- The BoC stayed on hold and described itself as “patient”…

- ...while nevertheless committing to a hawkish bias…

- ...encouragingly avoiding a prematurely dovish pivot...

- ...that leaves them monitoring conditions like the rest of us

The Bank of Canada delivered a hawkish hold as expected, but it was slightly more hawkish than I had expected going into it. The overnight rate was left at 5% as universally anticipated and so was ongoing quantitative tightening, while the verbiage retained a tightening bias that was anticipated. A statement comparison is offered in the appendix. The Monetary Policy Report including fresh forecasts is available here and the Governor’s opening remarks during his press conference are available here.

On net, Canada's front-end is somewhat volatile today but is unchanged on the day compared to where things left off yesterday while outperforming the US front-end that saw yields drift a little higher after US new home sales data hit. USDCAD is unchanged, perhaps also influenced by the simultaneous release of strong US data.

I like the overall blend of communications that the BoC delivered here today. They struck a reasonable balance in their assessments while leaning cautiously against prematurely declaring victory over inflation while avoiding a promise to end rate hikes. Their view on how inflation risk has moved higher is the same view that I have been marketing with clients.

What can we point to in order to say that their communications were slightly more hawkish on balance than before?

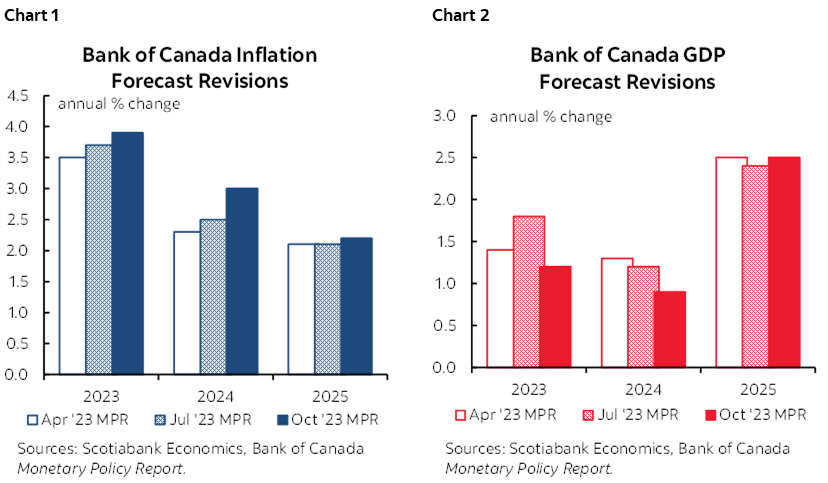

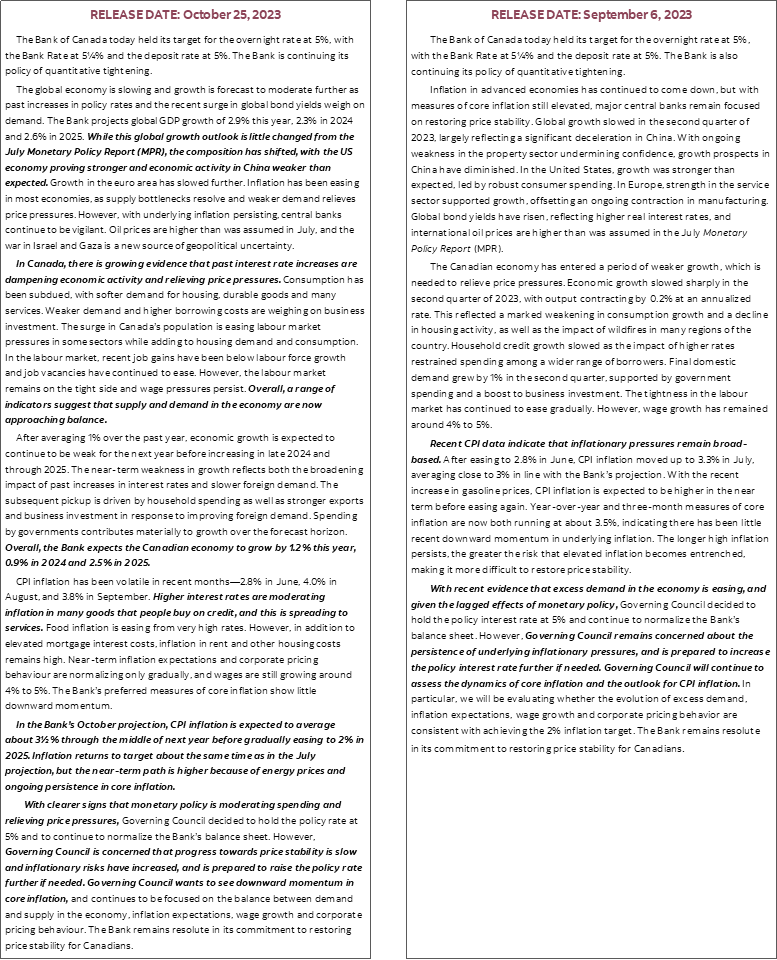

- One obvious starting point is that they raised their inflation forecasts and now see inflation at 3.3% y/y in 2023Q4 (previously 2.9%) and 2.5% in 2024Q4 (previously 2.2%). See chart 1. This is despite revising 2023 and 2024 GDP growth downward while leaving 2025 unchanged (chart 2).

- They delayed the forecast achievement of 2% inflation until 2025H2 instead of mid-2025. Working backwards, that would imply a later start to their thinking on implied easing in advance of achieving this target.

- They statement-codified reference to how "inflationary risks have increased"

- Potential output has been revised down slightly over the projection horizon, reflecting ongoing weakness in productivity against their prior expectation for productivity to improve and as an offset to unexpected strength in population growth. A lower speed limit for growth in future implies that a weakened economy would not create as much disinflationary slack.

