ON DECK FOR WEDNESDAY, MARCH 3

KEY POINTS:

- Volatile ECB-speak drives a global bond selloff

- US job market readings point to a modest rise in payrolls…

- ...as ADP’s modest rise offers no nonfarm implications...

- ...but ISM-services leans toward a modest payroll gain

- Three reasons to ignore US ISM-services

- UK budget takeaways

- Canada’s housing market is jumping over the moon

- Canada’s pandemic case tracking

INTERNATIONAL

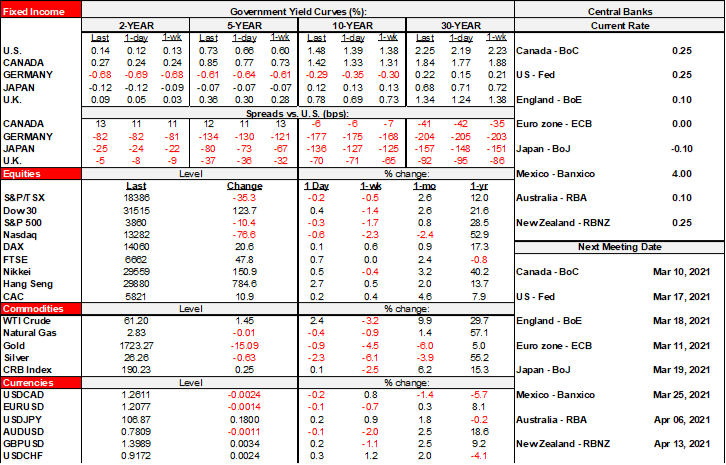

The ECB’s dog and pony show is rattling markets this morning. A dent to prospects for improved carry influences out of EGBs into global bond markets including Treasuries is one catalyst for renewed curve steepening led by about 6–9bp increases in 10s and 30s in the US, Canada and UK. Ten year EGB yields are up by 5–7bps. The USD is a little firmer against most crosses. Stocks started off more favourably but are now more mixed and little changed overall across N.A. and Europe.

The ECB hawks appear to be in greater control than the doves may have indicated since late last week, but there will remain risk into next Thursday’s ECB meeting. Volatile ECB headlines appear to be netting out toward agreement that big actions are unlikely yet maybe they’ll tweak the purchase flow within the PEPP, yet there isn’t any evidence they’ve done so thus far in the weekly transactions and there doesn’t appear to be broad-based evidence of support for doing more beyond talking about it. All this for a program with 44% utilization and guidance they might not use it all anyway before the €1.85 trillion program expires a year from now. The broad stance at the ECB is well summed up in remarks by Bundesbank President Weidmann this morning:

“I would tend to argue that the size of the movements is not such that this is a particularly worrisome development. But we have to look at it and we are ready to adjust the volume of PEPP purchases. The PEPP has that flexibility embodied in it so we can react to unwarranted tightening of financing conditions.”

Weidmann is known as a hawk but his guidance follows an early story by the always-dangerous anonymous ECB officials who say there is not big action against bond markets that is being planned.

The communications flap offers a study in contrasts between the ECB and the Fed’s purchase programs in that the ECB set a theoretical size it is not overly committed to achieving with a set expiration date that it may or may not adjust again but fiddles with the flow, versus the Fed that commits to the flow but says it doesn’t know what the ultimate size will be or how long purchases will last and creates uncertainty toward when it will adjust the flow. Jury’s out on which approach is best imo.

