- Mexico: Industrial sector continues to weigh on GDP

- Colombia: BanRep survey—Inflation expectations rise again and rates will stay high for longer; Imports continued their gains in September, reflecting strong domestic demand

MEXICO: INDUSTRIAL SECTOR CONTINUES TO WEIGH ON GDP

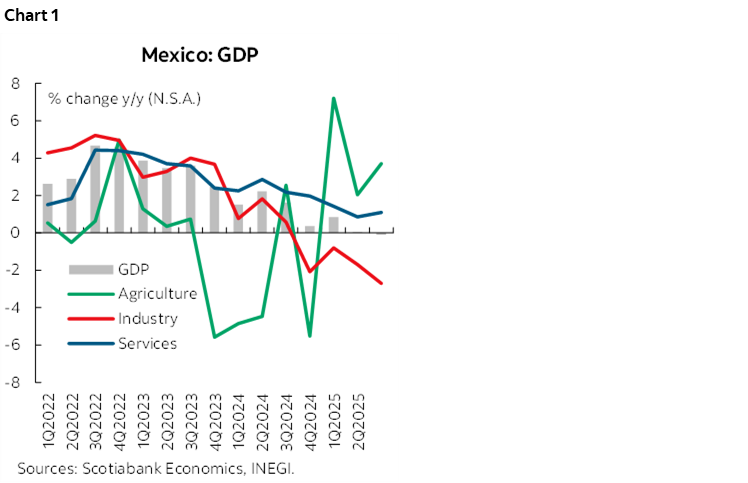

According to INEGI, in the July–September 2025 quarter and with seasonally adjusted figures, Gross Domestic Product (GDP) registered a contraction of -0.3% q/q, while with original figures it remained stagnant, with a slight decrease of -0.1% a/a. By component (chart 1), on a quarterly basis and with seasonally adjusted series, primary activities increased 3.5% and services 0.2%. Meanwhile, industrial activities decreased -1.5%. At an annual rate, primary activities expanded 3.7% and services 1.1%, with the main increases occurring in leisure, cultural and sports services, and other recreational services (13.2%), business support services (10.7%), and health and social assistance services (5.3%). Meanwhile, industrial activities fell for the fourth consecutive quarter, standing at -2.7% y/y, where mining contracted -5.0%, utilities fell -1.4%, construction -4.7%, and manufacturing industries -1.9%.

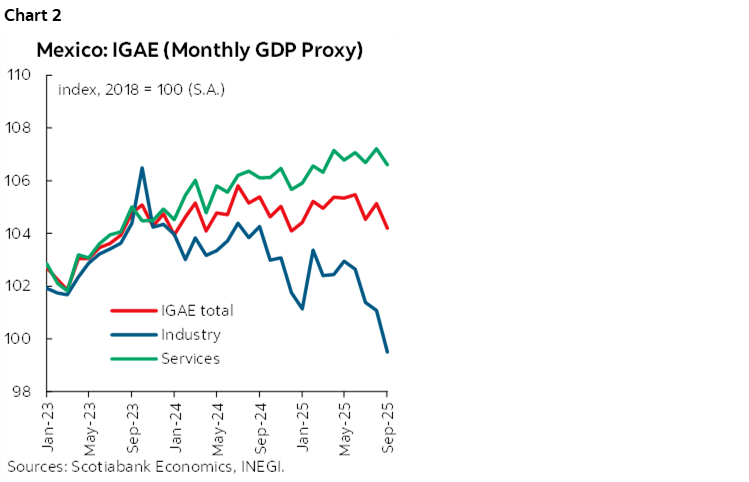

In September, the Global Indicator of Economic Activity (IGAE) fell on a monthly basis by -0.6% from the previous 0.6%. By activities (chart 2), there were widespread declines in seasonally adjusted monthly figures, the deepest being primary activities, with -4.9%, compared to 14.5% last month. Secondary activities fell -0.4% compared to August, highlighting the contraction in construction (-2.5%). As for services, they had a monthly decrease of -0.5%, with contractions in trade (-2.6% wholesale and -0.4% retail), leisure services (-3.0%), lodging services (-2.1%), among others. In its annual comparison with original figures, the IGAE grew barely 0.7%, now moving into positive territory. Primary activities grew 8.2% and services by 2.0%, while secondary activities fell for the sixth consecutive month, by -2.4%.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

COLOMBIA: BANREP SURVEY—INFLATION EXPECTATIONS RISE AGAIN AND RATES WILL STAY HIGH FOR LONGER

The Central Bank (BanRep) published its November survey of economists’ expectations late on Wednesday, November 20th. Inflation expectations rose again, likely adjusting to the upside surprise from the latest CPI reading. Expectations for December 2025 inflation stand at 5.34%, while projections for December 2026 are at 4.43%, both above the central bank’s target range of 2%–4%.

