ON DECK FOR FRIDAY, MAY 28

KEY POINTS:

- Markets are welcoming the US long weekend

- Early US bond market closure today

- Fed’s preferred inflation gauge should largely follow CPI higher

- US personal income expected to fall as stimulus cheques wane

- US consumer spending: will services offset weak retail?

- France’s economy double dips

- French consumer spending tanked during lockdown…

- …which means more pent-up demand coming out of it!

INTERNATIONAL

Well it will feel like a holiday in markets rather quickly today as the US long weekend arrives and after Europe goes home. Monday is sure to be a thriller. The US bond market shuts early at 2pmET today ahead of the Memorial Day long weekend. There is no early close in stocks, at least technically! So far, we’ve got a rather polite long weekend send-off brewing with a mild risk-on tone ahead of US macro data that shouldn’t carry huge surprises given previous indications. Overnight releases were of minor consequence to global risk appetite and focused upon dismal readings out of France.

- US and Canadian equity futures are up by about ¼% – ½% or so with European cash markets up by as much as ½% in Paris and Frankfurt.

- Sovereign bonds are treading water.

- The USD is little changed overall.

Unless no inflation in Japan shocks anyone, then the main overnight brow raiser came out of France where consumer spending tanked by -8.3% m/m in April (-4% consensus) and Q1 GDP was revised down a half point to -0.1% q/q non-annualized. France entered its third national lockdown at the end of March and so while estimating the magnitude of the dip in consumer spending is guesswork, the general outcome isn’t terribly surprising and just suggests there is more potential pent-up demand to unleash as the economy reopens. Downward revisions to construction spending were the main culprit behind the weaker GDP print. That technically thrust France’s economy back into technical recession after Q4 GDP fell by 1.5% q/q. Mon dieu!

UNITED STATES

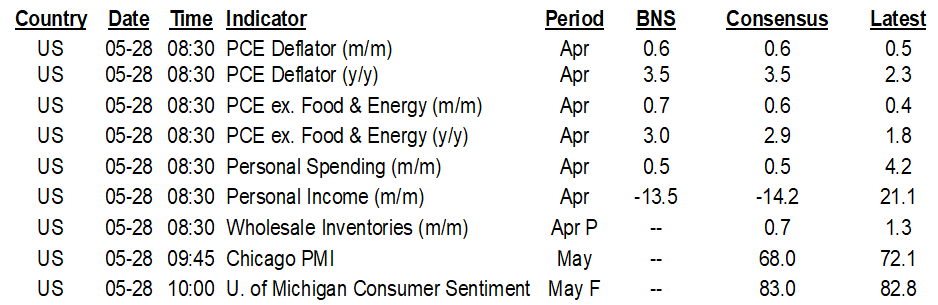

The US will release the Fed’s preferred inflation gauges plus updates on consumer incomes and spending this morning (8:30amET).

Headline PCE inflation is generally expected to follow CPI higher with prices up by 0.6% m/m and 3.5% y/y. Ditto for core PCE inflation that is expected to rise by about 3% y/y and 0.6–0.7% m/m. Note that annualized month-over-month core PCE inflation has been running at 2.4% in January, 1.1% in February, 4.4% in March and is estimated at 8.7% for today. Ignore the year-over-year and focus upon the trend in m/m SA core PCE by taking, say, a 3mth MA which is obviously not driven by base effects.

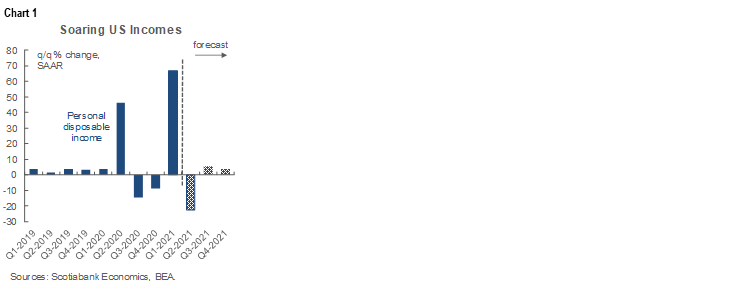

US personal income is expected to have dropped by 13.5% m/m in April’s reading. Look through it. The main driver is that about $325B of stimulus cheques went out in March versus US$61B in April and a relatively trivial amount in May so the effects of the American Recovery Act on income growth are waning but leaving behind stockpiled cash. After a 67% q/q annualized rise in personal incomes during Q1 thanks to two rounds of stimulus cheques including January’s, income is likely to contract by over 20% in Q2 before 4–5% annualized growth is likely to occur over Q3 and Q4 (chart 1).

Personal spending is forecast to rise by 0.5% on the assumption that services bounce back in a reopening economy by enough to offset the already known retail disappointment. I'd say there is more downside than upside to that but it's hard to estimate the services side.

The US also releases the advance report for the balance of trade in goods during April (8:30amET) at the same time as inventory estimates for the retail and wholesale sectors during April.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.