Central banks & macro data: Holds expected in Mexico and Peru; October inflation prints from Mexico and Argentina

Brazil: Brazilian inflation accelerated in October, driven by stimulus and food prices

Colombia: Fitch affirmed Colombia’s sovereign credit rating at “BBB-”, outlook “Negative”

Mexico: Investment rebounded in August; consumption reflected weak domestic demand; IMF Article IV consultation

Peru: BCRP business sentiment survey suggested greater stability; car sales were up in October

CENTRAL BANKS & MACRO DATA: HOLDS EXPECTED IN MEXICO AND PERU; OCTOBER INFLATION PRINTS FROM MEXICO AND ARGENTINA

Inflation prints this week in Mexico (Nov. 9) and Argentina (Nov. 12) complete the suite of updates on October price data across the Latam-6. While recoveries are driving inflation up from its mid-year lows, we expect prices to remain broadly well-contained across the region. In Mexico, October inflation out at 07:00 ET this morning rose from 0.23% m/m in September to 0.61% m/m in October, above the 0.57% m/m consensus; nevertheless, base effects meant the headline annual rate moved up only from 4.01% y/y in September to 4.09% y/y in October (versus consensus of 4.06% y/y). A more fulsome dissection of the data will follow from our team in CDMX, but the above-target-range print reinforces our expectation of a hold from Banxico on Thursday. See the Market Events & Indicators risk calendar in the most recent Latam Weekly for a full list of releases and policy developments coming this week.

Monetary-policy decisions are due Thursday from both Mexico’s Banxico and Peru’s BCRP. We look at considerations for both decisions below.

- Mexico. The Banxico Board’s next monetary policy meeting is scheduled for Thursday, November 12 and it is expected to be another finely balanced decision. In a close call, our team in Mexico City expects the Board to hold the target rate at 4.25%, thereby ending its easing cycle (chart 1). Nevertheless, our team recognizes that there is a non-negligible risk that the Board cuts once more on Thursday and then signals a hold.

At its last rate meeting on September 24, the Board voted unanimously to cut its target rate for an eleventh time, by -25 bps to the current 4.25%, for a total of -400 bps in easing this cycle. Although in line with consensus, analysts had expected a divided Board owing to risks from inflation, growth, and financial markets. In its statement, the Board emphasized three key points: (1) the balance of risks for inflation remained uncertain, but the Board anticipated that headline and core inflation would stay around 3% y/y over the next 12 to 21 months; (2) the balance of risks to growth were skewed downward, a point on which our forecasts concur (see the October 31 Latam Weekly); and (3) global economic activity is recovering, but advanced-economy central banks are likely to keep their policy stances accommodative.

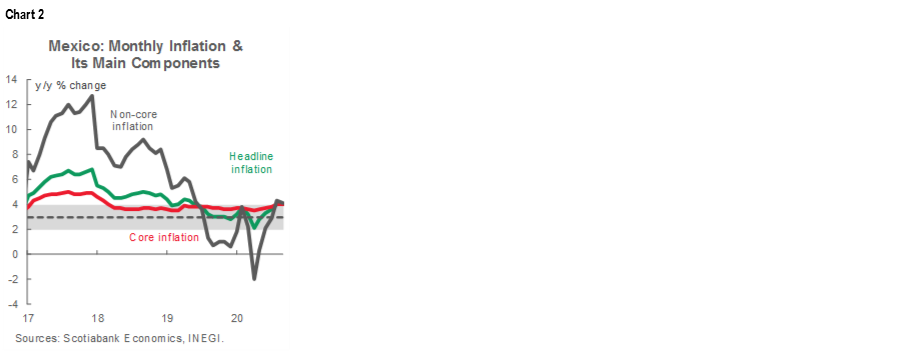

In the meeting’s minutes, published on October 8, we saw evidence of more varied views than was suggested by the Board’s unanimous vote. In fact, it appears that three of the Board’s five members noted at least some equivocations on the need for another cut in the reference rate. With inflation still above the 4% upper bound of Banxico’s target range (chart 2), we expect the Board to keep its benchmark policy rate unchanged at its November 12 meeting, but we acknowledge that growth concerns may tip the Board toward one additional final cut.

