THE ART (AND MATH) OF GIVING AND TAKING

- Canada’s Federal 2022–23 Budget unleashes more spending, masked by major revenue windfalls and new revenue-raising measures.

- New spending measures tally $56.6 bn by FY27, ticking off the boxes on many of the Liberals’ election pledges on housing, healthcare, and green investments, along with some under the recent Liberal-NDP pact including a national dental care program (though there is a notable absence of pharmacare).

- Revenue windfalls since the Fall Update amount to a whopping $85.5 bn by FY27. Meanwhile, new revenue-raising measures—including the anticipated taxes on banks and insurers and new plans for a government expenditure review—would yield $25.4 bn by FY27.

- The net budgetary impact shows a $51 bn improvement by FY27 but over half of this ($31 bn) accrues to the recently closed FY22 as higher nominal growth has padded government coffers.

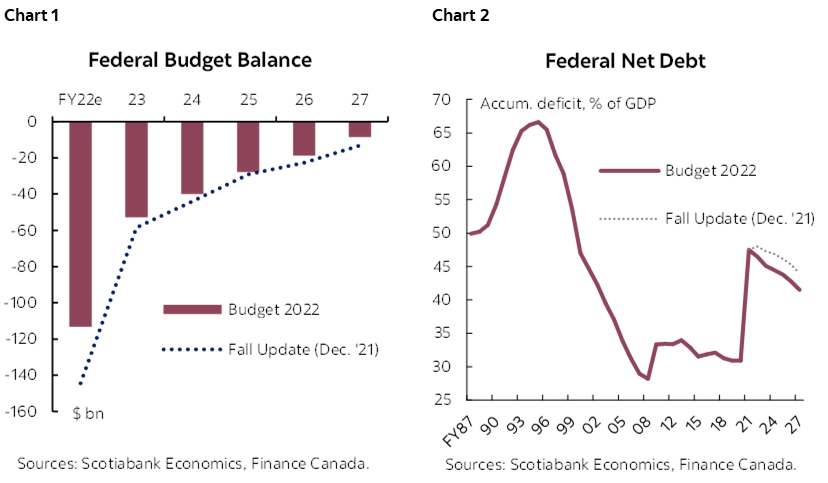

- Apart from the material improvement in the FY22 deficit (-4.6% of GDP versus the earlier-forecasted -5.8%), the path for deficits looks broadly similar to the last official update in December with shortfalls gradually tapering to -0.3% by FY27 (chart 1).

- Canada’s federal net debt shows similar modest improvements relative to the last official update (chart 2). The level for FY22 is estimated slightly lower than prior expectations at 46.5% of GDP—though mostly driven by a stronger denominator—while gradual improvements are expected over the horizon with the level expected to sit at 41.5 % by FY27. A declining trajectory remains the only fiscal anchor.

- There are some laudable measures targeting growth potential and affordability over the medium term—from investments supporting innovation, green growth, and housing supply—but they fall short of a comprehensive growth agenda that would change our medium term outlook for Canada just yet. The budget however does provide a frank assessment of the longer term challenges Canada faces ahead and that is a start.

- In the near term, the government has largely refrained from launching major new supports to offset inflationary pressures facing many Canadians. A one-time $500 payment to Canadians experiencing housing need (through the existing Canada Housing Benefit) is targeted and time-limited, with a relatively modest aggregate impact ($475 mn in FY23).

- However, once provincial relief measures (likely in the order of $7 bn) and retroactive relief payments for childcare in Ontario for FY22 are folded in, directionally at least, there is likely continued pressure on prices.

- Not that there was much lingering doubt, but today’s Budget reaffirms that the onus will fall squarely on the Bank of Canada to wrangle inflation. Markets are braced for a 50 bps move next week (and more to come before the year is out).

- Dated forecast assumptions likely mean more revenue windfalls ahead for the federal government, but still-outstanding (and notable) pledges that would likely put a call on these eventually.

BROAD TAKE-AWAYS

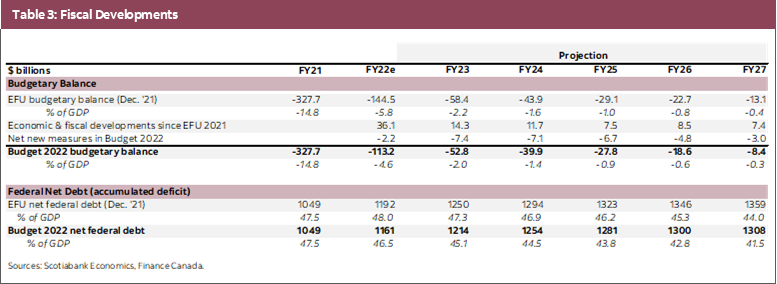

The Budget broadly met our expectations with its tax-and-spend approach to fiscal management. The government set out major new spending by FY27 ($56.6 bn—or closer to $65 bn when various reprofiling and reallocation measures are folded in), offset by stronger economic (e.g., revenue) developments ($85 bn) and new revenue-raising measures ($25.5 bn). The net impact is a cumulative $51 bn to debt-financed spending by FY27 (or a more modest $20 bn if FY22 is netted out) relative to the fiscal path set out in December’s Economic and Fiscal Update. In other words, the Budget confirms the spending bias for Canada’s federal finances even if the bottom line doesn’t appear starkly different.

