SPEND LIKE THERE IS NO TOMORROW, TAX LIKE THERE IS

- Canada’s federal Finance Minister tabled Budget 2024 on April 16th. Gross new spending measures were substantially higher than signalled ahead of budget day, with equally substantial taxation measures partially offsetting the net impact.

- The budget adds a near-term boost to growth with major new spending, but it introduces another twist as it gives with one hand while taking with the other. While net new spending amounts to 0.4% f GDP over the next two years, gross outlays to Canadians adds up to a much more substantial $22.5 bn (0.7%), while syphoning off $9.5 bn from drivers of growth. This is additive to the $44 bn incremental spending provinces have announced in recent weeks.

- The budget clearly makes the Bank of Canada’s job more difficult. The soft inflation print released into the budget risks fanning complacency around the risk of a resurgence in inflationary pressure particularly with a housing market rebound waiting in the wings (and more potential buyers on the margin after this budget).

- New spending is hardly focused. A gross $56.8 bn is spread widely across a range of “priorities”. The new Housing Plan reflects ‘just’ 1/6th of new outlays. Others were channeled ahead—military spending, AI investments, and pharmacare—while new pledges were tabled towards Aboriginal investments, community spending, and a new disability benefit among others.

- New tax measures will yield a $21.9 bn offset—notably a big increase to the capital gains inclusion rate from one-half to two-thirds for individuals and corporations later this Spring.

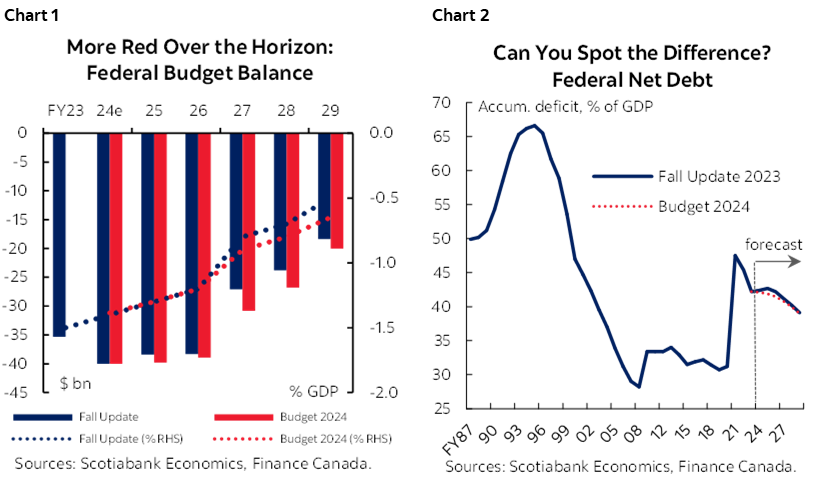

- The net cost of new measures in this budget lands at $34.8 bn over the planning horizon. Near-term economic momentum has provided additional offsets ($29.1 bn), leaving the fiscal path broadly similar to the Fall Update. The FY24 deficit comes in on the mark at $40 bn (1.4% of GDP) and is expected to descend softly to $20 bn (0.6%) by FY29 (chart 1). Debt remains largely on a similar path of modest declines as a share of GDP over the horizon (chart 2).

- The fiscal plan could have delivered on critical priorities including the Housing Plan, along with AI and Indigenous spending, while still adhering to its fiscal anchors without resorting to substantial new taxation measures that will dampen confidence and introduce further distortions to Canada’s competitive landscape.

- It won’t likely trigger an election, but it is clearly a warm-up lap as Canadians brace for the polls within the next 12–18 months. The taps are unlikely to be turned off any time soon.

A CALCULATED (AND COSTLY) RISK

Canada’s Budget 2024 left some surprises for game day on April 16th. There was substantially more spending announced in the budget on top of what had been spoon-fed ahead of budget day, while an equally-big tax package is headline-grabbing. Budget 2024 delivered just that with another major spending package amounting to $56.8 bn, offset in part by a bit of economic luck ($29.1 bn) and a lot more taxes ($21.9 bn) over the planning horizon (FY24–29).

