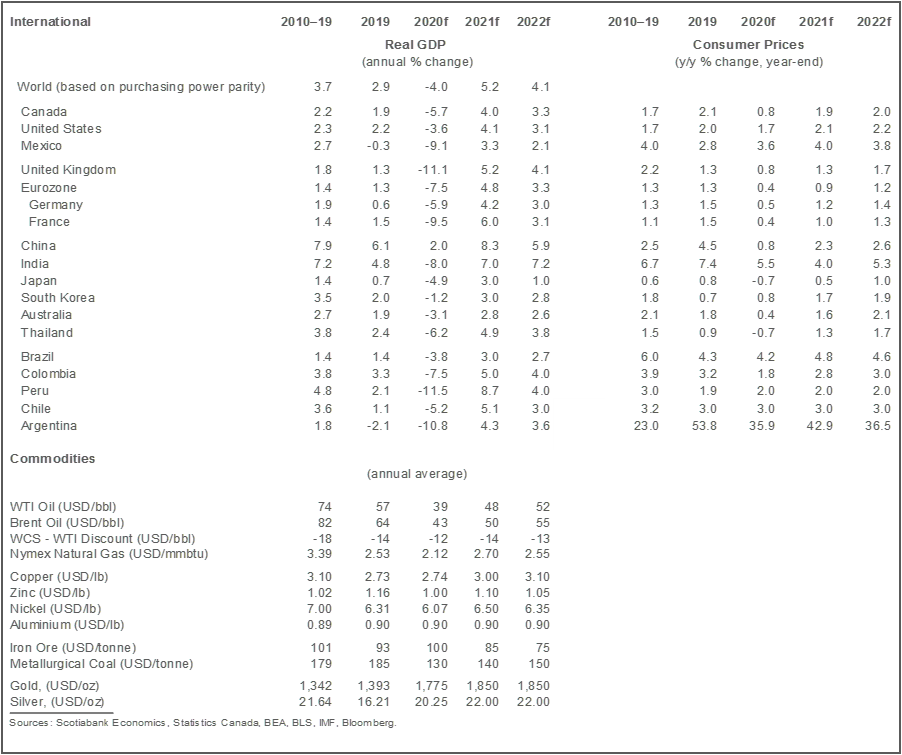

The resurgence in the virus will result in weaker growth this quarter and next, but its impact on full-year forecasts of 2021 will be largely offset by the arrival of the vaccine and likely additional fiscal stimulus in the US.