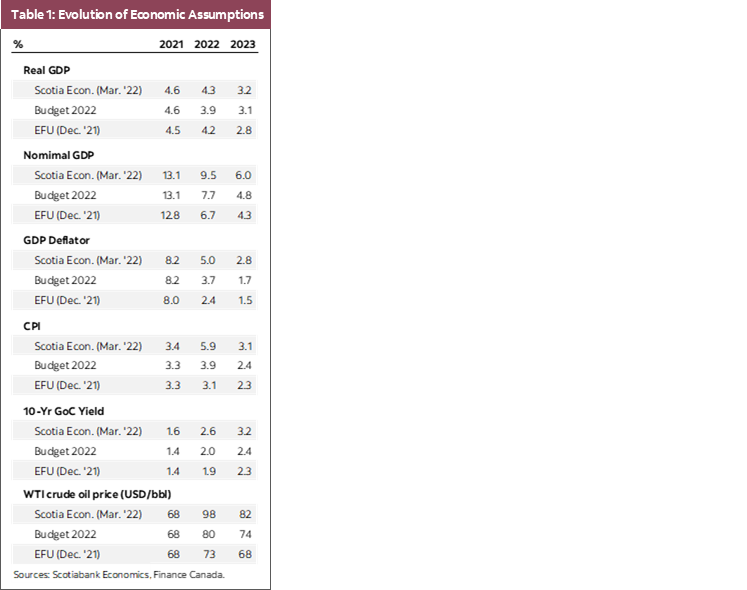

Budgetary developments reinforce our outlook for the Canadian economy. The Canadian economy is already operating above capacity, inflationary pressures are persistent, and the Budget does little to tether expectations. Economic assumptions that inform this Budget (Table 1, page 5) are stale (i.e., assumes 3.9% CPI versus Scotia’s 5.9% in 2022). While the government has wisely refrained from undertaking major new broad-based measures to offset near-term affordability pressures, the system is still primed to spend more once provincial relief measures are factored in that would put more pressure on our price outlook in the near term. Overall, the Budget bolsters our expectation that monetary policy will shoulder the brunt of reining in inflation—and puts (even) more conviction around a 50 bps move next week.

The Budget is delivered in a highly uncertain and volatile environment. With exogenous factors driving government bond yields higher around the world, (federal) fiscal activism reinforces—at the margins—the uplift in the Canadian yield curve, particularly pronounced at the shorter end. Much of today’s developments had likely already been anticipated by markets, and, frankly, get swallowed up by far bigger market-moving events south of the border (and overseas) in the lead-up to Budget Day and the days and weeks to follow.

Looking further out on the horizon, there is little by way of a game-changing growth agenda. There are some important markers such as the carbon capture, utilization, and storage tax incentive, the new innovation agency, and the Canada Growth Fund that—if effective in driving desired outcomes—could materially change the economic landscape and the path to net-zero, but there is still a high degree of implementation uncertainty surrounding these measures so we wouldn’t change our longer-term forecasts just yet. Other measures (e.g., around housing, immigration) should directionally drive higher growth potential and improved affordability over the medium term, but again it would not change our outlook just yet. A frank assessment of the challenges ahead is a start.

It is not just a missed opportunity to set out a national vision for future prosperity over the long run, but also a missed chance to assuage markets in the near term that Canada has a plan. With markets closely monitoring various versions of the yield curve for signs of inversion as a harbinger for a recession, strong economic fundamentals (and a good fiscal buffer) over the medium term are still the best defense in supporting the longer end of the curve.

KEY POLICY MEASURES

For a relatively small document, the Budget covers a broad and all-encompassing landscape of ‘priorities’. Allocation of new spending is spread across eight major themes ranging from housing, green growth, jobs, international priorities, to reconciliation. A ninth category covers revenue-raising measures. See Table 2 (page 5) for an annotated list of priorities and key components.

