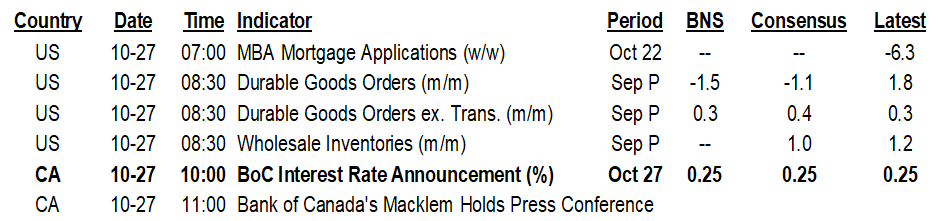

ON DECK FOR WEDNESDAY, OCTOBER 27

KEY POINTS:

- Dollar bloc front-ends cheapen on inflation, CB drivers

- BoC’s Macklem to walk a fine dovish-hawkish line

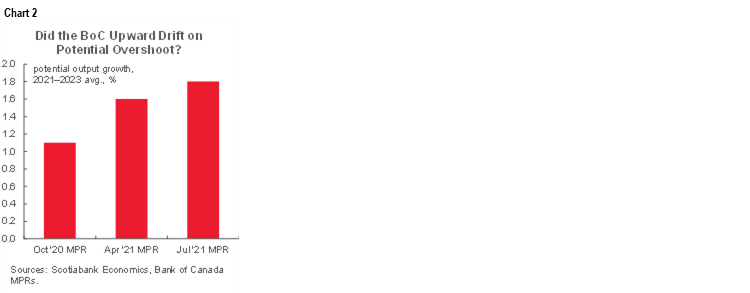

- What the BoC will do to potential GDP growth may be key

- Macklem is unlikely to do a 180-degree turn after his last three appearances

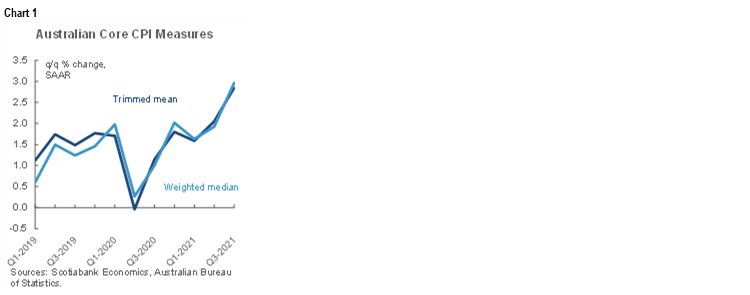

- The credibility of the RBA’s 3-yr yield target…

- …faced a bigger challenge post-CPI…

- …with spillover effects to the RBNZ

- Brazil’s central bank expected to accelerate hiking

- US core durable goods orders: the positive streak continues

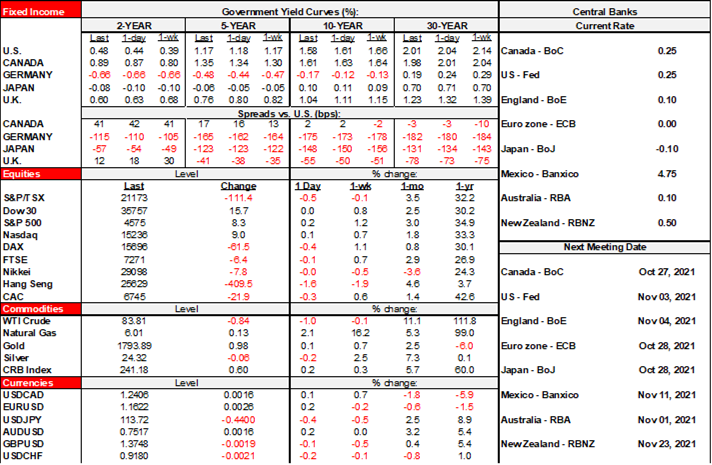

The biggest movers across sovereign curves include abrupt sell offs in both Australian and New Zealand bonds after Australian CPI surprised higher. Otherwise, the gilts and EGB curves are bull flattening with 10 year yields down 5–7bps. The US Treasury curve is bear flattening with the 2-year yield up a touch and the longer end down by ~2–3bps. Stocks are slightly in the red as Asian exchanges generally sold off overnight, European cash markets are down by ¼% to ½% and N.A. futures are little changed. The broad dollar is softening with negative risk sentiment buoying the yen and Swiss franc while CAD is slightly softer ahead of the BoC.