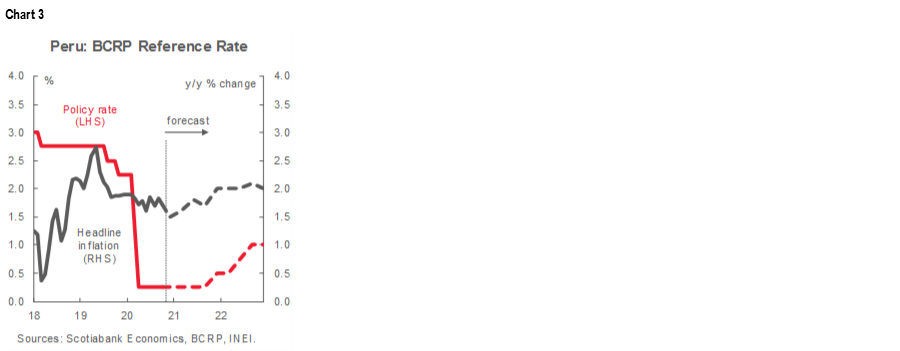

Peru. The BCRP’s Board meets on monetary policy on Thursday, November 12, and along with what is likely to be a unanimous view amongst analysts, we expect the headline policy rate to be held at 0.25%, where it has been since early April (chart 3).

In the statement from its October 7 meeting, the Board’s main messages remained unchanged from previous meetings. It held to its commitment to maintain its expansive monetary stance for a “prolonged” period of time with a bias toward the implementation of greater stimulus, if it were to become necessary, through measures other than further cuts in the policy rate. That said, our team in Lima does not have the impression that the BCRP is preparing new instruments. Instead, the Bank is focused on providing liquidity through existing channels and managing PEN volatility, some of which is being driven by intermittent political strife between Congress and the Executive.

October’s inflation reading, out on November 1, was the last key remaining input for the BCRP’s monetary-policy decision-making process. In the event, headline inflation remained stable in October at 1.72% y/y, down just a touch from September’s 1.82% y/y (chart 4). October’s print pretty much ensures that inflation will end the year higher than the BCRP’s forecast of 1.1% y/y and closer to our own projection of 1.5% y/y. However, this will not affect BCRP monetary policy, which remains focused on stimulating the economy.

—Brett House

BRAZIL: BRAZILIAN INFLATION ACCELERATED IN OCTOBER, DRIVEN BY STIMULUS AND FOOD PRICES

On Friday, November 6, Brazil’s IBGE released IPCA inflation data for October (3.92% y/y, chart 5), which printed higher than the levels expected by consensus (3.90% y/y) or ourselves (3.7% y/y). As has been the case in recent months, the bulk of the price pressures came from food and beverages (13.88% y/y), with the only other major component with inflation above 3% y/y being communications (3.38% y/y).

On a month over month basis, headline inflation rose from 0.64% m/m in September to 0.86% m/m in October, while core accelerated from 0.33% m/m to 0.71% m/m (chart 6). The components that saw the biggest increases in price growth were household goods (up 1.53% m/m), clothing (up 1.11% m/m) and food and beverages (up 1.93% m/m)—all of which were likely boosted by household stimulus, a point which was brought up by Finance Minister Guedes.

Inflation is not yet at levels which are likely to force the BCB to reconsider its forward guidance, but the pace at which its rising is concerning. However, two factors the BCB could use to look through the price spikes—at least those seen so far—are (1) it appears that some of the pressures are being driven by strong demand propped up by fiscal measures that are set to end in a couple of months; and (2) part of the food-price spike is likely to be temporary and seasonally driven, as the BCB has said.

—Eduardo Suárez

COLOMBIA: FITCH AFFIRMED COLOMBIA’S SOVEREIGN CREDIT RATING AT “BBB-”, OUTLOOK “NEGATIVE”

On Friday, November 6, Fitch kept Colombia’s sovereign credit rating at “BBB-”, the bottom of investment grade, and emphasized that the rating reflected a long record of conservative macroeconomic management that supports financial and macroeconomic stability. However, the “negative” outlook also spoke to downside risks related to fiscal consolidation and debt management in the coming years.

