ON DECK FOR TUESDAY, NOVEMBER 23

KEY POINTS:

- European fixed income hit by inflation signals, carry drags N.A. yields higher

- PMIs showcase record Eurozone price pressures

- EZ and Australian PMIs beat, UK PMIs held steady…

- …but fade near-term growth signals on the renewed COVID-19 waves in Europe

- Plenty of drama in Ottawa today…

- …as a BoC speech and the SFT land at about the same time

- Turks are paying mightily for Erdogan’s policies

- The pointless globally coordinated release of oil reserves

- Are markets too confident that the FOMC is now more hawkish?

There is a broad but generally mild risk-off tone in equities and generally in FX as European fixed income digests another round of inflationary signals while driving higher N.A. yields through carry influences. Global PMIs from the Eurozone, UK and Australia are the main focal points ahead of US PMIs and a pair of Canadian speeches. The globally coordinated release of strategic oil reserves by the US, China, Japan, India and South Korea is a farcical attempt at wrestling control of the oil market away from OPEC+. Such moves are typically transitory in their significance.

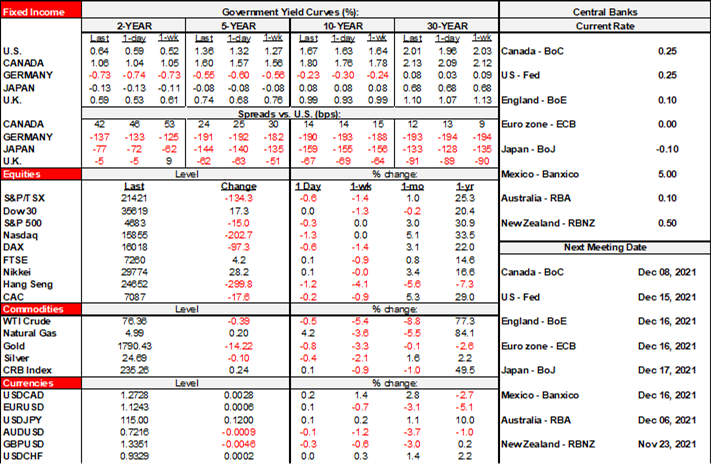

Sovereign yield curves are cheaper and mostly steeper again this morning and particularly across the Eurozone. Powell/Brainard headlines from 9amET yesterday are old news by now, so instead I’d point to another round of inflationary signals. There were more constructive signals from global PMIs than disappointing ones, but the fact that they slanted toward intensifying European price pressures with no let up in sight probably didn’t help fixed income. I would treat readings on growth in new orders and employment as stale because of COVID-19 surges in Europe.

Equities are broadly in the red, but not alarmingly so thus far. US futures are flat to down by up to ¼% with European cash markets ranging from flat (London) to off by about ¾%. Safe havens like the dollar, yen and Swissie are outperforming, but the Euro is up there with them as well. Oil was off by ~1% but is already shaking off the release of reserves by several countries.

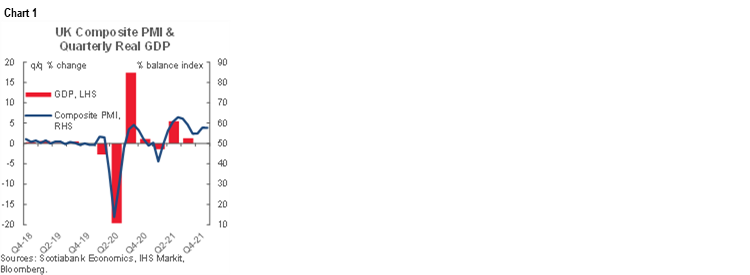

UK PMIs (here) held steady and were shaken off by gilts and sterling. The composite was unchanged at 57.7 (57.8 prior) as a statistically tiny rise in the manufacturing PMI to 58.2 (57.8 prior) was offset by a comparable drop in the services PMI to 58.6. Markit indicated that prices paid for inputs across both sectors combined rose at the fastest pace since the measure began in January 1998 with higher wages and materials prices driving the gain. Growth in new orders across both sectors picked up to a five-month high.

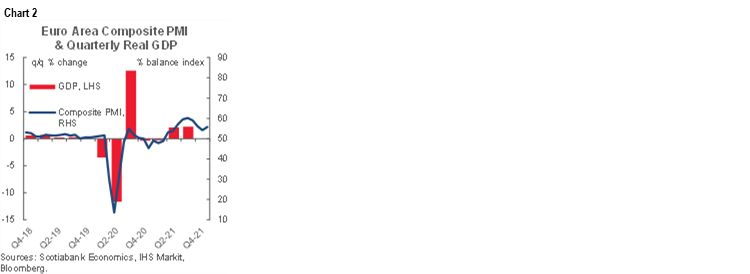

The Eurozone composite PMI (here) increased by 1.6 points to 55.8 which halted a three-month skid. That’s likely a stale assessment, however, given the sudden rise in COVID-19 cases this month. Most of the gain was led by services. Markit indicated a record gain in the price subindex, the second highest pace of job creation in over 21 years but also a 10 month low in the forward-looking outlook component due to COVID-19 and supply constraints.