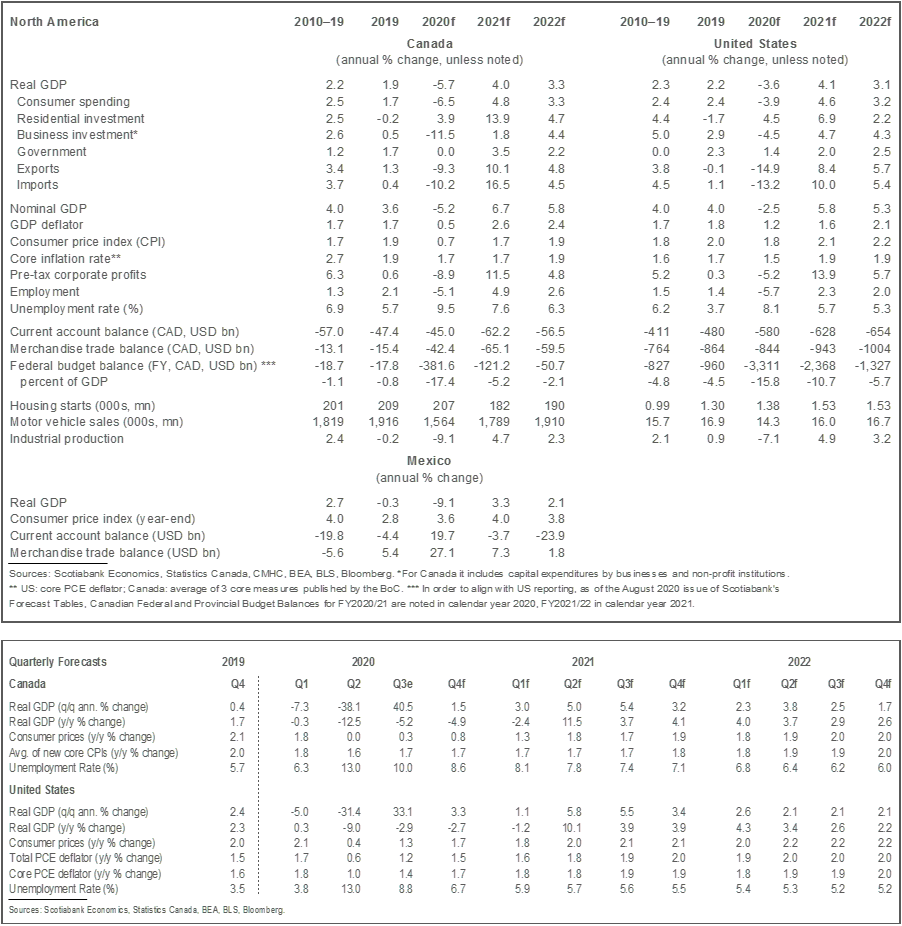

In Canada, we continue to expect a solid, though slightly delayed, recovery next year. We forecast a significant acceleration in growth when the vaccine rolls out and uncertainty dissipates given the large amount of cash held by firms and households. However, it will take time for some sectors relying most heavily on social interaction to recover fully.