Fitch has taken the most critical line on Colombia amongst the credit agencies. In fact, at the beginning of the COVID-19-shock (April 1), Fitch reduced Colombia’s rating one notch from “BBB” and kept the “negative” outlook with a strong warning that the country could lose its investment-grade status. That said, through recent actions Colombia has bought some time from S&P and Fitch to deliver, finally, a structural fiscal reform next year. In contrast, Moody's rating for Colombia is still at “Baa2” (equivalent to BBB) with a “stable” outlook (table 1); it is the last credit rating agency expected to pronounce in the short term and still has room to move.

In its statement, Fitch laid out its expectations for the Colombian economy:

- A -6.9% y/y real GDP contraction in 2020 and a rebound of 4.9% y/y in 2021;

- The central government fiscal deficit would widen to -9.1% of GDP, above the current target of -8.2% of GDP for the current fiscal year, while general government debt would be expected to rise to 60.3% of GDP.

That said, Fitch warned that deficit reduction in 2022 would depend on passing fiscal reforms. The agency noted hat the Duque Government has improved its relationship with Congress and, in general, Colombia has a good record of passing and implementing key tax reforms.

All in all, Fitch affirmed that Colombia appears set to stay in the investment-grade club, but with fiscal reform in the spotlight. Fiscal reform will remain the primary concern for the credit rating agencies. We expect fiscal-policy discussions to begin as soon as the experts' commission on tax benefits release its initial recommendations in the first half of 2021.

—Sergio Olarte & Jackeline Piraján

MEXICO: INVESTMENT REBOUNDED IN AUGUST; CONSUMPTION REFLECTED WEAK DOMESTIC DEMAND; IMF ARTICLE IV CONSULTATION

I. Investment rebound in August

On Friday, November 6, INEGI published August’s gross fixed investment (GFI) data that showed a 5.7% m/m sa gain, a further recovery from July’s 3.5% m/m increase. This is the third consecutive month where monthly GFI growth remained on positive ground, a reflection of the ongoing resumption and normalization of activities. Still, in the annual comparison, this produced only a small lift from -21.3% y/y in July to -17.4% y/y (chart 7), not quite as strong as the consensus expectation of -16.0% y/y. Productive investment is set to remain weak with small monthly gains for the rest of 2020, as suggested by soft capital goods imports in September.

In August’s GFI details:

- Investment in machinery and equipment was down in annual terms for a 19th month in a row and contracted at a steeper rate, going from -18.1% y/y in July to -20.6% y/y in August; its two major components, domestic and imported goods, fell by -23.1% y/y and -22.7% y/y, respectively; and

- Construction spending softened its annual decline from -23.8% y/y to -15.0% y/y, with both of its major components recording slightly smaller annual contractions: the residential sub-index went from -21.9% y/y in July to -7.5% y/y in August, and non-residential construction rose from -25.7% y/y in July to -21.9% y/y in August.

II. August private consumption data point to weak domestic demand

INEGI also released data for August on domestic private consumption, which advanced at a slower pace in its seasonally-adjusted monthly measurement. Growth slowed from 5.4% m/m in July to 1.8% m/m in August, even though the process of re-opening the country's economic activities continued. This confirmed that domestic demand remained weak, as we had anticipated. Total private consumption was still down -14.2% y/y in August, the largest contraction for any August since at least 1994 (chart 8).

Looking at private consumption’s major components, domestic goods were down -7.6% y/y, stronger than imported goods, which were still off by -21.6% y/y. The preference for domestic over imported goods was probably induced by price effects stemming from the weaker Mexican peso weakened and rising inflation, as well as the impact of lower aggregate household income due to weakness in the labour market. Services mildly attenuated their decline from -20.3% y/y in July to -18.5% y/y in August, but they still reflected an historic drop for the month of August.

We continue to expect weak domestic private consumption growth for the rest of the year as consumers are set to remain cautious in light of the highly uncertain economic environment and weak expectations in the labour market.

III. Remarks on the Article IV Consultation with Mexico

On Monday, November 2, 2020, the Executive Board of the International Monetary Fund (IMF) concluded its Article IV Consultation with Mexico and the Fund highlighted a number of key issues in the Board’s assessment, which it released on Wednesday, November 4. Unsurprisingly, the pandemic dominated the review: it was estimated that close to 12 mn jobs were lost, most which were in the informal sector. The share of the Mexican population in a state of “working poverty” went from 36% to 48%, according to data from June. All together, the burden of the pandemic has fallen hard on the most vulnerable and low-income population.