Economists’ expectations remain well above the path projected by the central bank in its latest Monetary Policy Report (3.8% for Dec-2026). The main difference appears to be assumptions regarding the minimum wage increase. Our projection for year-end 2026 (4.3%) incorporates an 11% minimum wage increase, whereas the central bank assumes an increase following the technical rule of inflation plus productivity (approximately 6%). In any case, we infer that the economist consensus already factors in a significant minimum wage hike. Interestingly, even the most pessimistic projection does not assume a sharp acceleration in inflation, which suggests that a rate hike from BanRep remains unlikely in the current monetary policy horizon. Scotiabank Colpatria’s inflation path for 2025 is broadly aligned with economist consensus. We project year-end inflation at 5.31%, and for December 2026, our forecast is 4.30%. In our view, disinflation will mainly come from non-core components, particularly food prices.

On monetary policy, the survey’s median expectation indicates that rate cuts could begin in October, with rates closing the year at 8.75%, above previous expectations of 8.25%–8.50%. Discussions around a potential hike have gained traction in financial markets following recent remarks by board members, who noted that while hikes are not central to the debate, they cannot be ruled out. At Scotiabank Colpatria, we expect rate stability until June 2026, followed by gradual cuts of 25 bps per meeting, ending the year at 8.50%. In our opinion, the central bank would only consider hikes if inflation accelerates significantly—an outcome we currently do not anticipate.

Expectations for the exchange rate continued to decline. For December 2025, analysts estimate COP 3,846 per USD, down 144 pesos from the previous survey. For 2026, the forecast is COP 3,920, 124 pesos below the prior projection. Scotiabank Colpatria’s fundamental value for the exchange rate is around COP 4,150; however, in the short term, we expect USDCOP to remain below fundamentals due to Ministry of Finance monetization activity. Our year-end projections are COP 3,986 for 2025 and COP 4,045 for 2026.

Key takeaways:

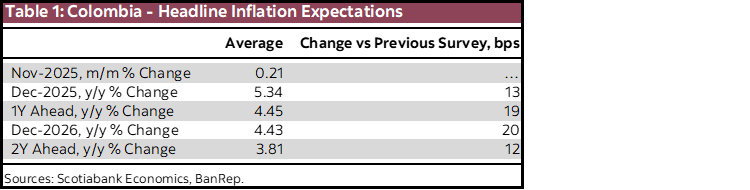

- Short-term inflation expectations. For November, the consensus estimate is 0.21% m/m, implying annual inflation of ~5.45% y/y, down from 5.51% previously. The highest estimate is 0.30%, and the lowest is 0.10%. Scotiabank Colpatria projects 0.20% m/m and 5.44% y/y. Core inflation (excluding food) is projected at 0.24% m/m and 5.19% y/y; our forecast is 0.25% m/m and 5.20% y/y (table 1).