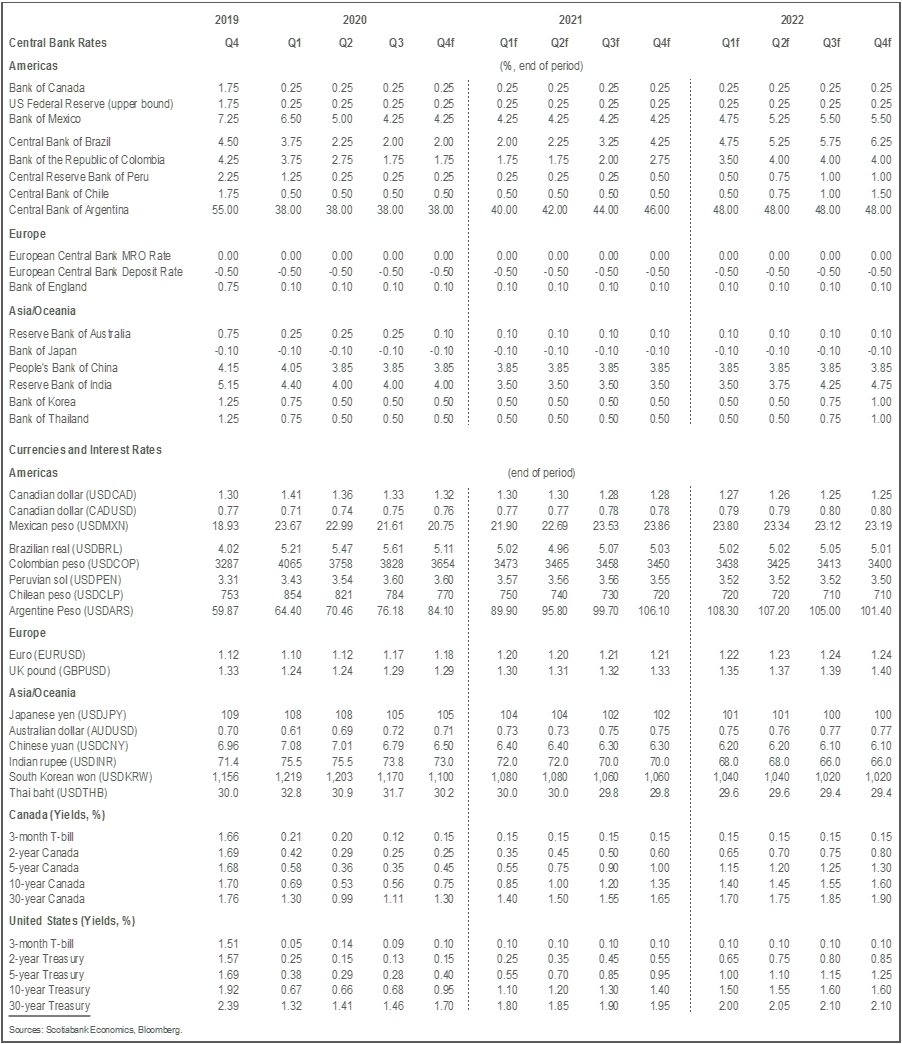

Policy rates are still expected to remain at current levels until 2023 but the stickiness of inflation and the potential impact on costs of the eventual unwind of business support measures could lead to rising inflation expectations. If so, we may need to adjust our view on the timing of the next move by the Bank of Canada.

The dominant influences on forecast revisions over the past few weeks have once again centered on the pandemic. On one hand, the resurgence of cases in many countries, as generally expected, is a blow to the near-term outlook. Though containment measures are generally far more focused than those rolled out in the first phase, the measures and concerns over the spread of the virus will lead to slower growth in the next couple of quarters. On the other hand, news on the vaccine front has been very encouraging and we anticipate that we will overcome the virus next year. That has sparked a further rally in financial markets and substantial moves to add risk to portfolios. On balance, despite the worries around the current state of the pandemic, it appears clear that we are on the cusp of turning the corner on COVID-19.

Adding to this optimism are the impact of the Biden victory in the United States and implications for further fiscal support. It now appears the Republicans and Democrats are close to a deal on extension of a range of fiscal supports. President-elect Biden is indicating these are only down payments on what he plans to move on. The extent of further support will depend in large measure on the Georgia Senate run-off and who ultimately will control the Senate. Again, financial markets have responded quite positively to these possibilities. Our forecast only incorporates about USD 500 bn in additional support next year—well below the levels being currently considered—so there is potential upside there.

Taken together, recent developments continue to suggest a solid recovery will unfold next year, though it may be delayed by a quarter relative to earlier views. From a Canadian perspective, the near-term outlook has worsened owing to COVID-19, but measures announced in the Fall Economic Statement, along with the vaccine, and the strength of house prices should lead to a sizeable jump in economic activity in the second quarter and beyond. We expect large holdings of cash will be drawn down as Canadians become more confident that the pandemic will be controlled, and that job and health-related risks will fall. For the first time since the pandemic began, risks for the next year appear tilted to the upside given the vaccine, the potential for a stronger-than-expected US economy, the likelihood of additional fiscal measures in the Spring Federal Budget, and the ongoing strength of the housing market.

Even if upside risks materialize in 2021 and growth is stronger than currently expected, significant sections of the economy are under intense financial stress and are likely to only gradually return to pre-COVID levels of activity. As a result, we believe the unemployment rate will continue to fall but remain above pre-pandemic levels until the end of 2022. Moreover, a number of firms are likely to struggle through the year as support measures such as the wage subsidy and rent relief program are rolled off (if that occurs…).

We continue to expect policy rates will remain on hold through 2023 in Canada, but our conviction on that call is fading. Inflation in Canada has not fallen as much as anticipated as the core measures of inflation have averaged around 1.7 for a few months now. As we look to the next twelve months, it may well be that input cost pressures accelerate owing to pick-up in commodity prices, but also due to the unwinding of business support programs, and lower potential output. At present, wage subsidies and rent relief programs are without any doubt allowing firms to keep prices down relative to what would otherwise be the case without these programs. Inflation data for the third and fourth quarter of next year will be key to informing views on how businesses respond to lower financial assistance. Moreover, the rapid increase in the money base here and elsewhere is expected to have mildly inflationary consequences, which is, of course, a key reason for central banks to have undertaken their quantitative support programs. The risk, as we see it, is that these programs—combined with higher commodity prices and an unwinding of business support programs—lead to a rise in inflation expectations which could trigger a more rapid increase in inflation and a faster increase in policy and market rates. We will be paying very close attention to measures of inflation expectations in coming months, as will, we suspect, the Bank of Canada. For now, we are sticking with our policy rate call of no change until 2023, but we do expect the yield curve to steepen gradually well ahead of that, as has been our forecast for many months now. That process is already under way.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.