The IMF expects GDP to fall by -9.0% y/y in 2020, the deepest contraction since the Great Depression, and it anticipates that the recovery will be gradual, with persistent risk and large social and economic costs. Aligned with this view, they noted that:

- On the fiscal front, most of the IMF’s Board recommended further short-term and temporary support that is well communicated and focused, with due consideration to reflect country circumstances and safeguard medium-term fiscal sustainability. They emphasized the importance of limiting damage from the pandemic, promoting a strong recovery, and pursuing strong, lasting and inclusive growth;

- On monetary policy, the Fund’s experts were of the view that Banxico’s actions have supported the functioning of financial markets and the economy; and

- Finally, they made a series of structural recommendations that included: review of Pemex's business strategy; broadening the Mexican government’s tax base, and improving governance institutions and policies.

—Paulina Villanueva

PERU: BCRP BUSINESS SENTIMENT SURVEY SUGGESTED GREATER STABILITY; CAR SALES WERE UP IN OCTOBER

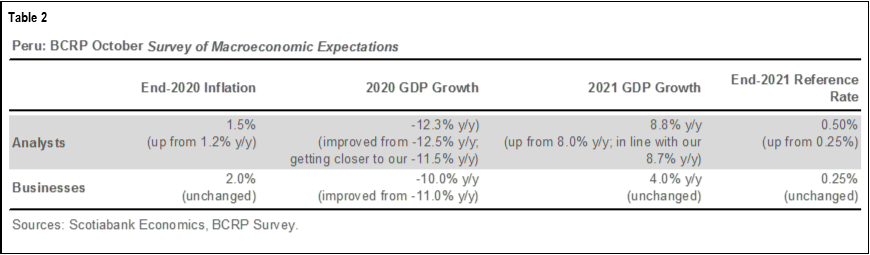

The October edition of the BCRP’s monthly survey on macroeconomic expectations, published on Thursday, November 5, produced the following responses from analysts (17 answered) and non-financial business representatives (294 answered), summarized in table 2.

The main message from the October BCRP survey was that forecasts are settling into narrower consensus ranges and changing less and less from one month to the next. This greater stability helps to produce a clearer vision of the future, which also seems to underly slightly improving sentiment in the business community.

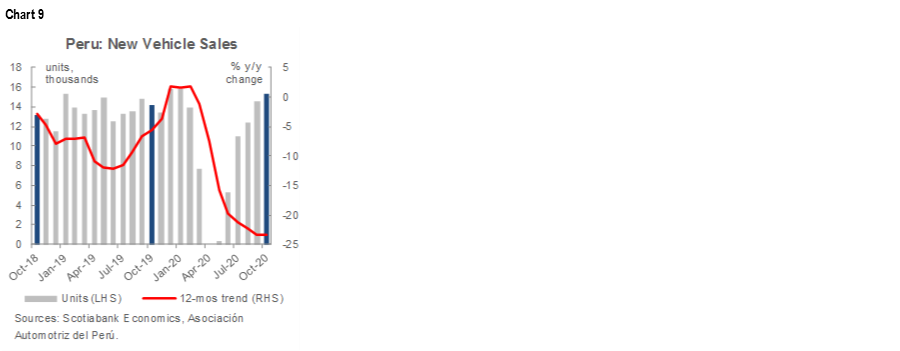

In another barometer of the rebound, new vehicle sales rose 8% y/y in October, according to data released last week by the Peruvian automobile business association, which marked a sixth straight month-on-month gain (chart 9). However, the market is still down a significant -31% y/y in the year-to-October and -23.3% y/y for the last 12 months (chart 9, again). Car (light vehicle) sales rose 7% y/y in October. This was the first month of positive annual sales growth since February, prior to the lockdown. Growth was particularly strong in pickups, which are used in construction and mining; this is yet more evidence of the extent to which construction has been picking up. Van sales were also strong, in line with the expansion of the delivery business. Truck sales also grew strongly, up 18% y/y. Unlike car sales, this was the third consecutive month of positive year-on-year growth for trucks.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.