There were four main points that I thought were important in the UK budget (here). Overall the Budget tended to reinforce the push toward curve steepeners that ECB-speak initiated today. One is reliance upon OBA forecasts for UK GDP growth that are roughly in line with consensus for this year (4.0% versus Bloomberg consensus at 4.9%) but above consensus for next year at 7.3% (Bloomberg consensus 3.7%). Second, to get to this faster growth, a combination of reliance upon extension of multiple support measures to September—and hence well past lockdowns and broad inoculation—will be combined with generous investment write-offs. Third, the UK is the canary in the coal mine in terms of the global push toward higher taxes going forward—especially on corporations—as the tax on corporate profits will rise to 25% from 19% by 2023. The tax burden will decline in the interim for companies that invest by allowing 130% write-offs on investment, assuming that existing slack and its gradual take-up will motivate companies to invest accordingly versus the checkered history of such incentives that have been used elsewhere (e.g. Canada). Fourth, gilts issuance will be larger than guided at about £296 billion (from about £250B).

UNITED STATES

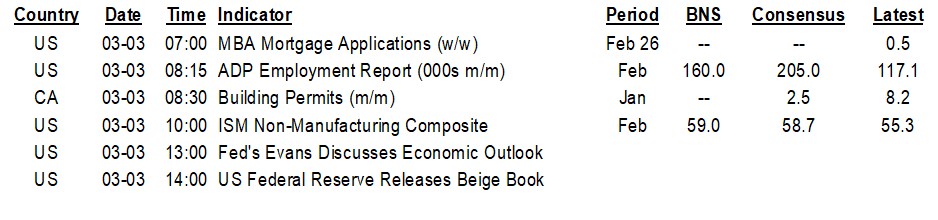

US employment readings generally support expectations for a modest rise in nonfarm payrolls on Friday. I don’t see any reason to change my nonfarm +175k guesstimate especially in light of the +/- 110,000 90% confidence interval. Two more such readings were digested today.

ADP payrolls came in somewhat softer than consensus expectations but probably offer no implications of relevance to Friday’s nonfarm payrolls report. ADP registered a rise of 117k which was about 88k lower than consensus and half that amount beneath my guess.

US ADP private payrolls, m/m change, 000s, SA, February:

Actual: 117

Scotia: 160

Consensus: 205

Prior: 195 (revised up from 174)

There are no nonfarm implications because the spread between initial ADP at 117k and the private nonfarm payrolls consensus at 200k is not statistically meaningful compared to history. As depicted in chart 1, about 15% of estimates since ADP revised methods in 2012 have been initial (pre-revisions) undershoots of 80k or more and that’s especially true this year! ADP has undershot private nonfarm payrolls by anywhere between 28k and 5.9 million since April 2020 with a median undershoot of 570k. In short, you would have needed a much, much bigger undershoot by ADP compared to the consensus for private nonfarm payrolls for it to have mattered in any obvious way before this year, let alone this year when ADP has been sharply undershooting nonfarm

ISM-services disappointed expectations in this morning’s February reading across the headline and most details. I’ll review the results but also provide three reasons why it might not matter so much.

US ISM-services, SA, February:

Actual: 55.3

Scotia: 59.0

Consensus: 58.7

Prior: 58.7

First, it’s not that this is a bad report per se in that a 55.3 reading is still materially above the dividing line of 50 that separates expansion (above 50) from contraction (below 50). Growth in a pandemic in the sector of the economy most affected by social distancing is an accomplishment.

Second, while there was no mention of this by the ISM folks, it’s feasible that shutting down power in Texas with its grid issues and frigid weather might have impacted the service sector across the region. That showed up as a drag on the petro sector in Monday’s ISM-manufacturing report but not across the rest of the country’s manufacturing sector.

Third, backward services sector data might not matter one bit with inoculation on the road map ahead. If President Biden’s forecast for enough vaccine to be available to fully inoculated the adult population by May is correct, then the social distanced services sectors stand the most to benefit.

