- August’s retail rebound ground to a halt in September…

- ...and so did manufacturing…

- ...as choppy data continues to hang over trend rebounds…

- ...at least partly reflecting shifts to services…

- ...and supply chain problems

- BoC implications

CDN retail sales, m/m % change, SA, August :

Actual: 2.1 / 2.8

Scotia: 2.1 / 2.4

Consensus: 2.0 / 2.6

Prior: -0.6 / -1.0

September ‘flash’ guidance: -1.9

Canadian retail sales disappointed in the preliminary guidance for September. That is the new information in the release and it dampens some of the enthusiasm around the rebound that occurred in August alongside disappointing advance guidance on manufacturing sales during September. There are nevertheless important caveats that are worth flagging.

Statistics Canada guided that September’s preliminary ‘flash’ estimate for retail sales was down 1.9% m/m which reverses almost all of the gain in August that landed in line with advance estimates. While its move toward providing ‘flash’ readings based on partial samples (54% in this case, versus the full ~90% response rate in the final estimate) has been welcomed, the agency doesn’t provide any details or guidance on the drivers. Our tracking of auto sales units suggests that played a major role, but with limited confidence in how this translates into autos within retail sales.

A further point of softness lies in the fact that about one-third of the gain in the value of retail sales during August was due to higher prices, as volumes were up by 1.4% m/m. If you’ve seen the CPI figures or even if you bought anything in August, then you’d probably have a good understanding of this point!

Still, we definitely saw a powerful rebound in Q3, although it sets up more questions into Q4. Sales in dollar terms were up by about +11% in q/q in annualized terms during Q3. That incorporates the preliminary September flash guidance. Sales in volume terms were up by about +6% q/q SAAR which incorporates the September flash guidance by assuming that volumes fell by a little more than the value did due to the partial offset from higher prices in September’s CPI report. Chart 1 shows the volume estimates compared to history.

The way the quarter ended nevertheless bakes in a weak starting point for Q4. We're going to need a strong holiday season to keep in the black for Q4 retail sales and there is no shortage of arguments around the risks in both directions. Based on the Q3 totals and the way the quarter ended, Q4 has a baked in decline of 2.4% q/q SAAR in sales dollars and a nearly 5% drop in sales volumes. Clearly we’re still in the midst of taking down choppy data.

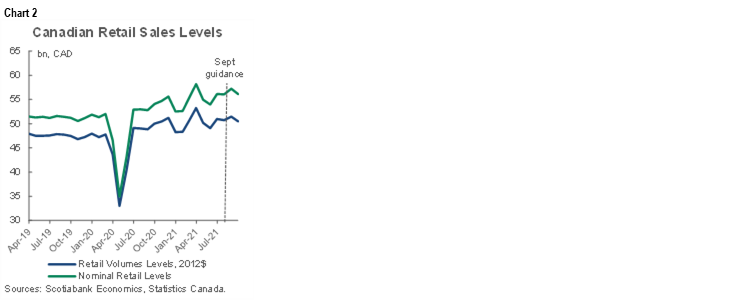

Chart 2 shows the trend in the levels of sales dollars and volumes during the pandemic.

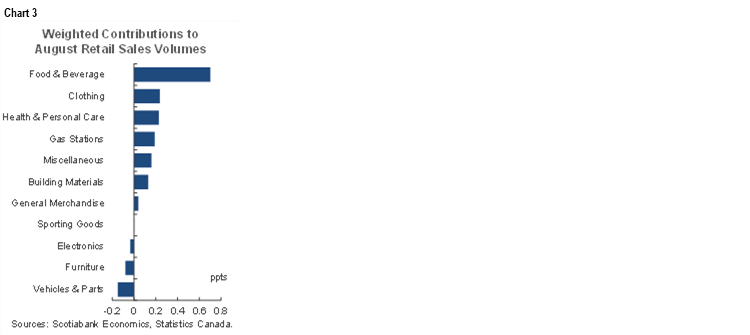

Chart 3 shows the breakdown of the change in retail sales volumes during August in terms of weighted contributions to the overall percentage gain of 2.1%.

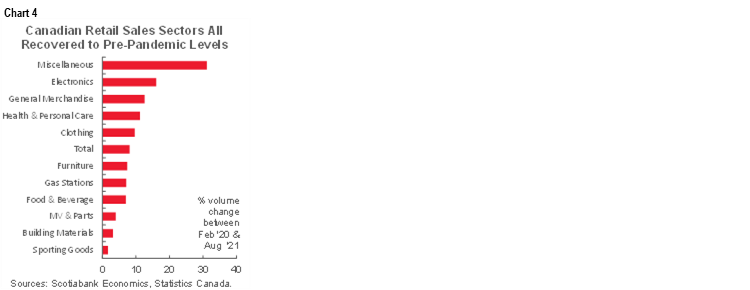

Chart 4 shows the cumulative change in the value of retail sales since the pandemic first struck.

BANK OF CANADA IMPLICATIONS

Of course it’s a stretch to say that one or two releases for a segment of the economy matter much to a central bank crafting its broad policy stance. Still, we can use it as an opportunity to reinforce a narrative.

Choppy data will keep the BoC guarded toward the near-term. I expect them to shift to the reinvestment phase of the QE program next Wednesday, but for Governor Macklem to emphasize choppiness and ongoing slack in the economy while leaning—in nuanced fashion—against early hike pricing that I still think has gone too far. If he doesn’t, the front-end is likely to get hit harder. Their forecasts are still likely to lean toward closure of spare capacity—and hence rate hikes—along a similar timeline to what thsey said in July.

CAVEATS

A rather large caveat is that 71% of the Canadian economy is represented by services. That matters because retail sales sharply underrepresent services spending and don’t include major types that are probably the biggest beneficiaries of ending lockdowns. Unfortunately we have far fewer readings for the services sector. We can point to things like Open Table restaurant reservations and mobility gauges, but they are not seasonally adjusted which matters at the start of a new school year and end of summer transitions, and so we’re left monitoring old economy variables like this one until GDP arrives at the end of the data march. What we therefore can’t tell is the extent to which spending shifted from goods toward services in September.

Second is the ongoing debate over supply chain effects versus demand signals. I wish Statcan would provide a bit more colour on their flash guidance. They say the drop in manufacturing was "mostly" due to transportation, in which case supply chain effects are probably the culprit. It would be helpful if they'd provide sales ex-trans guidance. In any event, supply chain effects continue to mess things up. That’s also likely to be the case for retail sales as product shortages in categories like autos, electronics etc and long delivery delays are holding back spending.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.