Central banks & macro data: Minutes and October inflation

Chile: BCCh minutes point to more monetary stimulus coming, as sectoral, monthly activity, and employment data reflect a fragile recovery

Colombia: Exports stalling, unemployment falling, and the BanRep on hold

Mexico: Economy rebounded in Q3; financial activity implies that aggregate demand remained weak in September

Peru: October inflation showed that prices continue to be extraordinarily stable

CENTRAL BANKS & MACRO DATA: MINUTES AND OCTOBER INFLATION

No monetary policy decisions are scheduled this week across the Latam-6, but minutes will be published by Colombia’s and Brazil’s central banks, and four of the Latam-6 economies are reporting October inflation.

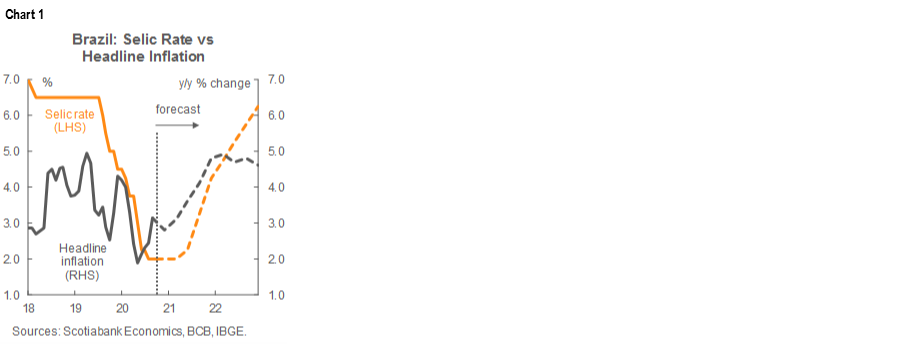

- Brazil. The BCB will publish on Tuesday, November 3 at 06:00 ET the minutes from the October 28 Copom meeting at which the Copom unanimously decided to hold the Selic rate at its record-low of 2.00% for a third meeting in a row. The minutes may provide some additional colour on two key issues. First, it will be interesting to see the Copom members’ reflections on the market response to their recent communications. More specifically, it will be particularly insightful to glean any additional detail on the Copom’s discussion of Brazil’s fiscal stance and prospects for adjustment and reform. Second, it will be useful to reset our impression of members’ views on the outlook for inflation after the recent upturn in headline IPCA readings.

- Our Brazil economist sees headline inflation rising progressively through Q1-2022, with a first increase in the Selic rate coming in Q2-2021 (chart 1).

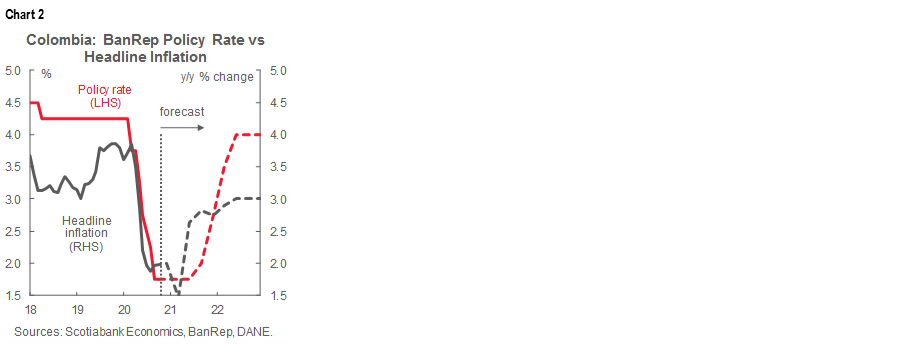

- Colombia. The BanRep is scheduled to publish on Tuesday, November 3, at 18:00 ET, the minutes of the Board’s unanimous decision to hold the benchmark interbank rate at its record-low of 1.75% at the Board's meeting on Friday, October 30. The time for the release of minutes has been moved from 14:00 ET to allow simultaneous releases in Spanish and English and will follow the publication of the BanRep’s latest quarterly Monetary Policy Report at 14:00 ET.

The minutes may shed some light on the Board’s views on how long it expects to keep its policy rate on hold and the considerations that will dominate its assessment of new developments over the coming months as it remains in data-dependent mode. Our team in Bogota doesn’t expect headline inflation to reach the BanRep’s 3% target until Q4-2021; consequently, the first policy-rate hike is forecast for late-Q3-2021 (chart 2). The Monetary Policy Report should provide updated forecasts and macroeconomic scenarios.

