- The decline in jobs was not materially worse than expected

- Jobs might drop again in May before a durable rebound returns

- The details broadly met expectations

Canadian jobs m/m 000s // UR %, SA, April:

Actual: -207.1 / 8.1

Scotia: -150 / 7.8

Consensus: -150 / 8.0

Prior: 303.1 / 7.5

Canada’s jobs report was generally in the ballpark of expectations relative to the big miss stateside. As restrictions tightened, jobs were lost at a pace commensurate to consensus expectations especially after taking into account a 95% confidence interval of +/-57k around the estimate. Putting on a statistician’s hat puts the drop barely at the outer limit of this interval. One cannot therefore say that the pace of decline was bigger than either the median consensus estimate or mine in a statistically significant manner. The decline averted both tails of the consensus distribution that included some expecting a small rise and a minority expecting a materially worse number.

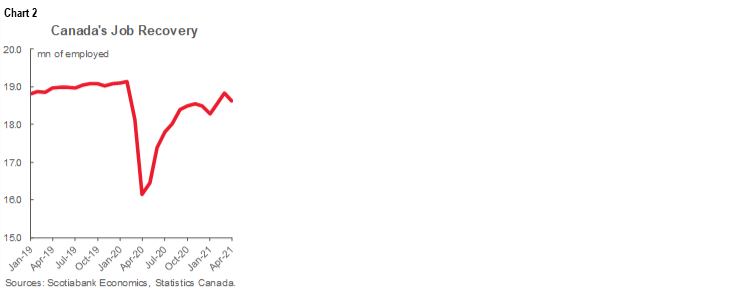

That makes Canada’s report much more boring than the unfortunate miss stateside albeit while taking that in stride (recap here). Canada’s jobs could also take a further step back in May but are likely to begin a more durable rebound from June onward if restrictions ease into June and the new cases trend continues to ebb (chart 1). It remains highly feasible that Canada could regain all lost jobs during the pandemic later this year and well before the US.

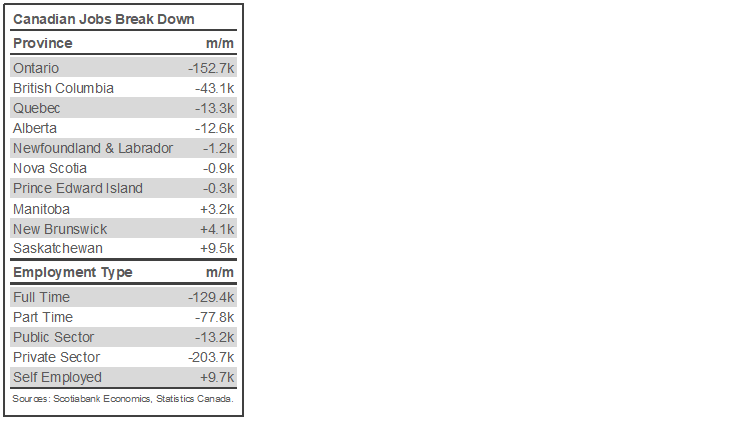

The details behind Canada’s report generally offered few surprises to the headline dip. See the summary table. See chart 2 for the progress toward regaining lost jobs to date.

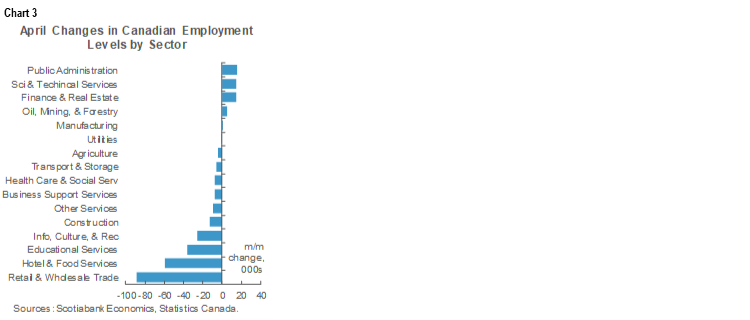

By sector, service sector jobs fell by 195.4k and goods sector jobs fell by about 12k. Within goods, construction jobs fell by almost 13k with agriculture down 4.4k and natural resources up 5k.

Within services, the drop was spread across four main areas. Wholesale/retail fell 89k. Accommodation and food services fell 59k. Educational services fell by 36k. Info/culture/recreation fell 26k.

Chart 3 shows the sector breakdown of the change in jobs.

The drop in the education sector was as expected and explained by StatsCan as driven by the fact that “more workers than usual were absent from their jobs due to the delayed spring break” in Ontario.

Public sector payroll jobs fell 13k so all of the decline in payroll employment was at private employers (-204k). Self-employed jobs were up by just 10k.

By province, the decline was concentrated in the biggest provinces and where the COVID-19 new cases have tended to be mostly focused. Ontario shed 153k jobs with BC down 43k and both Quebec and Alberta down by about 13k.

The unemployment rate climbed to 8.1% as the labour force fell by 84k and hence less than the drop in employment (chart 4).

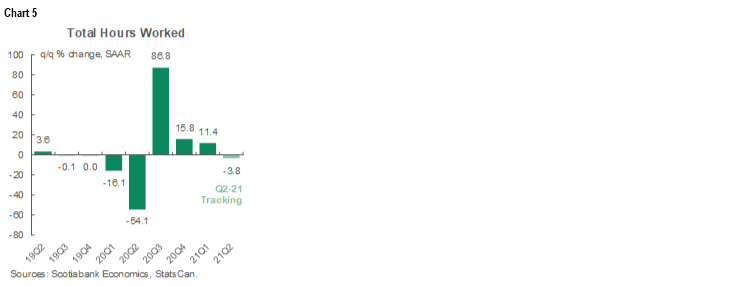

Hours worked also fell by 2.7% m/m which is the largest single-month drop since April of last year. At an annualized rate, hours worked are tracking a drop of 3.8% q/q in Q2 so far (chart 5).

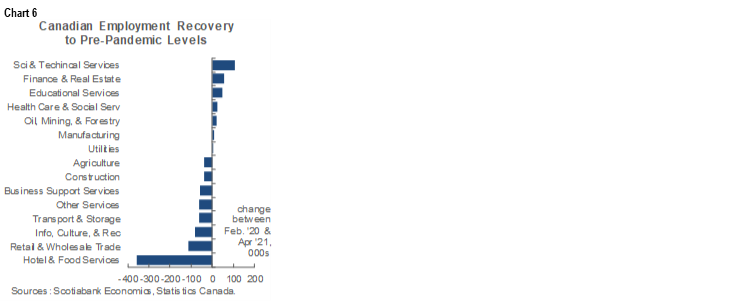

On a cumulative basis to date, Canada is down 503,000 jobs compared to February of last year, or about 2.6% of the pre-pandemic level of employment. That remains vastly better than the US where nonfarm payrolls remain 5.4% lower than in February 2020 for a net decline of 8.2 million that is far in excess of what can be explained by relative size of the two countries. Chart 6 shows where the cumulative employment changes are concentrated.

Youths took this one on the chin. The 15–24 age category saw a 101k job loss which roughly equalled the losses for everyone else aged 25+.

Wage growth should be ignored at least in terms of the year-over-year rate that is rebasing to the perversely higher average wage of April 2020 relative to prior months (chart 7). That was caused by relatively lower wage workers dropping out of the average wage figure in disproportionate fashion. It’s also not the BoC’s preferred wage measure anyway.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.