The BoC elaborated upon these points by stating that “Overall, inflationary risks have increased since July. Today’s forecast has inflation on a higher path than we expected. In addition, rising global tensions are increasing risks. In a more hostile world, energy prices could move sharply higher and supply chains could be disrupted again, pushing inflation up around the world.”

The reasons for saying that inflation risks are higher and for revising up inflation forecasts included:

- energy price pressures partly related to geopolitical tensions;

- structural housing shortfalls;

- Potential further shocks to global supply chains partly related to wars;

- stickiness in underlying prices.

Those are really the main takeaways. There are other points to quibble about, but they don’t change the bottom line which is that the BoC is on hold and monitoring conditions with a hawkish bias before deciding next steps.

One point to quibble over is that in my view they continue to inappropriately ignore the effects of multiple transitory shocks on the economy from wildfires to multiple strikes and shaky weather and pin the summertime slowdown entirely on their view that rate hikes are working to cool demand. That’s obviously an exaggeration to anyone who saw with their own eyes what was happening.

Another one to quibble about is that, in my opinion, the Bank of Canada is making the same mistake that some others are making in stating that real consumption growth has stalled in per capita terms and that labour force growth is exceeding job gains which are signs—in their view—that tighter policy is working. They are using aggregate population growth to arrive at these conclusions, but it’s silly to take the total population change when so much of the surge in immigration that has driven rapid population growth is made up of students and temps.

ADDED INSIGHTS FROM THE PRESS CONFERENCE

The press conference Q&A offered added insights compared to the formal communications with my attempt at a transcript offered below.

Q1. CAD is at a seven month low to the USD today. How concerned are you about the implications for inflation especially since the US economy is doing better than expected?

A1. We don't target the currency. Normally when we raise interest rates a lot, the currency appreciates and that slows the economy. Because other central banks have also been raising, CAD is reasonably stable versus the US, up against others. We're not getting the direct effect through lower imported inflation due to C$ weakness which means that we have to rely more upon interest rates and that is something we have to take into account.

Q2. What do you need to see happen in the near term to prompt another hike?

A2. We decided to hold the policy rate because we are seeing clearer evidence that higher rates are cooling the economy but we did leave the door open to higher rates if needed. We need to see downward momentum in our measures of core inflation. Over the past 8 months or so, there has really been very little downward momentum. We need to see downward momentum. We are watching the balance between demand and supply, wage growth, corporate pricing behaviour and inflation expectations. We will take our decisions one at a time. We are prepared to raise our policy rate further if that's what needed.

Q3. One of the upside risks is the war and the effect on energy prices. The MPR notes this may play out differently today because of other factors driving inflation. How would the BoC handle this now?

A3. We've already built in a higher path for oil prices. We have raised that by about US$10 since our projections in July. It's clear there are risks that tensions in the Middle East could intensify. Typically we would look through higher oil prices, but it's not the same set of circumstances today. Expectations are already high, corporate pricing behaviour has changed. In that environment we need to be more focused upon higher oil prices than normal and through the effects on core inflation by way of evidence they are feeding through the rest of the economy.

Q4. Are expecting recession in the coming quarters?

A4. We can't rule out the possibility of small negative numbers for growth. When people say 'recession' they have a steep decline in output and a sharp rise in unemployment but that's not what we are forecasting. The path to a soft landing was narrow and has gotten narrower.

Q5. What explains the difference between growth in the US and Canada and is it persistent?

A5. The structure of the mortgage market in Canada is different. Mortgages reset faster in Canada. Monetary policy would be expected to have more traction in Canada. Also, the buffer of extra savings is still being horded in Canada and not spent in part like in the US and so Canadian consumption has been weaker as people save for higher mortgage payments. A longer-term issue is productivity growth in the two countries.

Q6. Why have house prices not come down more in this hike cycle as in past cycles?

A6. The answer comes down to a structural lack of supply in the Canadian housing market.

Q7. Can you comment on mortgage resets?

A7. We are paying really close attention to the mortgage renewal cycle. We will comment more on this in the financial system review in November which is where we would normally do this.

Q8. To what extent is fiscal policy contributing to inflation? Are there other things that governments can do to bring inflation down?

A8. We don't set fiscal policy. If current spending plans are delivered then spending growth of about 2.5% will exceed potential GDP growth of about 2% and this will add to inflation. It would be helpful if governments considered the impact of their decisions on inflation.

Q9. When can we expect lower rates?

A9. We can reduce our policy rate before achieving 2% inflation when we see where it is going. Now is not the time to assess this. For now, we are evaluating whether the policy rate has tightened sufficiently. We need to see clear signs that inflation is going back down to 2% and right now it is too early.

Q10. Has Canada entered a period of stagflation?

A10. It's not a word I would use. Stagflation is a period of high inflation and high unemployment. Inflation is lower than the 1970s and the UR is quite low.

Q11. How confident are you that inflation returns to target around 2025H2? Has your confidence changed in the past couple of months?

A11. What has changed is that inflationary risks have increased for two reasons. One is that the trend has moved up so we are further from our target and we are starting from a worse place. The other is that we have raised our oil price forecast. There is also the potential for renewed supply chain shocks along with geopolitical shocks. At the same time, we are seeing supply and demand coming back into balance and that's the reason we held at 5% today. We will need to monitor the risks carefully.

Q12. If US Treasury yields continued to run higher because of deficits and Treasury supply and not inflation, could that be inflationary or disinflationary to Canada and what risks would that pose to Canadian monetary policy?

A12. To the degree that higher bond yields reflect central bank guidance it's not a substitute. To a degree to which it does not then it could be a substitute. It is unclear and remains to be seen.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.