October inflation dominates macro data releases in Latam this week. Peru saw headline Lima inflation edge down from 1.8% y/y in September to 1.7% y/y in October in Sunday’s print (see Peru section below). October price increases are expected to have picked up in Brazil (Nov. 6); held steady in Colombia (Nov. 5); and pulled back a bit in Chile (Nov. 6). Overall, we continue to see inflation remaining well below average across Latam’s inflation targetters over our forecast horizon, with the biggest pick-up expected in Brazil (chart 3). See the Market Events & Indicators risk calendar at the back of the October 31 Latam Weekly for more details.

—Brett House

CHILE: BCCh MINUTES POINT TO MORE MONETARY STIMULUS COMING, AS SECTORAL, MONTHLY ACTIVITY, AND EMPLOYMENT DATA REFLECT A FRAGILE RECOVERY

I. Central bank minutes from October 15 meeting: we anticipate additional stimulative measures in December

In the minutes from the BCCh’s October 15 Board meeting, published on Friday, October 30, the Board recognized that a less favourable scenario is unfolding at home and abroad since its previous meeting on September 1. Although fiscal support and the withdrawal of monies from the pension funds have generated positive effects on private consumption, this impact is expected to be transitory and should not generate relevant traction in job creation, which has been timid with weak wage growth. Likewise, although inflation has increased, its origins lie in temporary liquidity injections and it isn’t a concern for the central bank. The delivery of loans has begun to slow across all segments. The external sector, which showed bouts of recovery in September, has started to slow down again with very weak imports of capital. External and internal political risks also have negative biases, which is motivating precautionary behaviour by consumers that goes beyond influences coming from the pandemic.

In this context, there is no other option for the BCCh than to recognize that the economy is set to contract between -5% y/y and -6% y/y in 2020, with a decent probability that it will land outside the range foreseen in the September Monetary Policy Report (i.e., -4.5% y/y / -5.5 % y/y), in a context where inflation is not a problem and the labour market still exhibits huge capacity gaps. The foregoing assumes that the new withdrawal of monies form the pension funds that is currently under discussion won’t happen since this would have an impact on short-term activity figures, but would not affect the medium-term scenario that we hope the BCCh will prioritize.

Consequently, the implications for monetary policy are substantial, and we anticipate additional stimulus measures from the BCCh at the Board’s December 7 meeting. These new measures could take the form of more aggressive forward guidance over the policy horizon: something like, “the monetary policy rate will not rise until there are clear signs of a sustained recovery in employment / inflation”. The BCCh may even move to re-evaluate the “technical minimum” of the monetary policy rate. The central bank could also become more active in the money market by acquiring sovereign bonds and/or taking measures in the short end of the yield curve to ensure the maintenance and transfer of low interest rates to people and firms. The BCCh’s tools are still abundant despite having used several of them over recent months. We expect that more of them will be employed in December, consistent with an adjustment in the central bank’s baseline scenario.

II. Favourable sectoral data, but IMACEC (the monthly GDP proxy) for September still showed a contraction of -5.3% y/y explained by services

Friday, October 30, saw the release of a flight of sectoral activity data for September, followed by the monthly indicator of economic activity (GDP proxy) on the morning of Monday, November 2. Altogether, this heavy data drop confirmed that the recovery continues, but that more support from monetary policy will be required to sustain it.

- Manufacturing production surprised positively in September, increasing from -8.2% y/y in August to 5.3% y/y, after five straight months of annual declines. National holidays in September boosted the production of food, particularly meat, and alcoholic and non-alcoholic beverages. Both groups contributed the most to the manufacturing expansion, helped by the temporary impulse from higher disposable income after withdrawals of pension funds. On the downside, metal products stood out for having the worse performance, which is consistent with poorer-than-expected acitvity in the mining sector during the month.

- Retail sales were very close to our forecast and consensus, with a 9.5% y/y expansion. Supermarket sales grew by 4.6% y/y and continued to be the most favoured sector during the pandemic, although they already showed a seasonally adjusted slowdown compared to August (-6.8% m/m). In September, the main gains came from large stores where there was strong demand for electronics and clothing, among other items, supported by pension withdrawals and fiscal aid. We expect to see similar results if another withdrawal from the pension funds is authorized. Even though this boost to retail activity is waning, for October, we anticipate a year-on-year expansion even greater than that observed in September owing to base effects related to last year’s social unrest.

