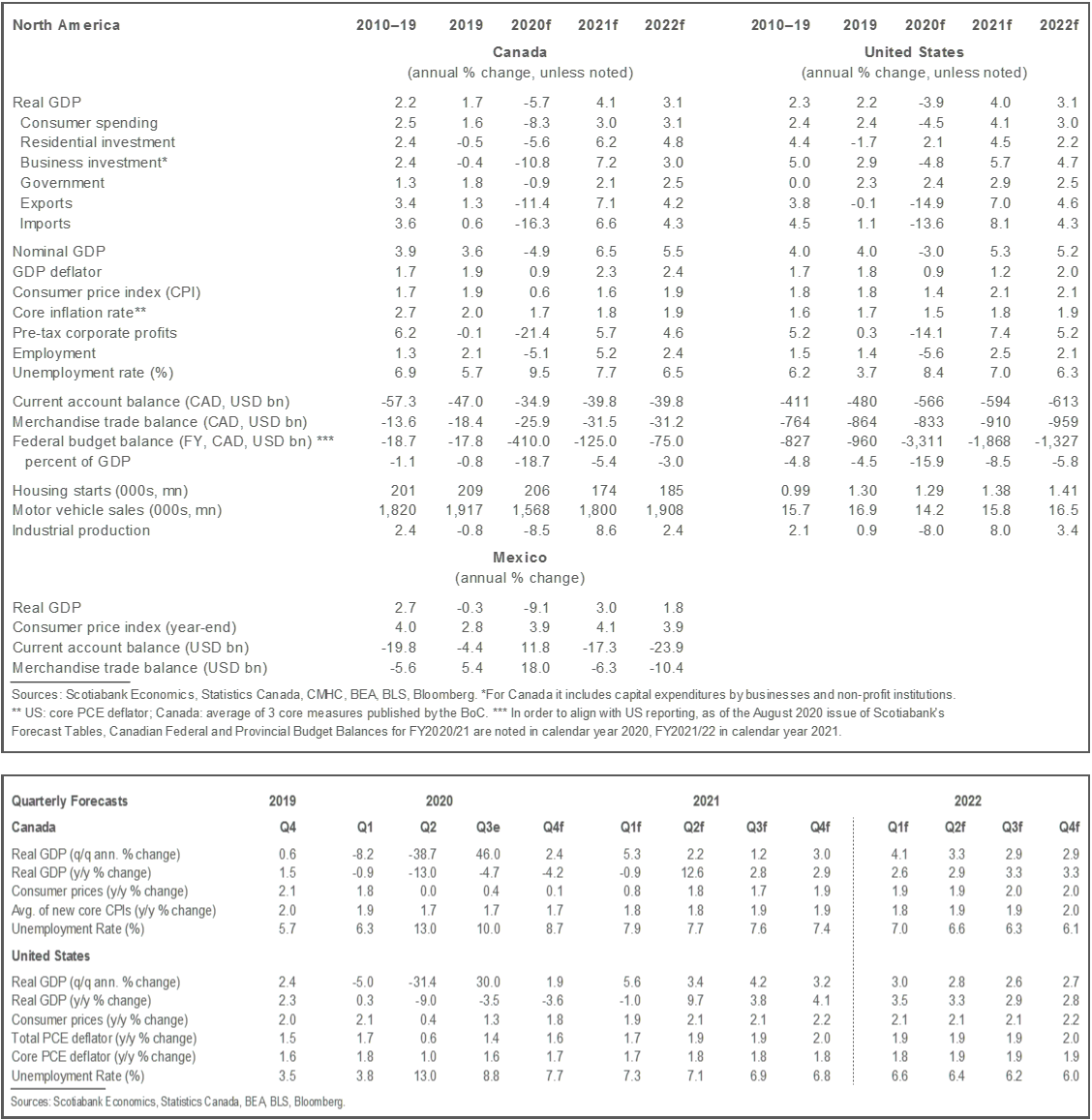

Economic repair from the effects of the pandemic may be occurring more rapidly in Canada than in the US.

The US election has the potential to substantially affect the forecast, but the extent to which this may occur depends critically on who wins the Presidency and controls the Senate.