This budget is not expected to trigger an immediate election, but it floats the trial balloon. All of the conditions to keep the Liberals in power until October 2025 had been met earlier this year (under the Liberal-NDP agreement). This budget goes big once again despite a waning economic outlook over the horizon—and perhaps with some false confidence in the inflation and interest rate paths ahead—suggesting they hope to tilt polling numbers in their favour sooner rather than later. Their current fiscal anchors don’t leave much space for another pre-election budget.

A KITCHEN SINK BUDGET

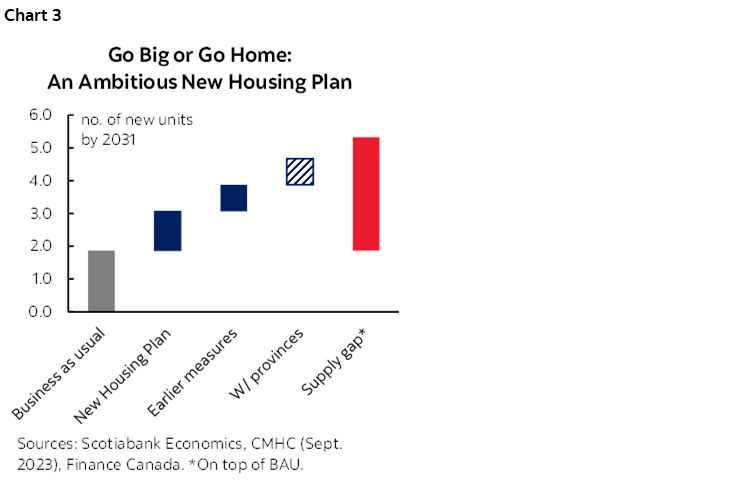

The new Housing Plan should have been the centrepiece of the budget. It had been released in dribs and drabs in the weeks ahead, with the budget revealing a final price tag of $8.6 bn (or only 1/6th of the full budget spend). The housing plan is ambitious with an aim of unlocking 3.87 mn homes—or 2 mn above baseline projections—by 2031, while potentially paving the way for another 800 k if provincial counterparts step up that could make meaningful progress on narrowing housing supply gaps over the medium term if implemented (chart 3). With recent-year housing starts hovering between 200–300 k annual units and an implied build rate of 550 k annually under this Plan, there is much work (and risk) ahead.

The new Housing Plan is also comprehensive. Nearly two dozen line items target a range of issues from building greater rental supply, removing regulatory hurdles, modernizing the construction industry, securing the right workforce, supporting housing-related infrastructure, improving rental market conditions, and revitalizing non-market or community housing to name a few. The spend is widely distributed across government and non-government players with few details yet on metrics for (early) evaluation or relative value for money. Given already ramped-up federal investments in housing have been overshadowed by market conditions (among other factors), it will be important to monitor the fed’s ability to leverage private capital towards its goals (chart 4).

The Plan will likely fuel incremental demand for home ownership on the margin. Though narrow in scope, measures such as longer amortization for first time home buyers and increased withdrawal limits to the Home Buyers’ Plan would reinforce purchasing power among some segments of the population and the timing could further fuel housing market rebounds. This could pose a significant headwind to the Bank of Canada’s first rate cut with a good chance it underpins a surge in activity ahead of August implementation.

These demand-side channels are a pragmatic acknowledgement that trend price growth may decelerate with greater supply under this plan but prices are not likely to decline. Longer amortization would better match younger buyers’ income-earning lifespan, though may make OFSI’s job trickier with relatively novel age-based lending restrictions. It may only be a matter of time (and the budget acknowledges this) before there is a broader-based shift towards longer amortization periods for all insured homebuyers. Carefully crafted and on the other side of inflation risk, this could redirect cash-flow (and capital) into more productive sectors of the economy, but only coupled with supportive growth policies that offer attractive alternatives. This budget falls short in position housing in the context of Canada’s broader productivity landscape.