- Mining production fell, as we expected, by -0.8% y/y, the second month of year-on-year decline after the -2.0% y/y fall in August. In September, less copper extraction and processing was observed, owing in part to lower mineral grades and smaller processing volumes amongst important companies in the sector. Stepping up production will be hard so long as the spread of COVID-19 continues to be a relevant risk. In addition, the sharp drop in the production of energy resources stands out, especially coal, crude oil, and natural gas.

September’s IMACEC headline growth number accelerated from 2.9% m/m in August (revised from 2.8% m/m) to 5.1% m/m, better than the 4.7% expected by the Bloomberg consensus. This brought the economy up from -11.3% y/y in August to -5.3% y/y in September. This leaves Q3 down -9.2% y/y, not far off our forecast of -9.0% y/y (see the October 31 Latam Weekly), but with strong sequential growth of 21% q/q to begin making up the 7.2% gap that remains from the economy’s pre-pandemic peak in early-2020 (chart 4).

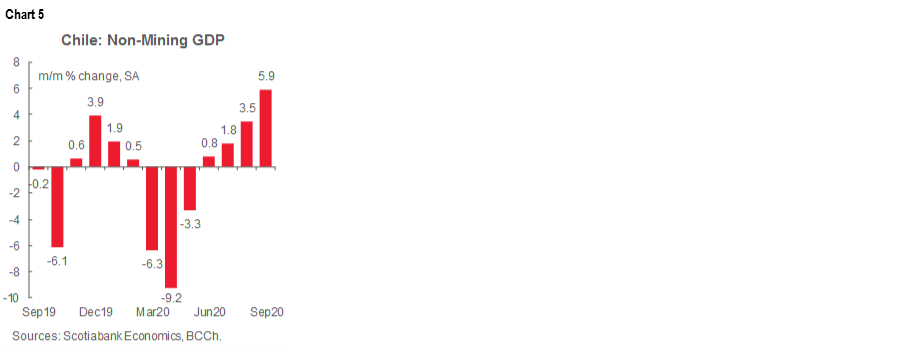

Non-mining activity gained 5.9% m/m in September, but remained down -5.7% y/y for the year (chart 5). Construction, education, transport, hospitality, and tourism remained the most affected sectors. On the positive side, commerce, manufacturing, and business services saw the strongest gains. The mining sector as a whole was still down by -1.9% y/y, but we anticipate further recovery in the coming months.

In our view, the BCCh will see these numbers as signs that more monetary stimulus will be needed at its December 7 meeting to sustain the recovery since these data imply that growth in 2020 is set to undershoot the -4.5% y/y / -5.5% y/y the central bank staff projected in its September Monetary Policy Report. Commercial credit growth is slowing, the labour market is recovering only gradually, and external demand could be hurt by the resurgence in the pandemic. Meanwhile, the BCCh should look through the recent uptick in inflation as a transitory phenomenon.

III. Employment improved in September, but still has a wide gap to close

In employment data released on Friday, October 30, the unemployment rate stood at 12.3% for the quarter between July and September, which followed 12.9% in the previous moving quarter. The decrease was explained by a somewhat greater improvement in employment than in the size of the active labour force. However, this phenomenon should be reversed in the coming months when a larger inflow to the labour force begins. This should keep the unemployment rate high (above 10%) for several quarters, unless hiring begins to gain traction along with more investment. For now, we do not see any signs of this, as investment is recovering slowly and job creation remains relatively insufficient for the size of the employment gap.

Job creation reached 172,842 in September (chart 6), but hiring growth is showing some stabilization at relatively low levels for the size of the gaps that must be closed in the coming months. The creation of self-employment has begun to take off (up about 78k), while private salaried employment stabilized with the creation of 71k jobs, slightly less than the previous moving quarter (73k). As is to be expected in a scenario of economic crisis, self-employment in commerce tends to pick up to the detriment of salaried employment, which is recovering very slowly in most sectors.

