- Fed Chair Powell’s messages broadly met expectations

- He was on the data fence toward the size of September’s move

- Warned against premature easing

- More candid about the costs to the economy

- Unchanged forward guidance

Fed Chair Powell broadly met my expectations for his speech (here) after large market moves in the past month, but how markets are reacting partly depends on the asset class. The US 2-year yield is up by only 3–4bps post-speech at the time of writing and would have reacted more strongly had market pricing not changed over recent weeks. The 10 year yield is about 1–2bps lower as the curve flattened. The dollar gained about ¾% on a DXY basis. The S&P500 fell by just under 2% since among all asset classes it had the most hope that Powell might pivot more dovishly which he clearly did not.

Here are the main takeaways from his speech.

Commitment Phobic in the Near-Term

The focus now pivots toward next Friday’s payrolls report and the next CPI print as Powell and other Fed officials have placed enormous importance upon near-term data to inform the size of the next rate move. Key in that regard is this passage:

“July's increase in the target range was the second 75 basis point increase in as many meetings, and I said then that another unusually large increase could be appropriate at our next meeting. We are now about halfway through the intermeeting period. Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook.”

Warning Against Premature Easing

Powell also leaned strongly against prematurely easing and declaring victory against high inflation. Key in this regard is this paragraph toward the end of his speech:

“That brings me to the third lesson, which is that we must keep at it until the job is done. History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting. The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.”

Powell backed this up with a section of his speech that is summarized in one line from it: “The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.” Right now, the Fed’s fears in this regard appear to be manageable but they want to keep it that way which counsels not dropping their guard and swinging in the other direction too quickly.

More Candid About the Implications for the Economy

Powell was a bit more candid about the economic costs to what the Fed is trying to do. That’s refreshing. It’s not helpful to have folks out there arguing that the Fed will be knocked off course if they discover evidence that they are breaking a few teacups. Powell is correctly stating that’s their intent, as it should be. The goal is to tighten financial conditions to ease on some slack and hence damage activity readings in a way that cools inflationary pressures.

Here’s the key passage in that regard:

“Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

Looking Through July’s Inflation. August Could Rebound

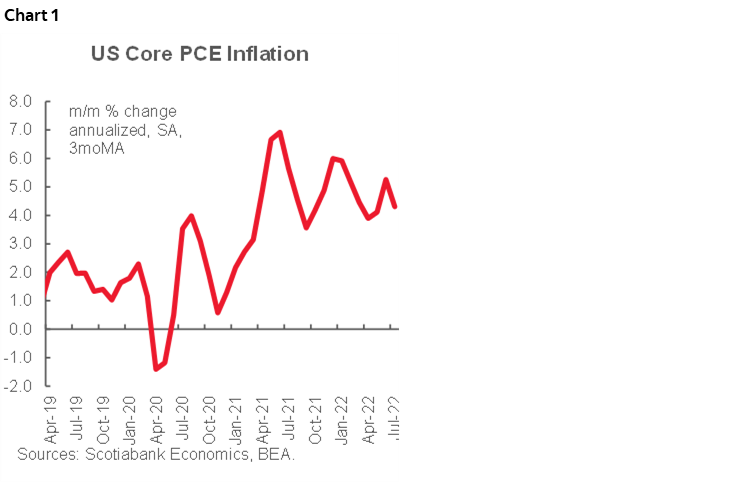

Powell dismissed the softer inflation readings for July including this morning’s core PCE gauges that met my expectations that were slightly below consensus although the income and spending numbers were softer than I had thought they would be. His direct quote on this is here: “While the lower inflation readings for July are welcome, a single month’s improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down.” Chart 1 shows why. The three-month moving average of m/m annualized core PCE inflation remains range bound and well above target with no trend improvement. Besides, this isn’t about inflation’s short game as much as it is about the longer path ahead.

On that note, my tentative bottom-up estimate for August’s CPI inflation readings on September 13th is 0.2% m/m SA and core at 0.4% m/m SA. If that happens then annualized inflation will rebound from July and preserve the smoothed trend at rates well above target.

Job Market is Too Strong

Powell placed further emphasis upon overheating job markets “…with demand for workers substantially exceeding the supply of available workers.” To that effect, we’ve had 3 ¼ million nonfarm payroll positions created so far this year which has exceeded consensus expectations by about one million. Strong indeed, though the household survey is less convincing as all of its gain was in Q1 before stumbling in Q2.

Truisms Behind Forward Guidance

On the pace after September, Powell simply repeated that “as the stance of monetary policy tightens further, it likely will become appropriate to slow the pace of increases.” That’s largely a truism since the closer you get to restrictive and the further into it the Fed goes, the less likely we’ll be getting super-sized moves but without shutting the down on additional smaller moves toward an uncertain peak.

Powell avoided any reference to estimates of the neutral policy rate and the longer-run policy rate path and simply referenced how participants will update their projections at the September meeting.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.