Incoming data suggest a sharp rebound is underway in many countries though failure to control the spread in the virus in the US suggests the recovery in the second half of the year will be more muted.

Despite a V-shaped recovery in growth rates which should see strong growth for the remainder of the year and into 2021, the recovery will be long and painful for many sectors and individuals. A return to pre-COVID levels of economic activity is several quarters away.

Disinflationary pressures will be significant, as inflation responds with a lag to the decline in output. Policy rates in most industrialized countries are likely to remain at current levels through the end of 2022.

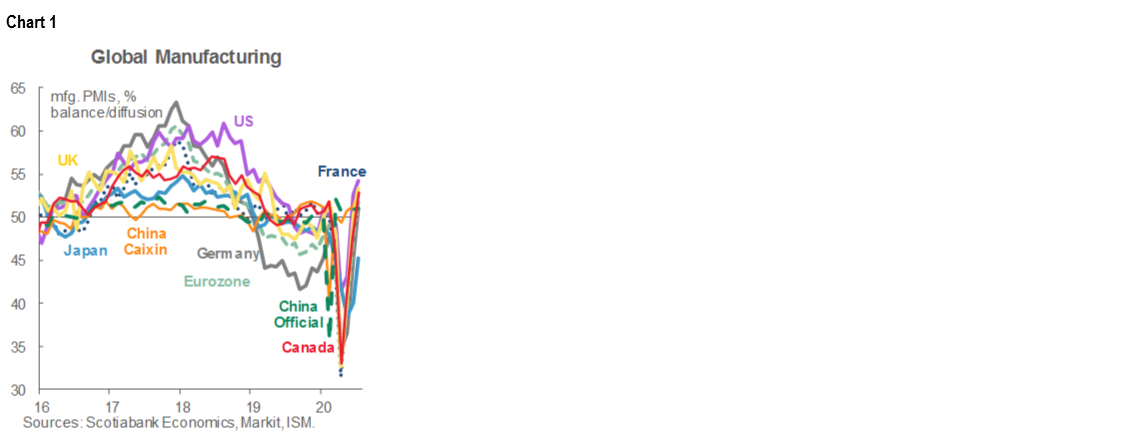

Though COVID-19 cases continue to rise globally, success in controlling the virus in some countries has allowed a relaxation of public health measures that have been so economically harmful. Across the industrialized economies for instance, economic indicators seem to confirm that a V-shaped recovery of growth rates is fully underway (chart 1). Those countries are in the easy phase of the recovery as spectacular growth rates flow from the re-opening process. To a varying degree, indicators of household or business activity suggest that a significant amount of COVID-related losses in output have been reversed. Markets have obviously been welcoming of these developments, but it is easy to overlook the fact that some of these losses will persist and that there are questions about the sustainability of the recovery once much of the re-opening process is complete. Levels of economic activity are expected to remain well-below those observed pre-COVID in many countries for quite a while. In Canada, for instance, we currently expect it will take until early 2022 to return to late 2019 levels of economic activity.

In countries where virus control has proven to be more challenging, such as some Latin American nations, the rebound is not yet underway despite policy efforts to attenuate the impact of the pandemic that are, for the most part, substantial. The dramatic increase in COVID cases seen in the United States—and to a lesser degree the evident ease with which the virus can re-establish itself as seen in many other parts of the world—are a stark reminder that the sharp rebound in economic activity observed at the moment across countries is acutely vulnerable to virus-related developments. So important are these downside risks that our forecasts for Canada and the US in 2020, for example, have remained roughly unchanged even though second quarter data and early third quarter data have generally been stronger than our expectations as we scale back the extent and speed of the rebound for the remainder of the year.

Compounding the health risks are policy risks in the United States. It is clear President Trump is embarking on a more confrontational path across several areas. Of most immediate concern, a premature withdrawal of policy support—such as may occur if the supplemental unemployment insurance payments were to be scaled back—risks damaging what is not yet a self-sustaining recovery. For the moment, we assume those benefits will be extended as-is for as long as needed, but if that were to change, as seems possible this week, we would reduce our US forecast accordingly.