—Jorge Selaive, Carlos Muñoz & Waldo Riveras

COLOMBIA: EXPORTS STALLING, UNEMPLOYMENT FALLING, AND THE BANREP ON HOLD

I. September exports were down by -17.5% y/y and remained at USD 2.5 bn

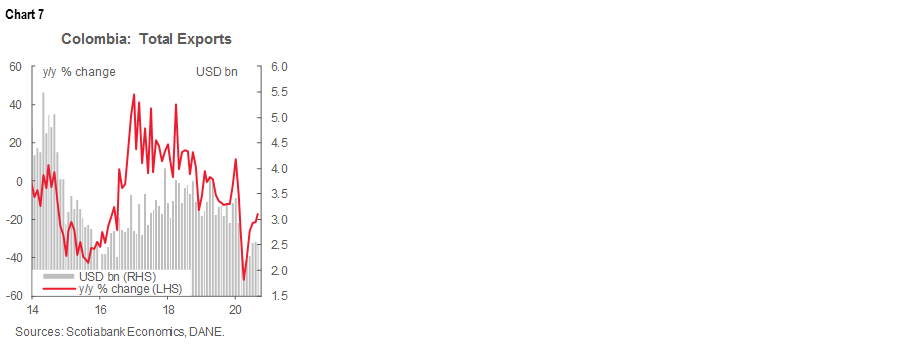

According to DANE's release on Friday, October 30, September’s monthly exports stood at USD 2.5 bn (-17.5% y/y, chart 7)—broadly the same level as the previous two months, which is the lowest point in four years. The annual contraction was a bit smaller than in August on better coffee and non-traditional exports. Oil-related exports remained the main driver of the overall annual contraction since these exports were still down -42.4% y/y, while in the previous month, they were off -39% y/y. Coal exports continued to be weak and remained down by -39% y/y. Agricultural exports were up by 22.2% y/y, while manufacturing exports were still down by -2.3% y/y.

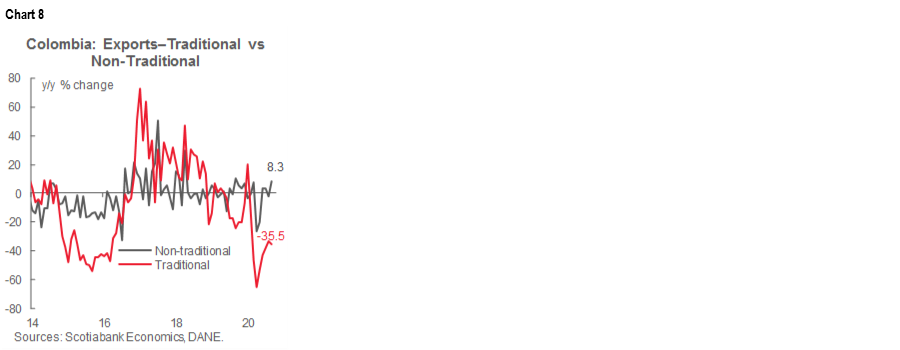

Traditional exports were off by -35.5% y/y in September, a similar pace from the previous month’s figure and at the weakest rate in four years (chart 8). Oil-related exports represented 26% of total exports compared with 40% of total exports in 2019, emphasizing a running trend. Yet, oil still provided a drag on total exports since both production and prices were weaker compared with the previous year. Similarly, coal export values were hit by both volumes and prices. On the positive side, coffee exports were up by 31.9% y/y due to better prices and volumes. Non-traditional exports amounted to USD 1.37 bn in September, up by 8.3% y/y owing to significant increases in flowers (15.6% y/y) and gold (67.7% y/y) shipments.

September’s overall export numbers showed stagnation at the same levels of the previous couple of months. New waves of COVID-19 infections could weigh on future export dynamics via lower oil prices and weaker demand from key trading partners. The impact on the current account should be moderate due to a simultaneous deterioration in exports and imports resulting from automatic stabilizers in the economy. That said, we still expect a current account deficit of about -3.2% of GDP in 2020.

II. September’s unemployment rate came down to 15.8%, jobs gains were smaller than in August

On Friday, October 30, DANE reported that in September, nationwide unemployment came in at 15.8% (September 2019 was 10.2%), while urban unemployment (i.e., across 13 cities) came in at 18.3% (September 2019 was 10.1%). The seasonally adjusted series showed that the national unemployment rate improved to 16.3% in September versus 17.1% in August 2020, while the urban unemployment rate came down from 20.4% in August to 19.4% in September—the best figures we’ve seen during the pandemic times (chart 9). September’s re-opening helped to restore jobs, although the gains were smaller than we saw in August. Employment rose by 535k jobs from August to September, bringing its total to 20.23 mn posts, still down -9% y/y from September 2019, but better than the -22% y/y gap recorded during the worst of the lockdowns. Gains are likely to continue diminishing as economic activity growth is slowing and remains below pre-pandemic levels.

