This is our last Scotiabank Economics Latam Daily for 2020; our first edition in the new year will be published on Monday, January 11 and shall include a risk calendar for the ensuing two weeks ahead of our next Latam Charts Weekly on January 13 followed by our Latam Weekly on January 23. We wish you safe and happy holidays!

Argentina: Fresh signs of sustained recovery

Brazil: Copom minutes and Inflation Report provided BCB’s updated outlook as 2020 ends

Mexico: Banxico held at 4.25%; Survey expectations improved; 2021 minimum wage increase coming

ARGENTINA: FRESH SIGNS OF SUSTAINED RECOVERY

A trio of prints in the second half of this week pointed to some additional green shoots in Argentina’s ongoing recovery.

- INDEC released Argentina’s stale, but detailed, Q3 GDP numbers on Wednesday, December 16, and they came in a bit better than anticipated by the monthly economic activity proxy. While the monthly numbers had been tracking -10.8% y/y in Q3 and the Bloomberg consensus anticipated -10.7%, the actual quarterly contraction came in at -10.2% y/y, a solid bounce from Q2’s -19.1% y/y (chart 1). The drag in Q2 from both private consumption and investment abated, but so too did the upside from exports owing to both seasonal effects and some holdback by producers anticipating a devaluation in the ARS (chart 2).

- On Wednesday, December 16, we also got October’s industrial capacity utilization rate, which rose from 60.8% in September to 61.8% (chart 3). While this was above February’s pre-pandemic 59.4% rate, capacity utilization is seasonal and this October’s level was still below October 2019’s 62.1%. Nevertheless, the continued increase in industrial capacity utilization points to a further rise in economic activity in Q4 as capacity utilization tends to lag in downturns and lead in upturns.

- On Thursday, December 17, INDEC followed up with Q3’s jobs numbers, wherein the unemployment rate pulled back a bit from 13.1% in Q2 to 11.7% (chart 4). We had expected Q3’s growth rebound to drive the unemployment rate down a bit further to 10.4%, but more people returned to the active labour force in the midst of the extended lockdown than we had expected, with a higher share of them accepting underemployed situations.

—Brett House

BRAZIL: COPOM MINUTES AND INFLATION REPORT PROVIDED BCB’S UPDATED OUTLOOK AS 2020 ENDS

So far, 2020 has been a tough year for most organizations, including the BCB, which introduced forward guidance to its toolkit to try to flatten the local yield curve and anchor its monetary stimulus, but it did not get enough cooperation from Brazil’s fiscal authorities to achieve the central bank’s intended results. Accordingly, the Brazilian yield curve has mostly steepened since forward guidance was introduced at the BCB’s August 5, 2020, monetary-policy meeting. The country’s gross-general-government-debt-to-GDP ratio has hit 100% and roughly one quarter of the stock of debt will need to be rolled over in 2021. Related questions about fiscal sustainability were among the major concerns for the Copom in 2020 and will likely play a role in preventing very accommodative monetary policy settings from remaining in place for longer. Real rates have been hovering south of -200 bps, but this is unlikely to be allowed to persist for much longer.

Accordingly, in the last Copom minutes of 2020 regarding the Committee’s December 9 meeting, members provided guidance on their plans for the elimination of its forward guidance. In particular, the BCB stated that “since the adoption of the forward guidance, inflation expectations reversed their declining trend relative to the target for the relevant horizon. Additionally, over the coming months, the 2021 calendar year should become less relevant than the 2022 calendar year, for which projections and expected inflation are around the target”. We viewed the minutes as signaling that the BCB’s forward guidance is likely to be unwound around the end of Q1-2021.

DI rates are pricing 475 bps of hikes over the next two years and while our own forecasts in the December 13 Latam Weekly fall 50 bps short of that target, the tightening cycle we expect is more front-loaded. The BCB has not signaled any relevant disagreement with the market’s views, which imply real rates of around 3.5% two years from now—inside the IMF’s estimate of a 3.00% to 4.00% neutral range. Given our expectations for Brazilian growth, we think the economy should get back to potential at some point between late-2022 and early-2023.

The BCB’s Inflation Report (IR) made material revisions to its baseline inflation scenario from the previous release in September and its new projections are consistent with a much more aggressive interest-rate hiking cycle, such as the path that is already reflected in DI rate prices. Consistent with the Copom’s minutes, the BCB’s IR stressed a high degree of two-sided uncertainty on inflation that stems from a lack of clarity on fiscal policy. On one hand, the unwinding of economic stimulus adds a layer of volatility to the growth outlook, while on the other hand, a paucity of information on the country’s coming fiscal consolidation creates doubts over what the country’s risk premium should be going forward.

One additional item highlighted in the BCB’s IR was a finding that, since the central bank introduced forward guidance, near-term inflation expectations in the BCB’s surveys have risen materially (chart 5).