THE LEAKY FAUCET

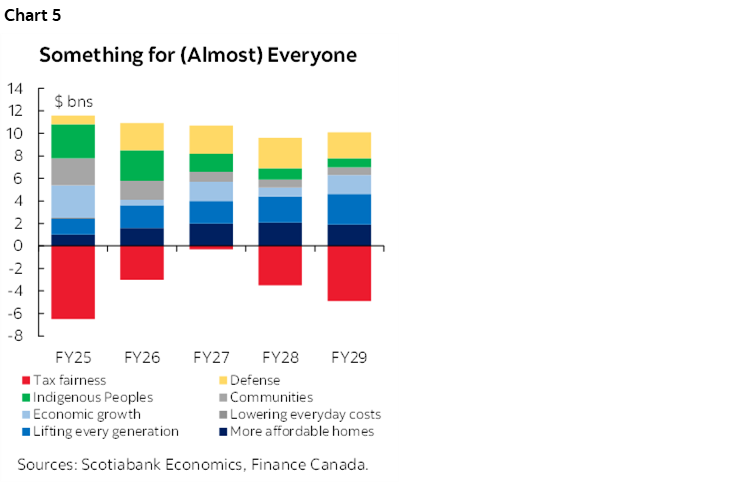

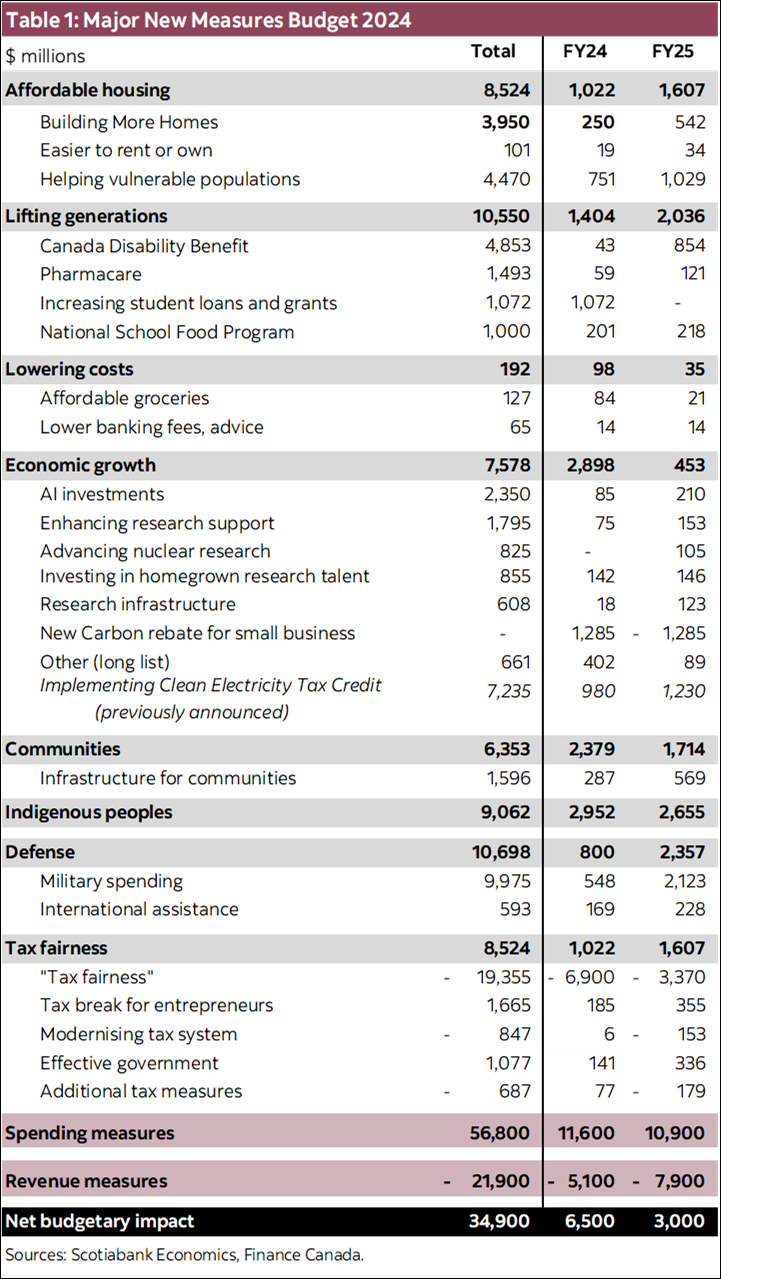

The budget doesn’t stop there. Another $44.4 bn is spread across a range of other measures (chart 5). This includes ramped up military spending ($9.9 bn), Indigenous investments ($9.0 bn), community investments ($6.4 bn), the new disability benefit ($4.8 bn), and pharmacare spending ($1.5 bn). There is also an “economic” growth chapter tallying $7.6 bn over the horizon, including AI ($2.4 bn) and a range of research-related investments ($4.0 bn). (Table 1, at the end, provides a snapshot of some key measures but the full lists are exhaustive.)