Housing and housing affordability is a central theme of Budget 2022. A $10 bn (5-year) package focuses largely on supply including low-income housing (totalling $8.8 bn including $4 bn to municipalities). These are important investments that tackle a structural shortage—with the Budget pointing to 3.5 mn homes needed over the next nine years—and it is encouraging to see that the federal government plans to use its weight to ensure concessions are made around zoning and other reforms. There are a series of measures ($1.3 bn) supporting first-time homebuyers including a new tax-free savings account, a doubling of the first-time homebuyers’ tax credit, and more flexible first-time homebuyer incentive. Underpinning demand, these potentially work against affordability objectives, and run the risk that it reinforces regressivity in home-buying. There will also be a 2-year ban on foreign buyers, speculation tax measures, and a rent-to-own program among other measures announced.

Budget 2022 further advances Canada’s green transition. Most measures announced in the Budget had been anticipated, notably via the recent tabling of the 5-year Emissions Reduction Plan at the end of March. A bulk of the $12 bn announced today (or $6.8 bn) around the green agenda falls to the transportation sector including the shift to electric vehicles. Details around tax credits for carbon capture, utilization and storage (CCUS)—including thresholds and exclusions—should provide $2.6 bn to the sector but the Budget presses provinces to complement these incentives, while the exclusion of enhanced oil recovery is likely to draw attention.

There is a great deal of airtime given to a broader growth and innovation agenda but it is more a string of measures as opposed to a comprehensive or compelling vision for stronger growth and productivity. Signature measures include two new arms-length agencies: a Canada Growth Fund to provide concessional support to leverage private capital towards achieving Canada’s resilient growth objectives (capitalized at $15 bn, $1.5 bn concessional), along with a new Canadian Innovation and Investment Agency ($1 bn). There is a tax cut for small businesses by increasing the threshold before companies are phased out of more favourable tax treatment (from $15 mn to $50 mn). Another $3 bn investment in “supply chains” through a host of channels is also provided. The net spend for this growth agenda comes to $5 bn over 5 years. At the same time, the Budget reprofiles $6 bn in infrastructure funds beyond the horizon of the budget (while nudging provinces to accelerate the uptake). A bit of a misnomer—a chapter on middle class jobs with another $6 bn attached to it—is mostly related to immigration programs. These are important investments but hardly comprehensive as the government faces chronic labour productivity challenges.

There is another $18 bn spread across a range on other government priorities. This includes further measures towards reconciliation ($10.6 bn), reinforced support for National Defense ($7.2 bn), a new national dental program ($5.3 bn), and safe community investments ($1.7 bn).

The Budget tables substantial new measures on the revenue-raising side of the ledger ($25.4 bn). A surtax on banks and insurers—albeit a smaller 1.5 ppts versus the platform pledge of 3 ppts—features prominently, along with the anticipated Canada Recovery Dividend—a one-time 15% tax on taxable income above $1 bn in 2021 for combined revenues of $6.1 bn. There is also a clamp-down in Canadian-controlled private corporations to bring in an estimated $4.2 bn, along with a commitment to examine a minimum tax for high earners. CRA enforcements are expected to recover another $3.4 bn. Finally—and a new element—is the plan to launch a government expenditure review that would net $8.9 bn in government revenues over the five year horizon. The latter is commendable (along with ramped up efforts to reallocate across priorities within the Budget itself), but such a review will take time and comes with a host of uncertainties. In fact, netting out the bank taxes, $19 bn of the $25 bn new sources of revenue carries risk.

FISCAL PROJECTIONS

Deficits are expected to continue to decline over the horizon [but at a slower pace] relative to December’s Update. The estimated shortfall for FY22 (-$114 bn, -4.6% of GDP) is much-improved relative to the earlier-anticipated (-$145 bn) owing to much stronger revenue performance. The FY23 balance is expected to decline further to -$53 bn, -2.0% of GDP with consolidation slowing thereafter to land at -$8 bn, -0.3% of GDP by FY27. Notably, the fiscal framework does not yet incorporate any potential spending pressures related to national pharma which would be material if and when implemented.

Net federal debt remains on a firmly downward trajectory. The federal accumulated deficit is estimated to have come down modestly as of share of GDP in FY22 (to 46.5% from 47.5% the year prior) and is expected to gradually descend to 41.5% by FY27 (about 2.5 ppts lower than the Fall Update’s projection. To little surprise, a declining debt trajectory remains the only loose fiscal anchor for the federal government. With stale economic forecasts that likely underestimate baseline expectations, higher nominal GDP growth is likely to do some of that work in the near term, though a “heightened impact” scenario of prolonged conflict shows this anchor could be breached.

