ON DECK FOR FRIDAY, MAY 7

KEY POINTS:

- Mild risk-on sentiment ahead of US payrolls

- US job growth could accelerate today…

- …as easing restrictions drove improvement across all advance readings

- Canadian jobs will likely dip in April and May…

- …until easing restrictions combine with vaccines to drive a durable jobs recovery

- ECB talk of June tapering

INTERNATIONAL

There is mild risk-on sentiment so far. US payrolls are all that matter to global markets and Canada’s jobs report will be followed in the local market. Chart 1 shows the movements in COVID-19 restrictions in the two countries that is basically the rationale behind why an acceleration of US job growth and a loss of Canadian jobs is likely to occur. Other overnight releases were relatively trivial and mostly a round-up of European industrial and export figures that are irrelevant on a day with payrolls. The one exception was a remark by an ECB Governing Council Member (Kazaks) that they could reduce the pace of PEPP EGB buying at the June meeting. Lagarde is speaking now but so far is not broaching the topic.

- US equity futures are up ¼% along with slightly firmer gains in Toronto and European equities are up as much as 1¼% in Germany.

- Sovereigns are little changed outside of cheapening in EGBs.

- The USD is flat and oil is a smidge weaker.

UNITED STATES

US payrolls are coming at 8:30amET in case that’s a surprise to anyone! Consensus is now 1 million even. I’m still at 1.3 million. The prior gain was 916k, barring revisions. The range for today runs from 700k to 2.1 million. The whisper number is 1.1 million and keeps drifting higher by the day so it’s about the same as the median across economists. The trimmed-in sample goes from roughly 750k to 1.3 million with a standard deviation of 204k. Recall that the 90% confidence interval on nonfarm payrolls is +/-110k.

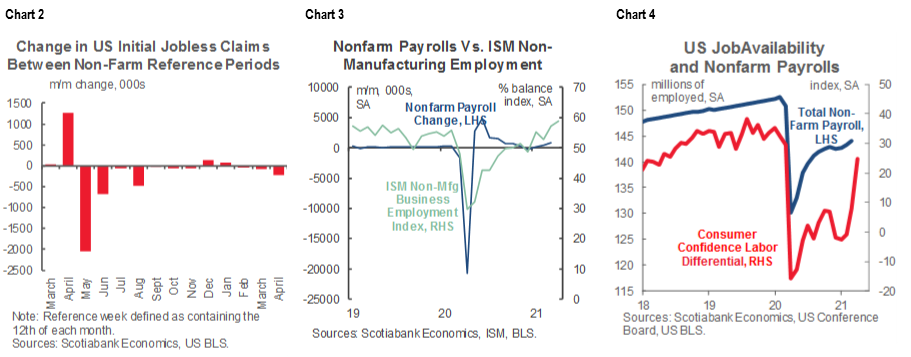

My rationale is this: There should be a material improvement in the pace of hiring over the last month based on the suite of advance indicators as restrictions eased across the US economy. I'm more confident in direction of the pace of change than in the magnitude. Restrictions measured by the stringency index are still material but at their least restrictive since last about mid-March last year. Mobility readings have picked up. Initial claims fell by more between reference periods this time than any other period since last August when payrolls went up by about 1.6 million (chart 2). ADP climbed at its fastest pace since last August. ISM-services-employment climbed to its highest since September 2018 (yes 2018). See chart 3. US consumer confidence signals on job availability soared (chart 4). Basically, everything showed an acceleration of hiring in April.

Ignore wage growth that will go from 4% y/y to zip or below as it’s a base effect and compositional issue that is not meaningful. Re-entry of lower wage workers in April over March will likely drive a weak month-over-month reading while the year-over-year reading gets rebased to April of last year after dollops of lower wage workers were disproportionately impacted by job loss and perversely drove the wage figure higher back then. Wages won’t matter until we’re into a material tightening of job markets.

What would be the biggest surprise to pricing? Since markets think the Fed is on hold for ages anyway, a surprise that recoups 25%+ of the cumulative employment shortfall in one swoop might cause foreheads to sweat over at the Eccles Building and add to taper pricing. That’s possible in my view especially with possible revisions that have been positive in 6 of the past 7 months.

CANADA

Psst….Canada’s jobs report arrives at 8:30amET too! Of course global markets couldn’t care less, but we’ll see if local markets do.

The rational here is the flipside of the US. Canada tightened restrictions after the March reference week and much of the country is going to be maintaining tightened restrictions at least through May. I’m guessing they ease ahead of the June reference week (including the 15th day of each month) and by that point we’ll get a durable jobs recovery driven by reopening and vaccines.

Consensus is -150k. I submitted -150k before knowing consensus. The prior was +303.1k. The range is from -380k to +75k. There is no whisper number for Canada, but maybe Bloomberg should start one just for giggles! There is no useful way of trimming-in the highly dispersed sample; it looks like what you get from lining up a shotgun to hit a mosquito at a couple hundred yards. That’s demonstrated by the standard deviation that is 'uuuge at 122k. That means Canada’s sample coefficient of variation is about four times what it is for US payrolls which statistically says it all. The 95% confidence interval on the monthly job change is +/-58k over the full sample history.

The main reason jobs rebounded the prior month was because restrictions eased right before the reference week that includes the 15th of each month. There was also a seasonal distortion to education employment because of the delayed Spring break. Almost right after that easing the third wave got out of hand and governments tightened up to the same level of restrictions as previously. Because the Spring break aligned with the reference week, we could see a notable drop in education sector employment. Unlike the US, the suite of advance indicators is rather poor in Canada. ADP is useless. StatsCan’s payrolls report is too lagged to matter. Ivey’s employment subindex for April unfortunately arrives after the jobs report this morning but it had previously soared (chart 5)

Ignore wage growth from this report because of distortions and because it’s not the measure the BoC watches versus its convoluted ‘wage common’ composite of four measures.

An upside risk would be if sectors participating in resource and supply chain rebounds drive enough of a lift to offset much or possibly all of the effect of tightened restrictions in service sectors. I doubt we’ll get early evidence of Census hiring that is more likely in the May figures, but watch public administration.

The additional downside risk is focused upon seasonal employment that would ordinarily begin to pick up around April–May. I mean come on, what more socially distanced activity is there than golf and you’ve gotta take that away too? Funny, but I thought all the folks with guaranteed jobs who keep saying shut the economy down until the cows come home at least played golf!

In Canada’s case I would skew tail risks to weaker rather than stronger than my guesstimate. The biggest surprise to pricing would be a positive print. Anything under -200k or so shouldn’t fuss and we might lose jobs again in May, but then reopening should lift jobs thereafter as cases recede and vaccines pick up. This is a transitory setback and my baseline assumption is that job growth steadily resumes from June onward toward recouping lost jobs by later this year ahead of the Fed.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.