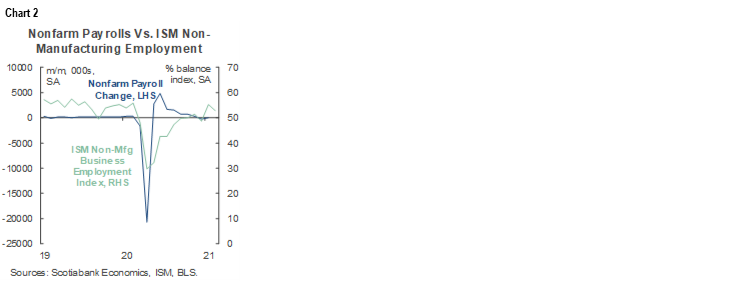

In any event, for now, we’re faced with the reality that growth nevertheless materially cooled. New orders growth pulled back sharply to a 51.9 reading from 61.8 previously. Prices paid skyrocketed, though that’s often the mirror of commodity development. Employment eased to 52.7 from 55.2. That may be a negative signal given the connection to nonfarm (chart 2).

Despite the dip in the ISM-services-employment gauge, note that it has been overshooting nonfarm payrolls for a few months now. It's hardly an airtight relationship, but this overshooting tendency might suggest that there could be positive payroll revisions or pent-up hiring demand that has yet to show up in payrolls. Or it’s just a spurious observation. See you Friday!

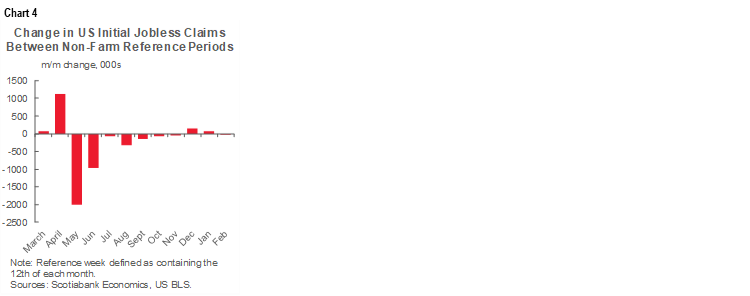

So to sum up the suite of pre-nonfarm indicators on balance I think they point toward a modest gain on Friday:

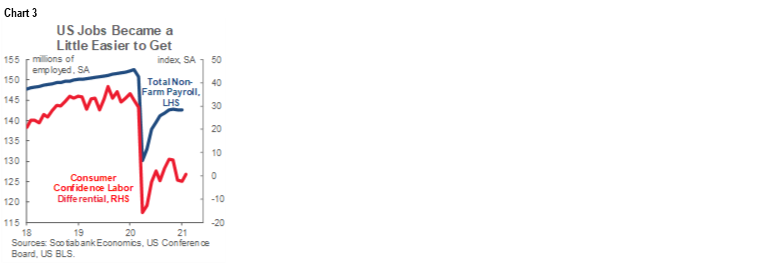

- initial claims were slightly lower between reference periods (chart 3);

- The Conference Board’s consumer confidence jobs availability reading improved a bit (chart 4);

- ISM-mfrg employment picked up smartly.

- ADP is irrelevant.

- ISM-services points to a soft employment gain.

CANADA

While not impactful to short-term markets, two additional bits of information reinforce the point about how the housing market is just off the charts. As a consequence, be on guard for macroprudential measures in a Spring budget—before end of March if spend-out is a goal, possibly April—and for the BoC implications in the context of the broader picture including yesterday’s evidence on rapid GDP growth. Ottawa has been caught completely off-guard in the magnitude of the housing response to very low financing costs.