To pay for the new spending, the government announces a substantial increase to the capital gains inclusion rate. The inclusion rate will be increased from one-half to two-thirds on capital gains realised annually above $250 k by individuals and on all capital gains realised by corporations and trusts. This is costed at $19.35 bn over the planning horizon before a $1.7 bn carve out for entrepreneurs. A tobacco tax provides another $1.7 bn in revenues, with net revenue-generation measures amount to $21.9 bn.

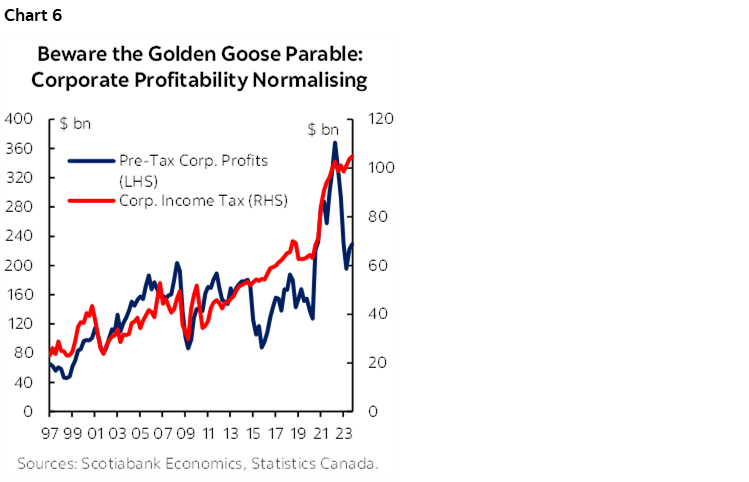

Today’s revenue-raising measures would shift a substantial sum in corporate capital to government balance sheets at a time when it is essential private capital is crowded in to ultimately deliver on major ambitions around housing and the green transition. This may prove to be shortsighted and a high-risk strategy in an environment of low productivity and waning economic drivers. The government continues to take a punitive approach to corporate taxation despite waning momentum in profitability and compressed margins against persistent inflationary (and relatedly-wage) pressures (chart 6). Repeated interventions also introduce distortions across sectors, heightening the costs of resource misallocation and undermining the attractiveness of Canada’s business landscape.

The net cost of budgetary measures comes in at $34.8 bn over the horizon.

GOOD LUCK (& GOOD PLUMBING)