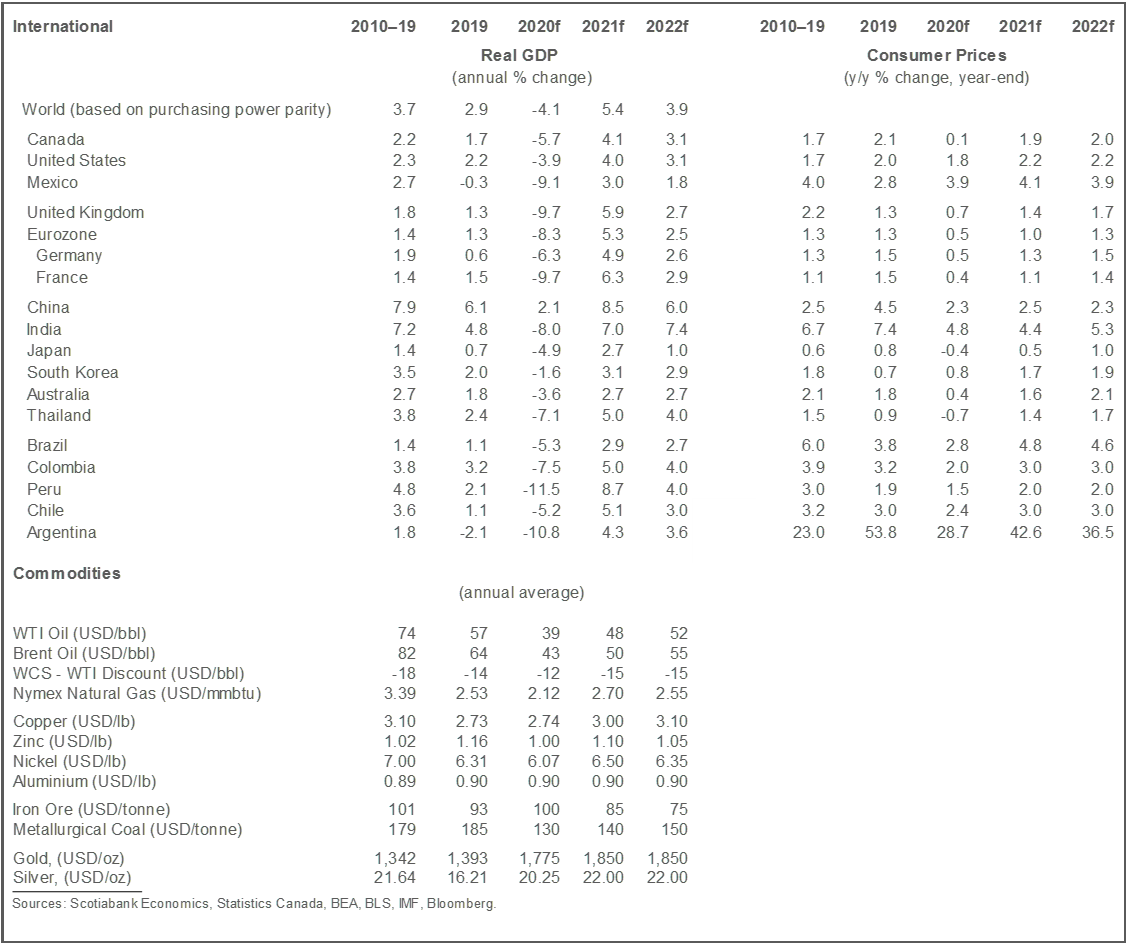

The sharp rise in COVID-19 cases is leading to a modest scaling-back of growth forecasts owing to markdown of near-term economic prospects, but a phase-1 like collapse of economic activity will be avoided. We currently expect global GDP to fall by 4.1% in 2020 and rebound by 5.4% next year. Our previous forecast was for a decline of 3.9% this year and a rebound of 5.6% in 2021. The rise in infections also serves as a stark reminder that downside risks to the outlook remain very high and that it will take many quarters to recover lost output. Sustained policy support remains essential to assist firms and households, and premature withdrawal of fiscal support, as seems to be occurring in the US, will slow the pace at which the global economy rebounds next year.

Policymakers seem to have taken the lessons from the first phase of the pandemic to heart. Though the virus has come back with a vengeance in many countries, as feared and expected, the response of authorities has been far more targeted and parsimonious. Full-scale lockdowns of economies have not been implemented even as this second wave seems more broad-based than the initial outbreak of COVID-19. Moreover, households seem better adapted to life in pandemic, though employment remains well below pre-pandemic levels. Global indicators of household spending, for instance, continue to point to a rebound in consumption.

The pace of the rebound observed in 20Q3 was never going to be sustainable, as it reflected a one-time boost in growth as economies re-opened from depressed levels of activity. We are now transitioning to a slower phase of the recovery, as the slow grind to return to pre-pandemic levels of economic activity continues. Unemployment rates remain well above pre-COVID levels with impacts disproportionately affecting low-wage service sector employees, and many industries remain under intense pressure. The pace of this transition will be dictated by the evolution of the virus, how governments respond to it, the extent to which business and household behaviour continues to evolve, and the nature of government supports.

In the very short run, we have scaled back our forecast for economic activity during 20Q4 and 21Q1. In the US this reflects lower fiscal support and virus-related drag, which will reduce growth in 20Q4 to 1.9% SAAR relative to the 5% we had forecast in our last update. In Canada, we now expect growth of 2.4% SAAR in 20Q4, well below the 5.1% we anticipated in our last forecast. This flows exclusively from the resurgence of the virus and containment measures instituted by some provinces. These revisions are partly offset in 2021 by the inclusion of extended wage subsidies and more generous employment insurance benefits, but growth next year is nevertheless expected to rebound less aggressively than previously assessed (now 5.4% vs 5.6% previously). There is likely to be upside risk to the amount of fiscal support provided next year given the Federal Government’s clearly expressed intentions in the Speech from the Throne. We will assess and incorporate new initiatives if they are announced in the upcoming budget.