—Eduardo Suárez

MEXICO: BANXICO HELD AT 4.25%; SURVEY EXPECTATIONS IMPROVED; 2021 MINIMUM WAGE INCREASE COMING

I. Banxico’s target rate maintained at 4.25%, as expected

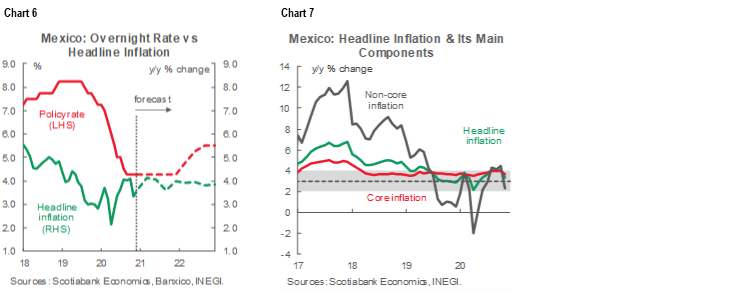

In the last monetary policy meeting of 2020, the Banco de Mexico’s Board maintained the target rate unchanged at 4.25%, as expected by most analysts and ourselves (chart 6); however, two of the five Board members voted for a rate cut of -25 bps to 4.00%. The statement noted that inflation expectations for 2020 had been reduced, owing to the recent downturn in headline CPI (chart 7), but that medium- and long-term expectations remained stable at levels above the 3.0% y/y target. The Board noted that: “Considering the aforementioned forecasts for inflation, the uncertainty that surrounds them, as well as the necessity of consolidating a downward path for headline and core inflation toward the 3% y/y target, with all members present the Banco de Mexico’s Governing Board decided by a majority to maintain the target for the overnight interbank interest rate at 4.25%,” with a reference to the balance of risks for inflation being uncertain.

The minutes of yesterday’s meeting will be published on January 7, 2021, and the next monetary policy decision is scheduled for February 11 of next year. Recall that this was the last meeting of one of the relatively hawkish members of the Board, Javier Guzmán Calafell, who will hand his seat to Galia Borja following her recent nomination by the President. Ms Borja does not appear to have a clear bias regarding Banxico’s monetary stance; however, it is broadly expected that she won’t be as hawkish as her predecessor.

For now, we maintain our projection of a hold at the Board’s next monetary-policy meeting in February, but we caution that this is subject to a fundamental review of our forecasts in January. Banxico’s Survey of Expectations now finds that most analysts expect another -25 bps cut to 4.00% to be delivered by Q2-2021.

II. Banxico Survey of Expectations shows slight improvement in growth outlook

On Thursday, December 17, Banco de Mexico published the results for December of its Survey of Expectations in anticipation of the year-end holidays. For the fifth consecutive time, respondents anticipated, on average, a smaller contraction in 2020’s GDP, moving from -9.10% y/y to a -8.99% drop. However, even though the outlook for 2020 has improved thanks to a stronger recovery than previously estimated—mainly driven by external demand—the Survey’s projected contraction would still be the steepest on record. However, the economic recovery forecast for 2021 also improved slightly from 3.29% y/y to 3.54% y/y, with a more positive bias.

Looking at the Survey’s details:

- Headline inflation expectations for end-2020 declined further, to 3.38% y/y from the previous 3.63% y/y, influenced by the “El Buen Fin” sales which lasted longer and with greater price reductions than in previous years. For end-2021, headline inflation expectations also declined, from 3.61% y/y to 3.57% y/y. We emphasize that in both the medium- and longer-term outlooks, headline and core inflation prospects remain within the target range of monetary policy;

- The exchange rate projections for end-2020 and end-2021 appreciated with respect to the November Survey; analysts now expect the peso to close 2020 at USDMXN 20.12 and to end 2021 at USDMXN 20.65;

- Regarding monetary policy, for the fourth quarter of 2020 and the first quarter of 2021, most researchers anticipate an interbank funding rate unchanged from the current target of 4.25%, although a few expect it to be lower. From Q2-2021 to Q3-2022, analysts foresee the interbank funding rate at an average of 4.00%;

- The labour market outlook remained practically unchanged, with an anticipated loss of -835k jobs (versus -832k previously) by the end of the year, with a recovery of 367k jobs (versus 360k previously) in 2021;

- As for the public deficit as a percentage of the GDP, expectations changed only marginally for 2020, from 3.86% in November’s Survey to 3.85% in December’s update; in contrast, the average view of respondents increased from 3.38% to 3.41% for the end of 2021; and

- Lastly, 100% of the consulted analysts still viewed the economy as worse off than it was a year ago, which it literally still is. The main factors they cited that could hinder Mexico’s economic growth during the next six months were: internal economic conditions (46%), governance (26%), and external conditions (15%).

III. Ambitious minimum wage increase for 2021 resisted by business councils

The National Commission on Minimum Wages (CONASAMI) agreed to increase the minimum daily wage for 2021 by 15% in nominal terms from MXN 123.22 (USD 6.16) to MXN 141.70 (USD 7.09), as had been proposed by the federal government. The decision came in line with AMLO’s objective of doubling the minimum wage by the end of his term in office in 2024: it follows on from nominal increases of 16% in 2019 and 20%, in 2020. This year, however, the increase was strongly resisted by Mexico’s business councils in the context of the pandemic, little government fiscal support, and the risk that some 700k enterprises are on the brink of disappearing from the Mexican economy over the next three months.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.