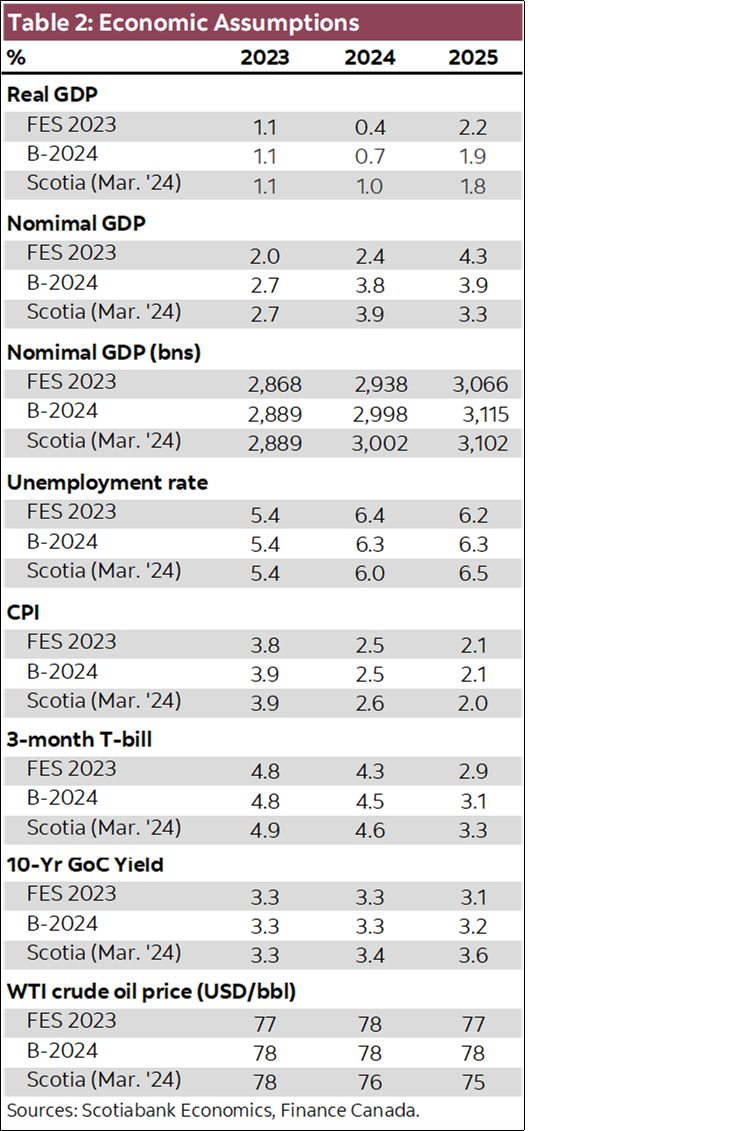

An improved economic outlook provides a decent offset to new spending. Nominal economic growth has been substantially stronger than the official outlook last Fall (with a 1.4 ppts upward revision for 2024). Real growth of 0.7% and 1.9% are penciled in for 2024 and 2025 leaving some more room for upside this year. While some growth is pulled forward, nominal output would still sit 1.6% higher over the horizon. There have only been marginal changes to near-term inflation and interest rate outlooks (table 2, at the end). Net revisions offer $29.1 bn in incremental fiscal savings over the horizon.

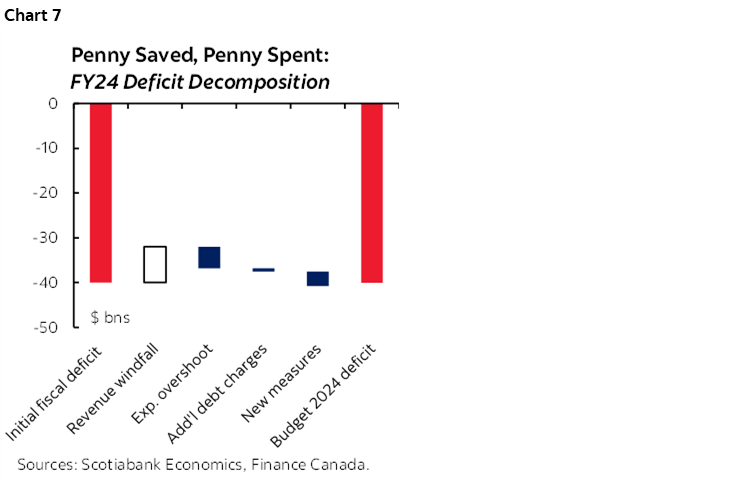

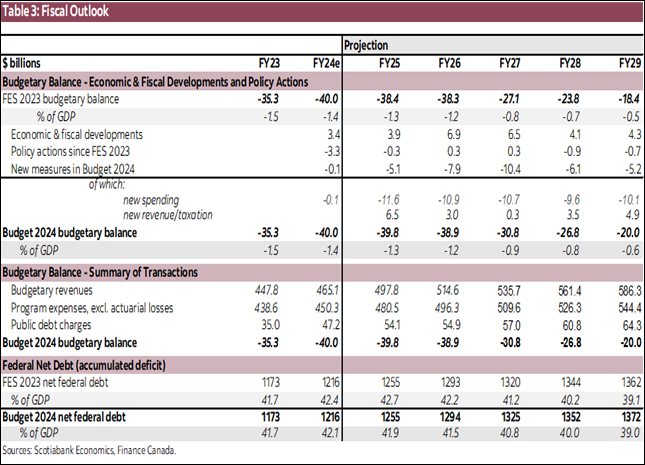

The plan adheres to its fiscal targets. Recall, the Fall update set out a range of anchors: deficits at or below $40.1 bn in FY24, declining as a ratio of GDP in FY25 and beyond, and below 1% in FY27 and beyond. It had also pledged an FY25 debt ratio lower than 42.7% and declining thereafter. The fiscal path meets these goal posts, while also exemplifying the perversity of their construct where stronger economic growth procyclically enables more spending. Absent recent economic tailwinds, the government would have blown through its first fiscal check-point (chart 7).