Importantly from a Canadian perspective, it appears the repair from the impact of the pandemic may be occurring more rapidly than in the US. The number of full-time employees has recovered much faster in Canada than it has in the US, for instance (chart 1). This almost certainly reflects Canada’s more effective approach to managing the virus and its public health and economic consequences.

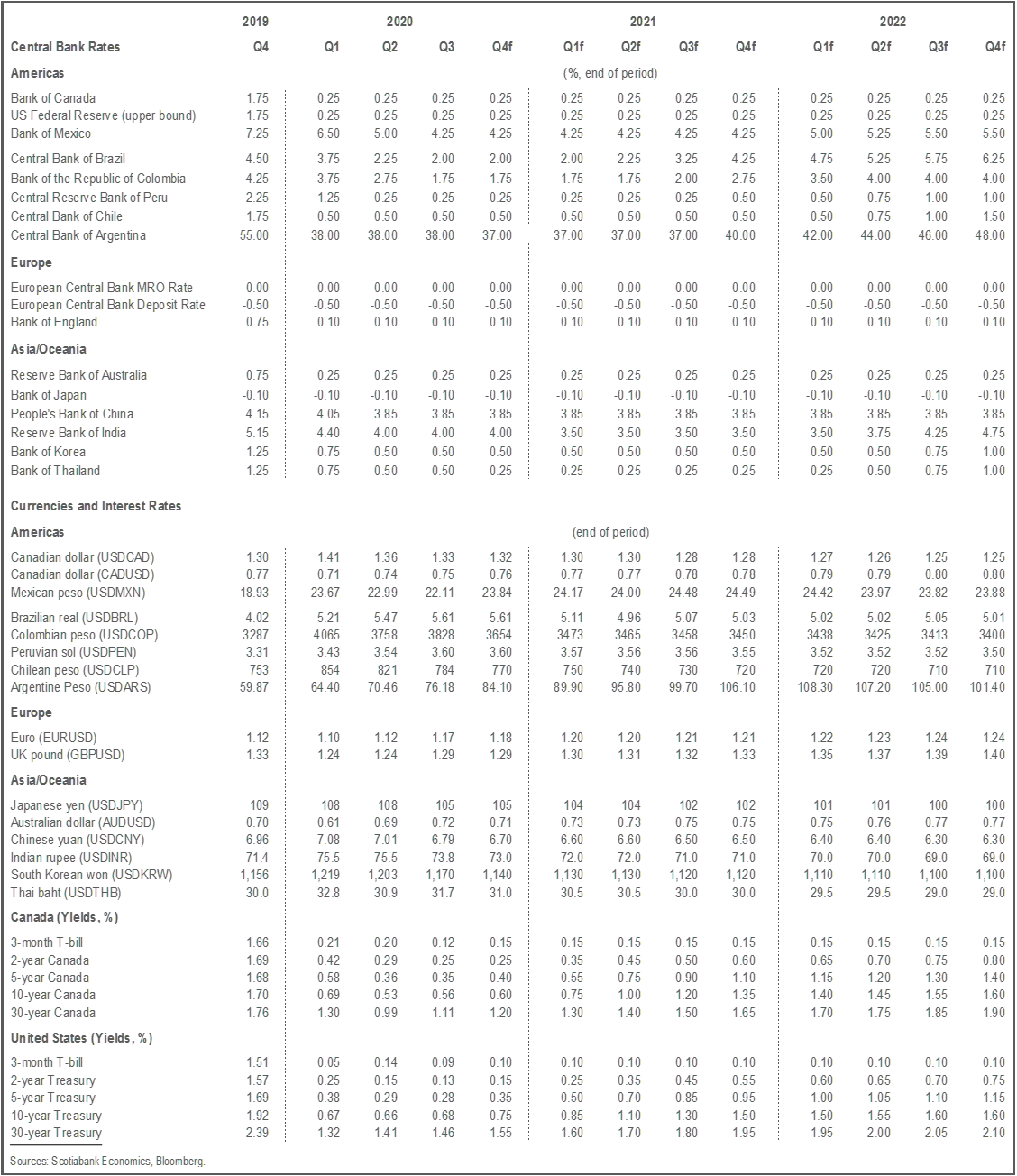

Our outlook does not incorporate the potential impact of the US election. It appears, at this point, that Mr. Biden will defeat President Trump. A President Biden, however, would be unable to alter the course of fiscal policy if Republicans maintain control of the Senate. In fact, it could well be that Senate Republicans block attempts by the new administration to support the economy as it continues to process the impacts of the pandemic. As Chairman Powell has noted many times, there remains a clear need for extensive fiscal support in the US economy. The current politicking around the extension of employment benefits is a taste what may come if Mr. Biden wins and the Republicans keep the Senate. If so, that would be negative for the outlook. Conversely, a Democratic Senate would likely be much more supportive of enhanced fiscal support, which could lead us to raise our forecast for next year. Finally, while President Trump seems unlikely to win at the moment, a victory is not out of reach. A second Trump mandate would likely see more fiscal support given the President’s newfound appreciation for stimulus. One thing is certain: the electoral distraction will be over soon, and a return to governing and a focus on the needs of the economy will be a welcome relief from the past few weeks.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.