September’s shift to the “new normal” re-opening scheme has allowed around 95% of the economy to resume activities, including commercial flights, hotels, gyms, and restaurants, but with restrictions remaining on massive indoor events and night clubs. Accelerated re-opening is easing trends in the labour market that boosted informality, widened gender gaps, and displaced jobs across sectors.

The most robust recoveries in employment during recent months have been in sectors with high degrees of social interaction, such as commerce, manufacturing, and construction, which at the worst part of the lockdowns accounted for more than 40% of employment contractions; in September they accounted for 24% of remaining gaps. In a shift, activities such as public administration, hotels and restaurants, and professional activities accounted for about three-quarters of lost jobs in September, which points to a big change in the labour market’s profile.

In the same vein, informality increased in urban areas from 46.9% one year ago to 48% in Q3-2020. The informal economy’s flexibility allows people to return to work more quickly than in the formal market, but this poses a considerable challenge for public policies related to tax collection, benefits provision, and economic development.

Finally, gender dynamics mark the third big change in Colombia’s labour-market profile, with women continuing to fare more poorly than men. In September, the unemployment rate for women stood at 20.7% versus 12.3% for men.

After September’s data, we expect slower job gains in the coming months while the Colombian economy is expected to continue operating below capacity. The labour market remains the biggest concern for policymakers since, at some point, it could put a cap on domestic demand and slow the economic recovery. In fact, leading indicators such as purchases with credit and debit cards are showing decreasing marginal gains compared with previous months. We still expect the unemployment rate to hit 16.4% by Q4-2020, as shown in our recent forecasts in the October 31 Latam Weekly, although after September’s labour data, our bias would be toward a slightly lower number.

III. The BanRep Board held at 1.75% in a unanimous decision; Governor Juan José Echavarría will leave office at the end of his current term

On Friday, October 30, the BanRep Board left the monetary policy rate (MPR) at 1.75% (chart 10) in a unanimous decision, as expected by market consensus. In the communiqué, the central bank emphasized that inflation expectations have increased, and that it anticipates that headline inflation would close 2020 at slightly below 2% y/y. On the economic activity side, the Board noted that the accelerated re-opening strategy, fiscal measures, and low interest rates should support economic recovery, but it highlighted that the labour market remains a significant concern.

At the end of the press conference, Gov. Echavarría noted that the current pause would last some months. So the next question is, when will the next move be? The Tuesday, November 3 release of the latest Monetary Policy Report should give further information on the BanRep’s forecasting under different macroeconomic scenarios.

Additionally, the central bank also announced that the FX NDF program will be renewed in November. The size of the outstanding program is about USD 238 mn and four expiration dates remain: November 4, 9, 12 and 18.

Additionally, Governor Echavarría made public that he would leave office by the end of his term in December 2020 due to personal issues. Echavarría emphasized that the central bank would preserve its traditional independence as an essential condition for long-term economic stability.

All in all, the BanRep’s decision met market expectations as the Board enhanced prospects for rate stability with a unanimous decision.

—Sergio Olarte & Jackeline Piraján

MEXICO: ECONOMY REBOUNDED IN Q3; FINANCIAL ACTIVITY IMPLIES THAT AGGREGATE DEMAND REMAINED WEAK IN SEPTEMBER

I. Gradual economic rebound in the third quarter

On Friday, October 30, INEGI released its preliminary third quarter GDP figures which showed that economic activity picked up from Q2-2020’s shutdowns at a record pace. On a seasonally adjusted quarterly basis, real GDP growth rebounded after five quarters of contraction and after its greatest single-quarter setback in Mexico’s modern history, accelerating from -17.1% q/q in Q2 to 12.0% q/q in Q3, in line with consensus. The third quarter’s record growth was driven by all three main sectors of the economy: services growth came up from -15.1% q/q in Q2 to 8.6%% q/q in Q3; industry growth rose from -23.4% q/q to 22.0% q/q; and agriculture growth increased from -2.0% q/q to 7.4% q/q.

In annual terms, Q3’s preliminary data implied a sixth consecutive quarter in which real GDP has fallen compared with the same period a year before: Mexico’s decline in economic activity began before the pandemic arrived. Still, the Q3 estimates implied that the pace of economic retreat has moderated (chart 11). Year-on-year growth improved from a contraction of -18.7% y/y in Q2 to -8.6% y/y Q3, just off market expectation, though still well below the -0.4% y/y pace in Q3-2019. GDP has now fallen by -9.5% y/y YTD, the biggest drop since the series began.