The credibility of the RBA’s yield target and its overall dovish policy stance is being increasingly challenged. The RBA’s 3-year government bond yield target of 0.1% was put under more strain overnight on the heels of an upside surprise to Australian inflation readings. The 3-year yield soared by 16bps to 92bps. Both trimmed mean CPI and weighted median CPI increased by 0.7% q/q non-annualized (consensus 0.5%) which pushed both measures higher to 2.1% y/y and into the RBA’s 2–3% inflation target range for headline that itself eased back to 3% y/y (3.1% consensus, 3.8% prior). The annualized and seasonally adjusted q/q rates of both central tendency inflation gauges are at the upper end of the 2–3% target range (chart 1) which leans against any temptation to dismiss it as driven by year-over-year base effects. New Zealand’s curve also sharply bear flattened with the two-year yield up 14bps.

Brazil’s CB is expected to sharply hike the Selic rate with inflation having crossed 10% y/y (5:30pmET).

CANADA

The Bank of Canada will be the main focus for many of us from about the 10amET–12pmET window. Please see yesterday afternoon’s note, the week ahead preview here and last Thursday’s deck and client conference call replay for more.

Macklem has to walk a fine dovish-hawkish line today. Briefly, I expect them to shift to the reinvestment phase, repeat that they won’t hike until slack is gone, reinforce that “considerable excess capacity” still exists after softer than expected ‘21Q1–Q3 GDP including forecast misses and negative GDP revisions with the gap poised to close later than markets have priced lift-off, and to raise nearer term inflation forecasts.

I won’t repeat the whole underlying rationale, but one key issue is that there is a lot of uncertainty around what they may do with potential GDP growth within the output gap framework. Recall that the BoC has been steadily revising it higher from a low of 1.1% y/y on average over 2021–23 in the October 2020 MPR to 1.6% in the April 2021 MPR to 1.8% in the July 2021 MPR (chart 2). They have backed off their worst estimates for damage to the economy’s productive potential compared to when they were assuming more labour market scarring and more damage to investment confidence closer to the depths of the pandemic. The evidence on material scarring is now weak at best, given the jobs recovery, while investment is ripping with equipment spending up 25% q/q SAAR in Q2 and another double digit gain being tracked in Q3. I doubt they back pedal on that upward trend in estimates of potential GDP growth over a three year time frame, or at least not by enough to shut spare capacity sooner than 2022H2. Growth has disappointed over 2021Q1–3 and some of the drivers of potential GDP have not worsened.

Relative risk-reward to what is priced around the April MPR meeting merits leaning against nearer term hike pricing. Messaging around inflation (transitory, more persistent bottleneck and supply chain issues etc) is unlikely to change at this time. Ditto around wages. In fact, I think much of the final two paragraphs in the September statement will remain intact except for the final two sentences that are likely to embrace language around the shift to the reinvestment phase.

Macklem’s comments in a media roundtable on October 14th also reinforce the tone of his two prior appearances that were recapped here. The lack of a published transcript and public appearance make us more reliant upon the media’s varied reporting than was the case during his two prior events, but here is the broad tone of what he said less than two weeks ago.

- For one, he emphasized his view that inflation is being narrowly driven by one-offs, supply disruptions and transitory factors that will persist for longer than expected but that will still fade. That’s highly debatable in my view, but it’s the Governor’s view at this point and perhaps significantly influenced by his efforts to manage market expectations.

- He also indicated that there continues to be significant slack in the overall economy and the job market. On the job market, he said that recovering lost jobs “is an important milestone, but it’s not the destination.” That reinforces the scattershot approach across a suite of labour market readings in the recent discussion paper by BoC staffers. Here too the signal is debateable as I don’t think it should be the role of monetary policy to aim for perfection across all labour market outcomes and this could just be hyperbole anyway.

- On growth, Macklem said “We’re still expecting a good rebound. It may be not quite as fast as we had” in the July MPR. That’s a clear (and expected) signal that a more muted rebound after negative GDP revisions especially in Q2 will reveal wider than expected slack in the economy. The BoC has to sharply downgrade its Q3 GDP growth expectations.

- His remarks on potential GDP growth were interesting in that he didn’t take sides on the direction of potential changes, saying that there are upside and downside arguments to further revisions which implies no great conviction toward how alterations may affect the BoC’s beloved output gap framework.

- So, if inflation is a headfake, there is still slack in the economy and job markets, and the BoC (and others…) doesn’t really know what potential GDP growth will be then hike as soon as 6 months from here? Not likely imo when the Governor has said all along he won’t hike until spare capacity has been exhausted.

UNITED STATES

Durable goods orders fell by less than expected in September (-0.4% m/m, consensus –1.1%). Core orders ex-air and defence were up by 0.8% m/m (consensus 0.5%) which surpassed expectations even after considering a minor downward revision to the prior gain (0.5% instead of 0.6%). That makes this the seventh straight monthly gain in the core orders book. The order book for core equipment is reflecting the pressures on the supply chain to address capacity issues including bottlenecks.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.