ON DECK FOR FRIDAY, SEPTEMBER 24

KEY POINTS:

- China drives mild risk-off sentiment

- Evergrande default watch continues…

- …while the PBOC continues to inject liquidity…

- …and outlaws cybercurrencies

- US: New home sales, more Fed-speak

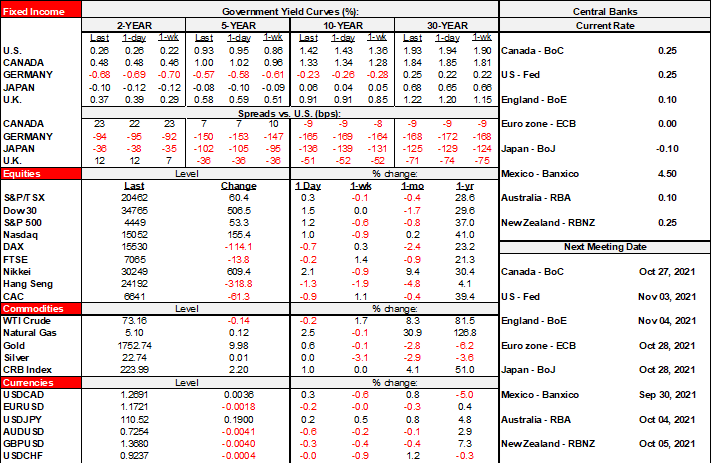

The week looks to end with a mild risk-off bias across global asset classes. US and Canadian equity futures are off by about ½% with European cash markets down by up to 1% and following declines of up to 1¼% in HK and mainland China’s exchanges. The US Ts curve is a touch flatter and the main moves in EGBs include wider Italian spreads over bunds while Australia’s and NZ’s curves sharply steepened as follow-through on yesterday’s large cheapening of Treasuries. The USD is slightly firmer.

China seems to be the main culprit and not least of which because of a lack of other notable developments. China headlines included three developments.

One was that Evergrande still has to make a US$83.5 million coupon payment on an 8.25% 2022 dollar bond that was due yesterday. Default risk is in the air, but there is a 30-day grace period. Regulators are increasing oversight of the uses of cash.

Second is that the PBOC continued to add more liquidity by pumping in 120 billion yuan through reverse repo transactions that netted out to 70 billion after subtracting maturities. Chart 1. There will be more next week and likely much more, given 220 billion of maturing 7-day reverse repos and ahead of the start of National Day/Golden Week that starts on Friday and with markets shut through the following Thursday.

Third is that the PBOC declared all crypto-related transactions and services to be illegal. They argue it cannot be treated as fiat currency and that cracking down on crypto mining is necessary to meet carbon goals. Bitcoin fell 6% after the headlines hit which is a flesh wound in the world of volatile crypto currencies. Still, it hasn’t been a great month for crypto currencies; bitcoin is down about 18% since September 6th. The other day’s announcement by Powell that a Fed discussion paper that will weigh the pros and cons of introducing its own cyber currency probably didn’t help. This is perhaps the continued thin edge of the wedge by way of the long-anticipated clampdown by central banks. The main motives are to preserve monopoly issuance of currencies in order to control money supply and the efficacy of monetary policy transmission mechanisms. CBs have always been willing to allow cybercurrencies to play at the margins, but not to the point at which they risk control over monetary policy and safety and soundness issues.

Nothing else mattered much overnight. German IFO business confidence slipped a touch in September’s reading. The Japanese Jibun composite PMI for September signalled a slowing pace of contraction led by slower shrinkage in services while manufacturing growth cooler a touch. Japanese CPI inflation is, whoa, hold on here (are you sitting?), well, it’s weak. Shocking. Didn’t see that coming… -0.4% y/y and 0% on core. Mexican retail sales fell again (-0.4% m/m, +0.2% consensus) which makes for the third decline in the past four months.

Canada will be quiet today and through most of next week ahead of next Thursday’s market holiday and then Friday’s July GDP with August guidance.

The US releases new home sales today (10amET) while Fed-speak should be low risk after Wednesday’s communications. Chair Powell, Vice Chair Clarida and Governor Bowman speak at a Fed Listens outreach event at 10amET while Cleveland President Mester (8:45amET), KC President George (10:05amET) and Atlanta President Bostic (12pmET) are also on the docket. I’ll publish the Global Week Ahead later today as usual.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.