Agriculture also trumped industry and services in annual comparisons. Industry saw an eighth consecutive year-on-year decline, although the pullback softened from -25.7% y/y in Q2 to -8.8% y/y in Q3 (versus -1.4% y/y in Q3-2019), and services saw a sixth consecutive annual drop, which also moderated from -16.2% y/y to -8.8% y/y (versus -0.1% y/y a year earlier). Agriculture stood out with a strong recovery, moving from being down -0.5% y/y in Q2 to up 7.6% y/y in Q3 (versus 1.9% y/y in Q3-2019).

The first estimates of Q3-2020 GDP show that the economy is gradually recovering from the Q2 lockdown. However, given the persistent weakness of business and consumer confidence, and therefore of gross fixed investment and private consumption, as well pandemic-driven uncertainty, it is probable that total economic activity will not show year-on-year gains until early-2021.

—Miguel Saldaña

II. Financial activity in September pointed to ongoing weakness in aggregate demand

Banxico presented, on Friday, October 30, data on financial activity in September. Highlights included:

- Growth in bank deposits rebounded in September, going from 5.6% y/y in August to 7.7% y/y (chart 12), keeping the pace above the levels observed prior to the pandemic owing to greater dynamism in immediately payable deposits and a less profound contraction in long-term deposits;

- Direct financing and the current credit portfolio with the private sector fell for the second time in more than a decade after the business sector weakened, consumption fell further, and housing remained practically unchanged.

° Total commercial bank financing to the private sector (65% of the total) slid further (chart 12, again), from -1.7% y/y in August to -1.9% y/y in September (versus 4.3% y/y in Sep-2019). Direct financing also fell, from -1.7% y/y to -2.0% y/y (versus 4.3% y/y a year earlier), due to softer business-sector activity—which contracted for the first time in more than a decade, an ongoing decline in consumption, and a flat housing sector;

° Total financing from commercial banks (i.e., in addition to the private sector, this includes he federal public sector, states and municipalities, and other resident sectors) saw higher real annual growth in September, going from 3.3% y/y to 4.7% y/y between August and September (versus 3.3% y/y a year earlier). This was driven by financing directed to the federal public sector that continues to see important gains, up from 21.2% y/y in August to 30.3% y/y in September (versus 6.2% y/y the previous year); and

° In line with the financing numbers, commercial banks’ current credit portfolio with the private sector (including both current and past due loans) also declined in September, from -1.4% y/y to -1.6% y/y (versus a gain of 4.6% y/y in September 2019), driven by the fifth consecutive monthly drop in its business component, which represents nearly 58% of the total. On the other hand, credit placement oriented to housing remained practically unchanged.

It is noteworthy that, despite the moderation in financial activity, the overdue portfolio of commercial banks continues to decrease. This likely reflects the impact of payment deferral facilities and debt relief that have been provided by the banks to bridge debtors through the crisis. While helping to prevent insolvencies, these measures may obscure the real level of risk in the banking system.

In sum, the September financial-sector data imply that aggregate demand, and economic activity as a whole, could take a little longer to recover than our current—already conservative—GDP forecasts foresee.

—Paulina Villanueva

PERU: INFLATION CONTINUES TO BE EXTRAORDINARILY STABLE

Data released over the weekend showed that Lima’s October inflation came in at a negligible 0.02% m/m. As a result, twelve-month inflation ticked down from 1.8% y/y to 1.7% y/y, largely in line with our expectations and our year-end forecast of 1.5% y/y (chart 13). Inflation has now been in a tight spectrum of 1.6% y/y to 1.9% y/y, below the 2% y/y mid-point of the BCRP’s target range, for over a year. The contraction in domestic demand due to COVID-19 and the related lockdown has had much less impact on inflation than expected. In fact, the persistence since March of such an unusually stable inflation rate through a period of sharp demand fluctuations is extraordinary. With the worst of the economic contraction over, it seems increasingly unlikely that disinflationary pressures will take over.

Core inflation also converged to 1.7% y/y in October. In a rather rare coincidence, but indicative of how stable inflation has become, nationwide inflation also came in at 1.7% y/y, on par with Lima’s inflation rate, which is normally treated as the headline inflation benchmark. October’s print pretty much ensures that inflation will end the year higher than the BCRP’s forecast of 1.1% y/y. However, this will not affect BCRP monetary policy, which remains focused on stimulating the economy.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.