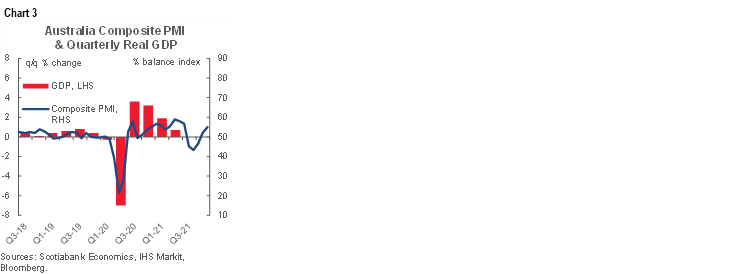

Australia’s composite PMI climbed the most of all to 55 from 52.1 and was entirely driven by an acceleration in services as reopening efforts continue to carry benefits after Australia’s prior COVID wavelet that while it was a big deal to Australian authorities paled in comparison to elsewhere.

Poor Turks. President Erdogan is destroying their currency and with it their standard of living while he rules out an election before mid-2023. The lira is in freefall in what amounts to a politically induced collapse. It is plunging by 13% this morning and has depreciated by about 55% against the USD since early September. Erdogan gave a speech last night in which he repeated calls for lower rates despite soaring inflation. Erdogan tends to get what he wants from the country’s central bank and when he doesn’t he replaces anyone in his way.

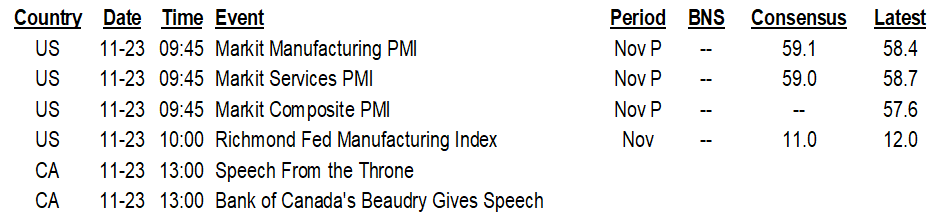

UNITED STATES

The US Markit PMI readings (9:45amET) are expected to hold their own or face upside risk partly given that we’ve seen pretty robust regional surveys thus far (eg. Philly, Empire, with the Richmond gauge due at 10amET). Recall that they cover domestic and international operations of US firms and hence why the Fed prefers the domestic-oriented ISM gauges that arrive next week.

For my two cents on the market reaction to the Fed appointments, I fail to see how taking Vice Chair Clarida out of the mix in favour of Brainard makes this a more hawkish central bank and yet that’s what at least the initial reaction in the dollar and Treasuries suggested. Reappointing Powell was the consensus expectation and Brainard offers little substantive policy difference to Powell’s view in my view (some others thought she would be more dovish…). The surprise was that Brainard took Clarida’s job instead of slipping into the Vice Chair of regs spot vacated by Quarles. Clarida had recently been positioning for a debate at the December FOMC over expedited tapering ahead of the current plan to shut down purchases by mid-2022 and that might have cost him with the Biden administration. Clarida’s candidacy for a second term might have also been torpedoed by the revelation that he traded out of a bond fund into stock funds a day before Chair Powell issued a statement that indicated a call to action against the pandemic last year, although most in the markets expected a Fed policy response by then. Clarida’s defence was that it was a “pre-planned rebalancing to his accounts” but the timing was indeed unfortunate either way and might have made for a bumpy ride in the Senate. In the end, the Dems got their choice: If Brainard couldn’t be #1, make her #2 instead of #3.

CANADA

Two Canadian speeches land at about the same time today. Unless one is a cover for the other, the simultaneous timing is fairly odd since these are the only two things going on in Canada this week and particularly Ottawa.

The BoC speech will come first at 1pmET sharp followed by roughly 1pmET or thereafter for the Speech from the Throne to be read in the Senate by Canada’s new Governor General Mary Simon.

The BoC speech by Deputy Governor Beaudry on risks to financial stability may, well, risk being interpreted as dovish by anyone who follows it less closely if they are surprised by the singular focus upon things that could go bump in the night.

The Throne Speech is mostly a political document, but the appeal to center-left Liberal-NDP tendencies is likely to include reference to implementation of the added tax on banks in addition to policy aims on immigration, social spending etc. We may get the date for the Fall fiscal update (or mini-Budget) on the back of the speech amid widespread expectations that it is likely to land in early December. Rebekah Young will have a recap of the SFT later tonight.

For more on the speeches please see the Global Week Ahead.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.