Persistent deficits are here to stay. The descent is marginally softer than earlier projections with an estimated 1.4% (of GDP) shortfall in FY24 declining to 0.6% by FY29. Denominator effects, namely, a stronger GDP profile does most of the work as budgetary needs climb by $10.2 bn over the horizon relative to the Fall update.

The debt outlook still expects to resume its soft downward descent. Net federal debt is estimated at 42.1% of GDP in FY24 (marginally better on the back of stronger GDP growth) and continues to drift downward thereafter landing at a projected drifting 39.0% by FY29 (table 3, at the end).

PLUMBING BACKUP

This budget adds a pretty big dollop of additional spending in the next two years that is masked in net terms. Namely, the budget provides about $22.5 bn over the next two years in gross outlays to Canadians while syphoning off $9.5 bn in revenues, mostly from drivers of growth and sources of private capital essential to a much-needed rotation to business-driven economic activity. It is added to the $44 bn in incremental outlays announced by provinces in recent weeks over the same horizon. The give-and-take calculations in the federal plan will no doubt further complicate the Bank of Canada’s interpretation of the net impact on near-term demand as it stimulates some sectors and dampens others. On balance, the larger bottom line is likely larger than anticipated.

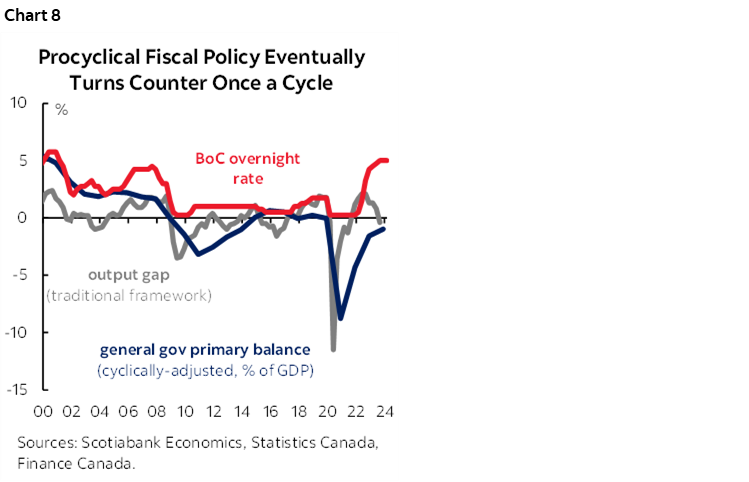

This also comes on top of $87 bn allocated federally since Budget 2021 for these same years. The net impact is accommodative fiscal policy running countercyclical to economic conditions (i.e., where an output gap signalling excess demand) for over two years now (chart 8).

Market watchers will—or should—be guarded against these incremental developments. Recent upward revisions to the expected impact of government spending by the Bank of Canada (to 0.7 ppts this year against a real GDP outlook of 1.5%) do not yet incorporate new federal spending. It has been explicit that government spending compounds ongoing challenges to bringing inflation (and inflation expectations) on a firm path back to target. There is a risk of complacency around upside risks to that path with another soft inflation print released hours ahead of the budget’s release fueling further market pricing of a June cut. This budget further reinforces Scotiabank Economics’ view that this would be premature. Continued fiscal support—amplified in this budget—adds to the risk of a premature rate cut and/or puts a floor under the pace of its descent thereafter.

Looking through near-term market implications, the longer term outlook paints a mixed picture. This budget—and earlier ones—have launched a slew of laudable policy measures aimed at structural bottlenecks (think, housing and related-infrastructure) and growth opportunities (think, the green transition). These packages have been big and bold in areas where the potential costs of inaction are high. But their success importantly hinges on crowding in private sector participants, and cajoling provincial counterparts to the table.