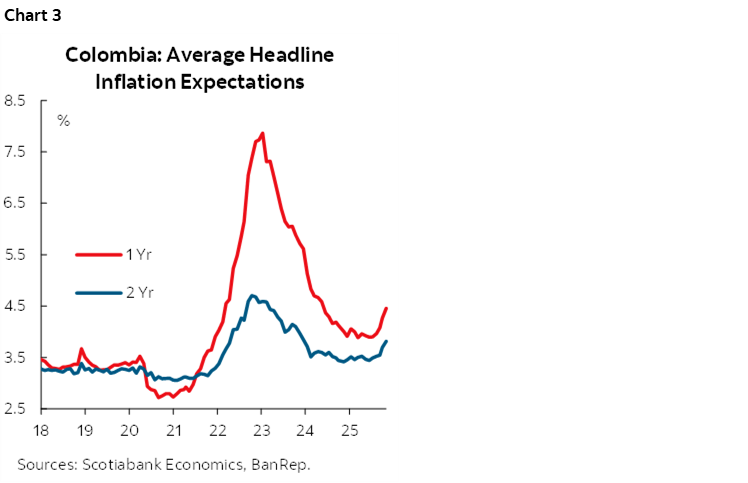

- Medium-term inflation expectations. December 2025 expectations rose 13 bps to 5.34%. One-year horizon expectations increased 19 bps to 4.45%, and two-year horizon expectations rose 12 bps to 3.81% (chart 3). Scotiabank Colpatria’s forecasts are close to consensus: Dec-2025 at 5.31% y/y and Dec-2026 at 4.30% y/y. We expect inflation to enter the target range in H2-2027.

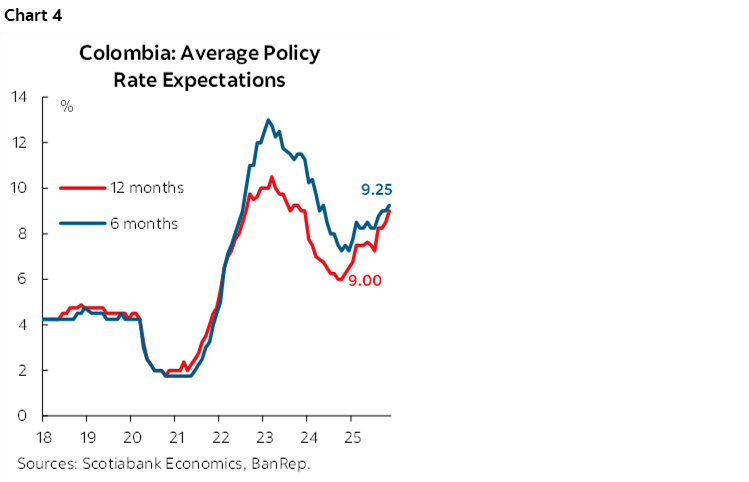

- Monetary policy rate. The median expectation is for prolonged stability, with cuts reappearing in late 2026. Hawkish scenario: hikes starting in December, closing 2025 at 9.50% and 2026 at 10.75%. Dovish scenario: rates closing at 9.00% in Dec-2025 and 7.50% in Dec-2026 (chart 4).

IMPORTS CONTINUED THEIR GAINS IN SEPTEMBER, REFLECTING STRONG DOMESTIC DEMAND

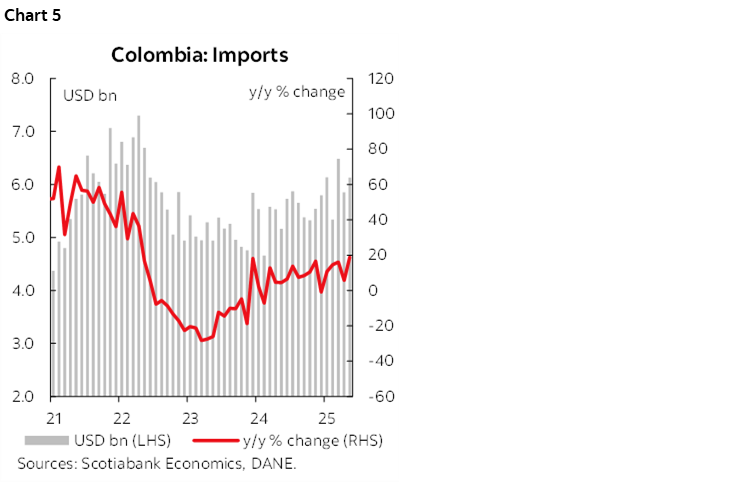

On Wednesday, November 19th, 2025, DANE released September import data, reporting a level of US$6.13 billion CIF (chart 5). This represents an 18.7% (y/y) increase. Consumption-related imports surged 29.5% y/y, driven by strong demand for durable goods (+45.8% y/y). Meanwhile, capital goods rose 15.3%, and raw materials and intermediate products advanced 14.1% y/y. All the segments reflect the strong performance of domestic demand.