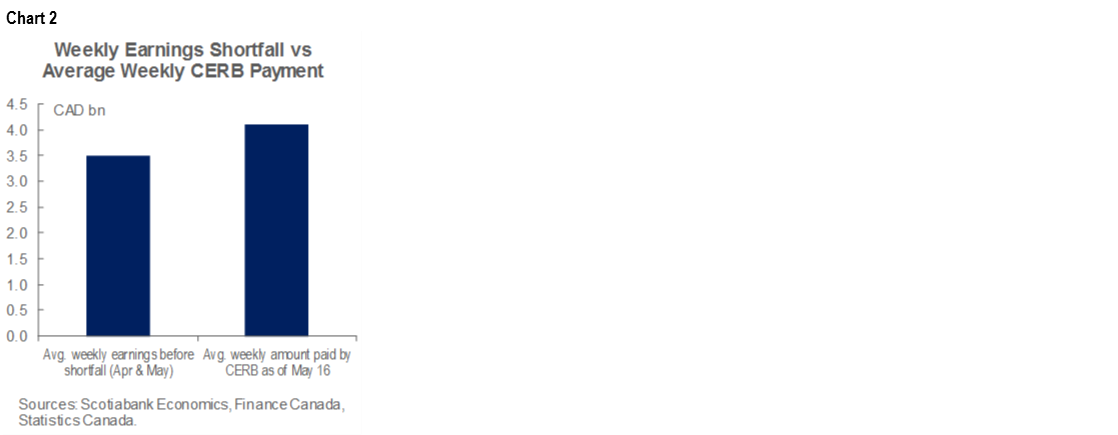

From a Canadian perspective, incoming data are clearly indicative of a very sharp improvement in economic activity even as many sectors are still struggling. This is most evident in the household spending data, with retail sales having returned to pre-COVID levels, though the composition of those sales is clearly very different as some sub-sectors (general merchandise and food stores) are significantly above pre-virus levels, while a number of others remain well-below February levels. Auto sales have rebounded powerfully, a combination of pent-up demand, but also reflecting greater interest in purchasing cars post-COVID. This is no doubt linked to surveys showing less desire to take public transit. Developments on the consumer spending side likely reflect an impressive resilience in household finances despite a sharp increase in unemployment. This likely flows from the emergency income support from the government (chart 2), reduced childcare expenses, the various deferral programs offered by financial institutions, the strength of house prices, and the very strong rebound in equity markets observed.

Despite the rebound in some market-based measures of inflation expectations, inflation appears likely to remain well below central banks’ targets in countries where those exist. The Canadian example is indicative of developments globally. The shock to the level of output is so large that, even if we accept that much of it results in lower supply, the output gap will widen sharply, putting downward pressure on inflation. Of course, the relation between output gaps or other measures of economic activity and inflation, is captured in the Phillips Curve and there is some debate as to how well that relation is holding up. In Canada, our estimated Phillips Curve has held up quite well in recent years, as has that for the US, though that curve has never worked as well as it is has in Canada. As there is a lag between a deterioration of the cyclical position of the economy and inflation (around a year in our model), the fact that various measures of trend inflation remain around 2% in Canada should not be interpreted as proof that inflation will remain at target, or even rise from current levels. Core inflation is only expected to return to the Bank of Canada’s target by the end of 2022.

Given our assessment of disinflationary pressures, policy rates in industrialized economies should remain at current levels for an extended period of time. Rates will not rise for many quarters. In the US, Chairman Powell indicated that the Fed has not even begun to think that they should begin thinking about higher policy rates. In Canada, the Bank of Canada has returned to Carney-era forward guidance by categorically committing to maintain its policy rate at current levels until inflation is sustainably at its target. If our forecast is accurate, that wouldn’t be until 2023. Moreover, if additional policy support is required, both central banks have indicated that they would not consider negative interest rates, but rather consider means to lower interest rates further up the curve, possibly by following Australia’s experience in yield curve control.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.