Execution risk is high. A burgeoning public sector (to deliver growing direct program expenditures) risks crowding out the needed rotation to private drivers of growth, while a largely punitive approach to corporate Canada does not help. This budget further reinforces these risks. Results and accountability frameworks should be front-and-centre with early signs for course-correction where warranted but these have not (yet) been newsworthy.

HOLDING YOUR NOSE

Greater bond supply will be issued into global markets very much focused on near term interest rate outlooks. Budget 2024 sets out borrowing plans for FY25 with a target bond issuance of $228 bn -12% higher than last year’s $204 bn but a decelerating from recent issuance activity with changes to non-budgetary drivers less substantial than anticipated. More importantly, a reassessment of interest rate risk south of border has overwhelmed fiscal signals at home in the near-term.

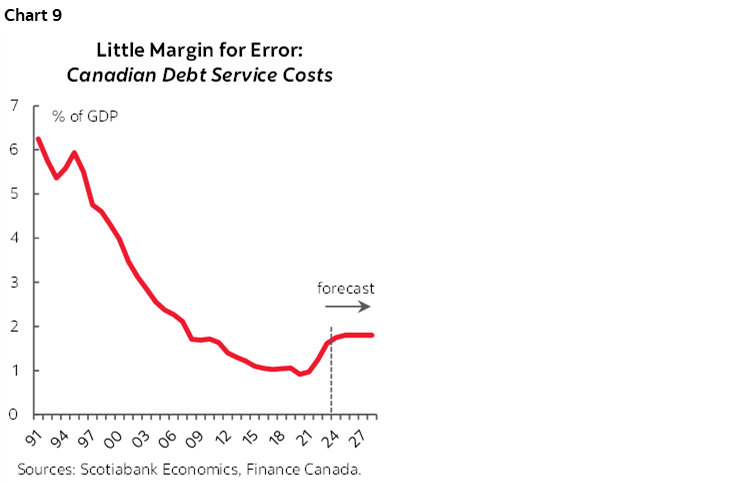

There may be complacency on the path ahead for interest rates. Canada’s 10 year bond yield has come down from last year’s peak north of 4%, sitting only modestly above expectations in this budget. However, it projects long term rates returning closer to 3% by next year. Forecast undershoots, along with higher spending, add $11.9 bn to debt servicing costs over the planning horizon. Debt service as a share of output is still expected to stabilize at a still-low 1.8% of GDP (chart 9) but that looks precarious against anemic economic potential over the medium term and a recently revised higher neutral interest rate.

Debate over appropriate debt levels arguably distract from the urgent debate needed on drivers of growth and productivity. Canada’s relative debt levels at the general government level—important to markets given Canada’s highly decentralized federation and implicit federal backing to sub-sovereigns—are pretty good or at least pretty benign (charts 10 & 11). Net debt metrics may overlook liquidity constraints and the lack of reserve-currency cushions in near-term crises, but gross debt comparisons undervalue unfunded public pension plans across most other comparators that is important over the long run as aging demographics catch up.

Canada has the space (albeit narrowing) to undertake targeted investments to unlock stronger growth, but if and only if it actually unlocks stronger growth. Much of the spending in Canada, especially at the provincial level, but also at the federal level over the past several years, fails this test. Spending has mostly rotated from transfers to alleviate immediate cost of living pressures to stop-gapping structural imbalances (from bloated public sector wage bills to paying for growing government programs to playing catch-up with demographic demands). This budget is no different in acting on the urgent, but not yet getting to the heart of the important. Despite an array of laudable measures, the sum of the parts do not yet add up to a credible productivity agenda that would lift living standards over time for all Canadians.

COMING SOON

This budget lays the foundation for a heightened and potentially prolonged election season for Canadians. A relatively benign outlook underpinning the budget leaves little room for surprise (pie-in-the-sky thinking on the eve of US elections?), nor does it leave much space for costly campaign platforms under current anchors. But it is reasonable to assume policy (and fiscal) resets at election time—or crisis mode—under the current or new government. Let’s hope all parties find a compelling and digestible way of bring growth and productivity back to the fore in Canadian discourse and in a meaningful way to all Canadians. Only this will secure better living standards for all Canadians over time.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.