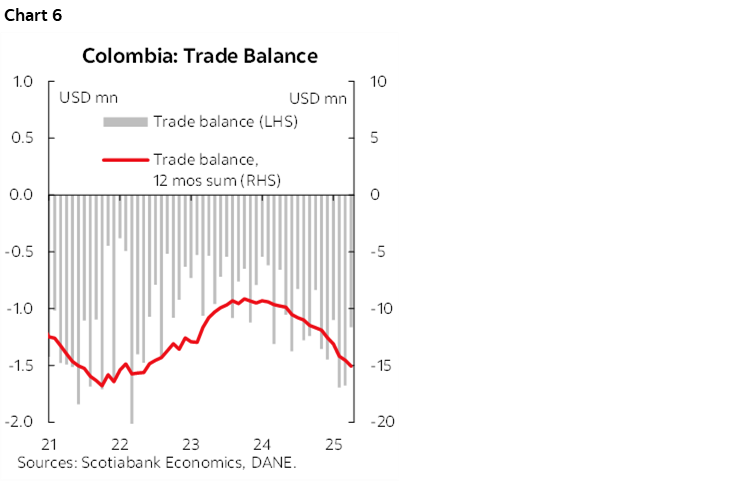

Compared to the previous year, the trade deficit widened standing at US$1.16 billion in September, reaching US$11.77 billion YTD, versus US$7.55 billion in the same period of 2024. This deterioration reflects weak exports performance combined with robust import growth, largely fueled by household spending patterns favouring higher consumption, and some investment pick-up in the manufacturing sector.

As highlighted in earlier reports, despite the trade deficit widening, remittances inflows have helped keep under control the current account deficit (chart 6). Consequently, we do not anticipate significant FX upside pressure under current conditions. However, monetization of foreign public debt and carry trade flows—given the central bank’s cautious stance—are likely to keep the USDCOP trading below our estimated macrofundamental level of COP 4,150.

Key takeaways:

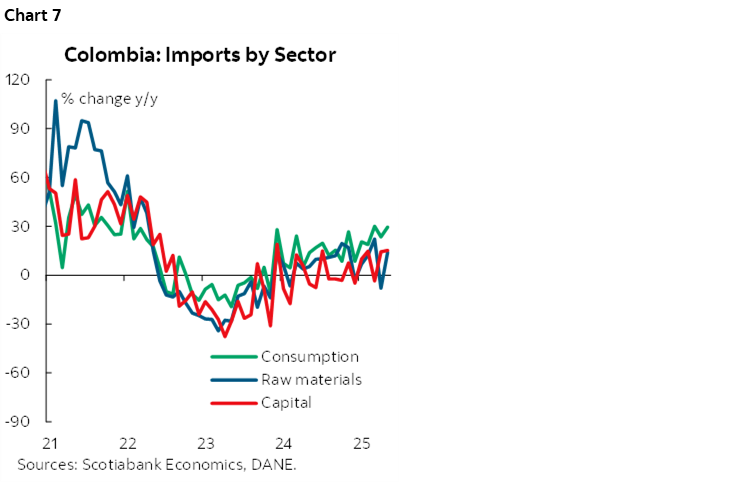

- Consumption goods imports once again led the gains (chart 7). In September, year-on-year consumption-related imports rose 29.5%, driven by a sharp increase in durable goods (+45.8% y/y), while non-durable goods advanced 16.7% y/y. The most dynamic segment was vehicle imports (+52% y/y), followed by clothing (+33.7% y/y).

- The surge in durable goods purchases is noteworthy. As we have mentioned before, despite stronger demand, credit uptake has not increased significantly, and inflation for tradable goods remains elevated—even under exchange rate conditions that could favour lower prices. Consequently, we maintain our view that Colombia’s recovery is currently supported by an exogenous income shock, reducing reliance on credit and limiting the pass-through of FX appreciation to consumer prices.

- Imports of raw materials grew 14.1% y/y, led by fuel (+15.4%) and food products (+26.8%), chemical products (+8.8% y/y) and mining products (+14.5% y/y).

- Capital goods imports expanded as well by 15.3% y/y, reflecting strong purchases of industrial capital goods (+17.5% y/y). The expansion in this chapter demonstrate that part of the better domestic demand is fueled by investment, in segments different from construction sector.

—Jackeline Piraján & Valentina Guio

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.