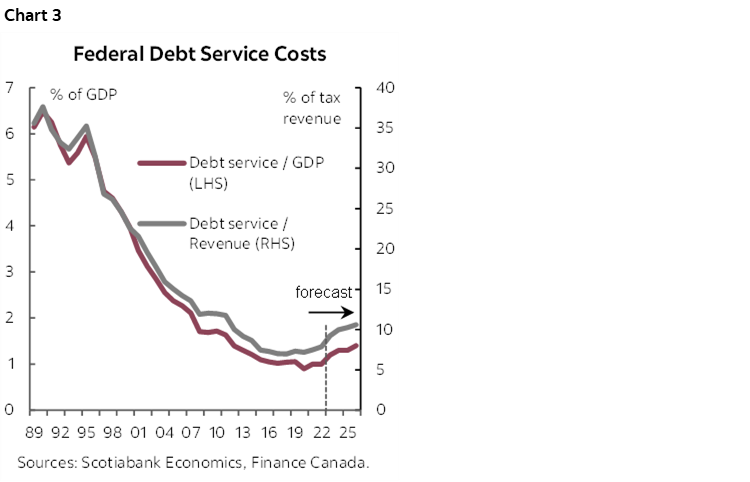

Higher interest rates are expected to put modestly more pressure on debt servicing costs, but these are still expected to remain low by historic standards. Debt servicing costs are estimated at 1.0% of GDP in FY22 and are expected to rise modestly to 1.4% of GDP by FY27 in line with rising interest rates. As a share of revenues, the projected increase is more visible: from 7.5% to 10.6% over the horizon. There is a wide range of views on where rates will settle (and why) over the medium term; the government estimates the impact of a sustained 100 bps increase in interest rates would drive these numbers closer to 1.7% of GDP. These levels would still be well-below historic highs (chart 3).

Borrowing requirements for FY23 are estimated at $435 bn (of which $378 bn reflect refinancing needs) slightly down from FY22 requirements ($453 bn). The government plans to issue $212 bn in bonds in FY23(versus $255 bn in FY22), of which 35% would be long bonds (10-year+), marking a slight shift away from the longer end though the average term to maturity would sit close to 7 years by the end of FY23. The government plans to issue another $5 bn green bonds after its inaugural $5 bn issuance last year. For perspective on incremental market supply, recall the Bank of Canada is expected to roll off maturing government bond assets from its balance sheets ($64 bn and $88 bn maturing in 2022 and 2023).

IT’S ALL RELATIVE

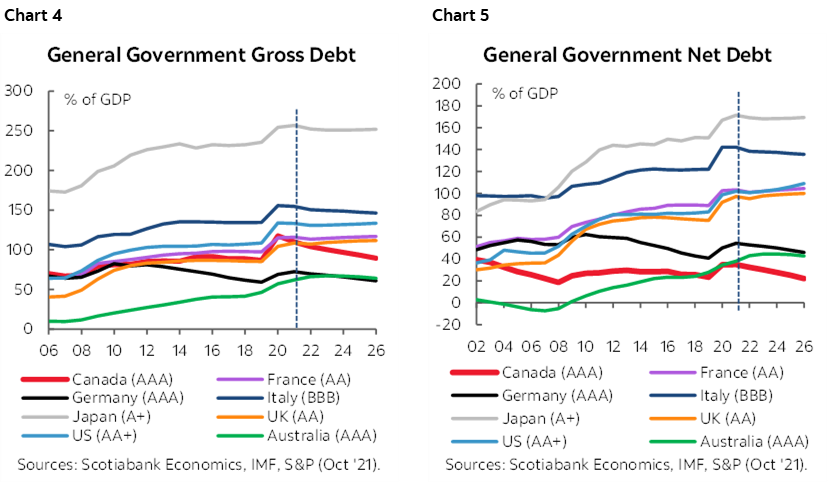

Canada’s general government debt outlook will likely show greater improvements relative to peers. Recall, provincial finances hold sway with about half of Canada’s outstanding government debt at the subnational level so tighter-than-anticipated fiscal paths for most provinces, along with today’s modest improvements at the federal level should translate into improvements in the general government balance relative to peers when the IMF updates its now-stale comparative debt outlook later this month (charts 4 & 5). In the meantime, a handful of peers have or will unleash new spending (notably, Japan, Germany, and the UK) to ward off legitimate economic weakness. The impact of the Russian invasion of Ukraine is driving divergences in growth outlooks along regional and commodity-dependence lines that, for now, likely strengthens Canada’s relative position.

Canada cannot rest on its laurels. Its lack of reserve currency status puts a lower tolerance on debt levels that limits the usefulness of peer comparisons. While commodity channels may boost Canada’s relative outlook for now, the direction of this driver over the medium term hinges on the successful execution of Canada’s green transition plans. Meanwhile, rating agencies should be relieved to see modest improvements to the federal track (and to be able to punt difficult discussions around structural deficits down the road given that pharma commitments weren’t tabled today). Nevertheless, with looming provincial pressures over the medium term they will likely increasingly ask tough questions and Canada—across all levels of government—will eventually need a coherent response.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.