ON DECK FOR WEDNESDAY, SEPTEMBER 29

KEY POINTS:

- Bond sell-off eases

- US Congress may aim for stopgap CR today

- PBOC injects small amount of liquidity

- Is the Fed’s o/n RRP helping or hindering?

- Powell and the Phillips curve

- Was Spanish inflation a warning shot ahead of Friday?

- A celebrity CB panel won’t offer any pivots

- Canadian bond holiday tomorrow

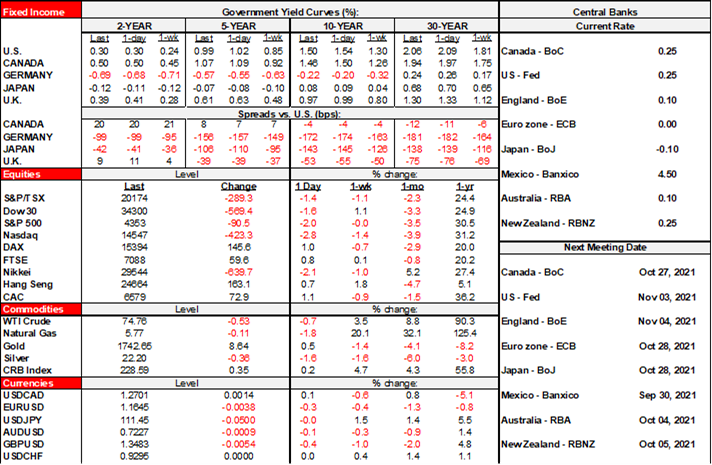

Stocks and bonds are both a bit richer this morning in at least partial reversals of yesterday’s moves. The US 10 year is down by about 3bps with Canada performing similarly and outperforming European yields in a nearly full reversal of yesterday’s move which still leaves the US 10 year yield up about 5–6bps on the week so far. US equity futures are up by ½% – ¾% with TSX futures close behind and European cash markets up by either side of 1%. Mainland China’s stocks fell by about 2% overnight. The dollar is a tad firmer but mixed across the majors.

The PBOC injected more liquidity but term repo rates continued to rise overnight. A gross amount of 100 billion yuan was injected through 14-day reverse repo. Net of maturities that worked out to just 40 billion yuan. The overnight repo rate fell by 43bps to 1.49% which is indeed the lowest since May, but the 7-day repo rate climbed 36bps to its highest since late June while the 14-day climbed 9bps to its highest since then as well (chart 1). As usual, some is seasonal demand around quarter-end, some is due to Evergrande and ahead of China’s week-long holiday. Evergrande got downgraded by Fitch overnight in a classic example of how ratings agencies lag developments. Today’s USD bond coupon payment is unlikely to be delivered and sets in motion the same 30-day grace period for monitoring default after missing the prior dollar bond payment last week.

Spain’s inflation rate for September got Eurozone inflation tracking off to a rough start ahead of the add-up on Friday. Spanish CPI was up 1.1% m/m on an EU-harmonized basis (0.9% consensus) and 4% y/y (3.6% consensus). France, Italy and Germany release tomorrow.

Calendar-based risk is very light. There was nothing material out overnight and this morning’s calendars will be equally light. The CBs panel today (here) is likely to be of little consequence as little if anything useful ever really materializes when you give 5 folks including a moderator an hour to speak. If they wanted to pivot on anything then this is not the place to do it, but maybe they’ll sign your ball caps.

There is no early close in Canada’s bond market today ahead of tomorrow’s federal holiday when stocks will be open.

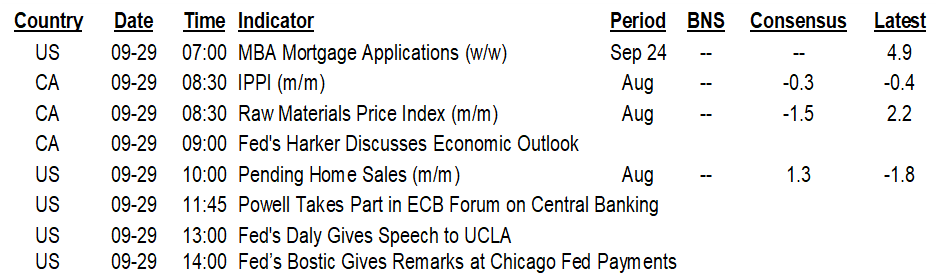

UNITED STATES

Only pending home sales for August is on tap (10amET).

We may see a voting process begin today on a continuing resolution to fund the US government until December 3rd as a stop gap measure. This would be absent any ability to achieve something grander on the multiple issues facing Congress and it keeps the other issues alive.

Tied up in all of this mess in Congress is the bipartisan infrastructure bill as the euphemistically termed “progressive” Dems in the House say they won’t support it in a likely vote on Thursday unless the broader $3.5T Build Back Better Act that emphasizes social spending and targeted tax measures also advances. Some Dems—like Manchin’s pivotal vote—think the US$3.5T price tag is too high and won’t support it. In order to agree on some sort of BBBA they’d have to raise or suspend the debt ceiling with 2.5 weeks to go until Yellen’s X-date, which also first requires acting to keep government open past Thursday. The GOP continues to say they won’t have anything to do with any of that and the Dems—preferring to avoid having the Dems take credit for any economic effects and preferring to advance a mid-term campaign against waste—and the White House say they require a bipartisan agreement. Given the 50–50 +1 VP tiebreaker in the Senate the Dems don’t have the required unity on all of this even within their own party to go it alone.

Easy peasy. Where’s David Beers when you need him….

A baseline view remains that default is highly improbable, but a partial shutdown and tiering/prioritization of obligations is an ongoing risk (which may resurrect the issue of how ratings agencies view prioritization that still winds up at least temporarily stiffing some obligations…). Too many people have to blink too many times in order to quickly get a sudden series of deals. That makes this quite different from past debt ceiling and funding episodes that didn’t tend to involve ~US$4.5T in stimulus hanging in the balance with a razor thin majority that can’t even lose a single vote!

Through it all the safehaven being sought is the Fed’s Overnight Reverse Repo Facility (chart 2). It is serving the purpose of draining liquidity in order to steer the short-term rates complex toward target goals. Also recall that one concern to setting up such a facility was always that it could aggravate periods of instability by diverting funds to zero risk at the Fed versus low risk in money market instruments like bills. Another US$68B got parked in the RRP facility today which has gone vertical since mid-month by adding about US$300B into it. Short-dated bill yields spiked today. A guaranteed 5bps from the Fed may well be the best spot to hang out for a time.

Fed Chair Powell missed his chance to elaborate upon inflation drivers going forward in his testimony yesterday. In response to a question about the Phillips curve driving current inflation, he simply said that the inflation we’re getting now is not a product of the Phillips curve. That’s a bit too strong of a statement. Recall the deflationary fears at the start of the pandemic and yet we’ve avoided that because of a rapid rebound that is shutting spare capacity (chart 3). As slack has rapidly diminished, it could have driven less deflationary/disinflationary pressure and going forward a move into excess demand conditions could represent the next wave of inflationary pressure over 2022–23 that could well coincide with supply chain bottlenecks. Powell should have perhaps emphasized how there are lagging relationships involved in all of this and that it’s feasible that even with a flatter Phillips curve we’ll get the next leg of inflation being derived from the closure of spare capacity on top of persistent supply chain issues.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.