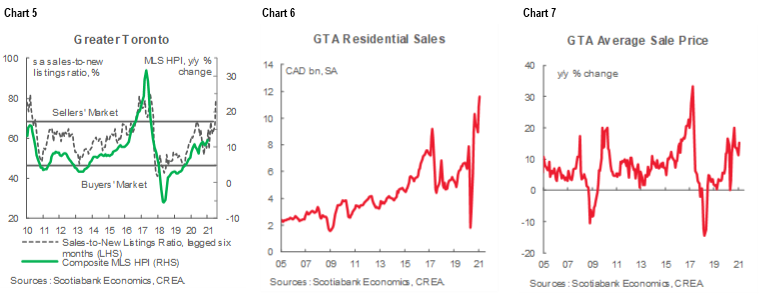

Toronto’s home sale report is available here. It builds upon the strength that was evident in the prior day’s reading out of Vancouver. Apparently, there are a lot of masochists out there who are not fussed one bit about moving in -20’C or colder weather and heavy snow! Sales were up by 15.9% m/m SA last month after being up by 3.1% m/m SA in January and 21% SA in December. Prices were up 2.3% m/m SA. Charts 5–7 provide depictions of what is happening. The level of seasonally adjusted sales is well past the moon and waving at Jupiter on the way by. Prices are accelerating. The sales to new listings ratio is deeply into sellers territory.

Further, Canadian home building is likely to remain strong. Home permit volumes were up by 7.3% m/m in January including +15.1% m/m for singles and +4.1% m/m for multiples. In year-over-year terms permit volumes were up 13% led by singles at 47% y/y (multiples +2.4%). That reinforces a move to the 'burbs kind of argument during the pandemic and points to a solid path for construction into better weather. The nonresidential side of the picture is also improving with the value of industrial permits up 31.7% m/m SA and commercial up 3.3% m/m SA.

If Canadians are taking out permits and buying resales at such a pace during winter then what does that say when the key Spring housing market and vaccines arrive? Policy is arguably overly easy and macropru changes may be afoot in a Spring budget.

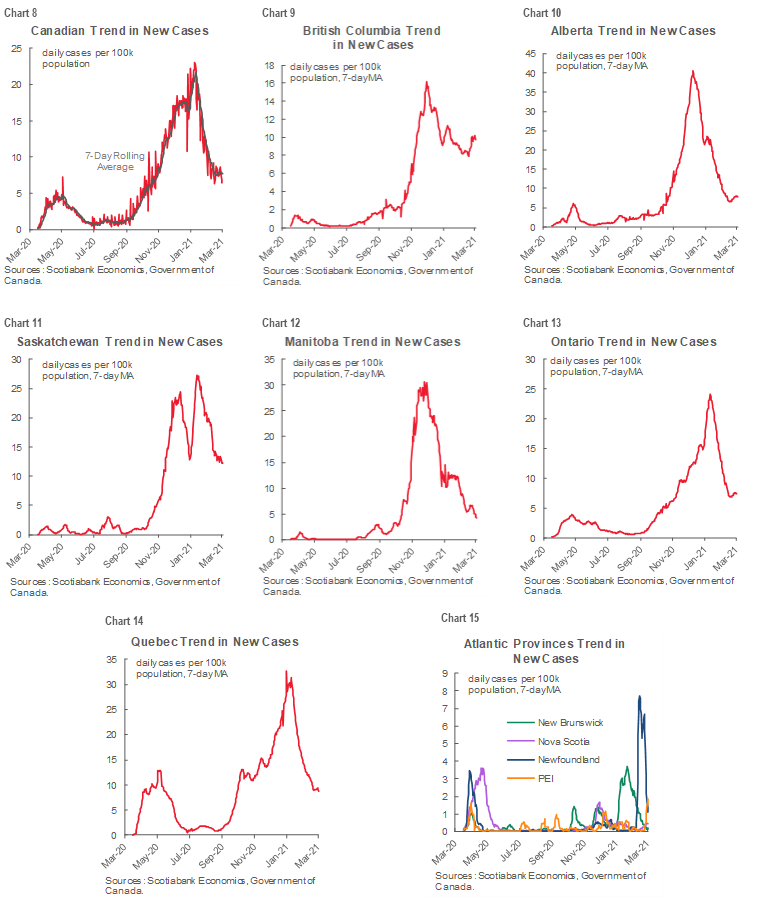

Finally, the remaining charts update Canada’s pandemic case tracking. The nationwide new case trend has moved sideways of late with regional variations depicted province by province.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.