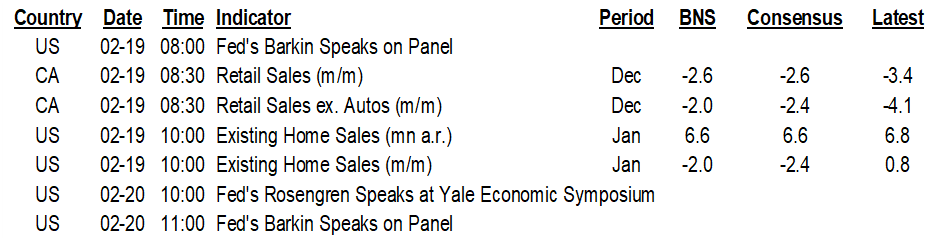

ON DECK FOR FRIDAY, FEBRUARY 19

KEY POINTS:

- Global markets ending the week with risk-on sentiment

- Oil down as good news is bad news out of Texas & Iran

- UK PMIs on the rebound…

- …but not so for Eurozone or Japanese PMIs…

- …and Australia’s expansion cooled a bit

- UK retail sales plunged during lockdown

- CDN retail sales did about what one would expect in lockdown…

- ...ahead of a likely Spring rebound

- US home sales beat, Markit PMIs flat, Fed’s MPR on tap

INTERNATIONAL

Global markets are in risk-on mode. News that Pfizer’s shot could be a one-dose wonder, the US extending an olive branch to Iran and the beginning of a Texas thaw effect on oil production are helping. Mixed global macro data is playing a minor role.

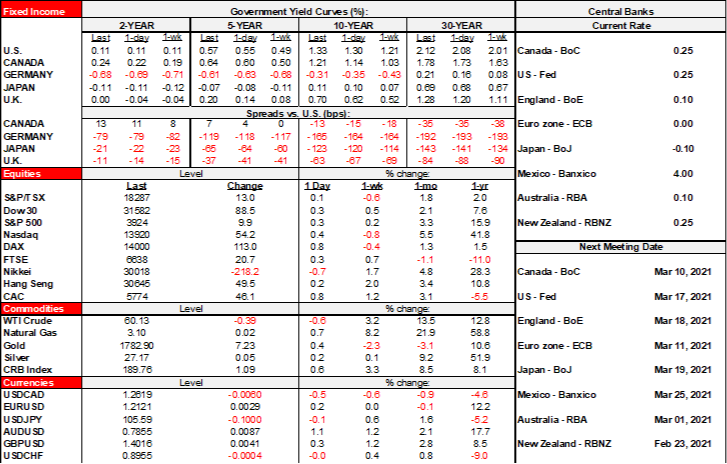

- The USD is a little softer against most major currencies except the Mexican peso. Despite lower oil, petro-currencies are mostly firmer including CAD and the Norwegian krone that are more driven by broader risk appetite.

- Sovereign 10s are cheapening again. The longer end of the US Treasury curve is up 3–4bps while all of Canada’s curve is cheaper and steepening faster than the US as Canada 10s rise 6bps with 2s up 1bps. Canada’s curve didn’t even bat an eye at smelly retail sales figures. Ten year yields are up 8bps in the UK, 2bps in Germany and Italian spreads are compressing a touch over bunds.

- Modest equity gains between ¼% and 1¼% are being registered in Europe and N.A.

- Oil, however, is off by a few dimes which is less than the selloff earlier this morning and it may be a good news is bad news thing as output problems ease in Texas and the Biden administration extended an olive branch to meet with Iran.

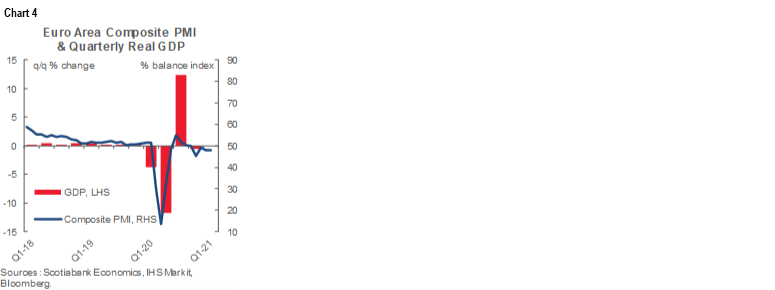

The Eurozone composite PMI slightly increased to 48.1 (47.8 prior) but the move isn’t really statistically significant and it does little to incrementally inform GDP tracking (chart 4). A nearly three-point rise in the manufacturing PMI to 57.7 signals quicker acceleration but that was offset by a slightly more rapid pace of contraction in services.

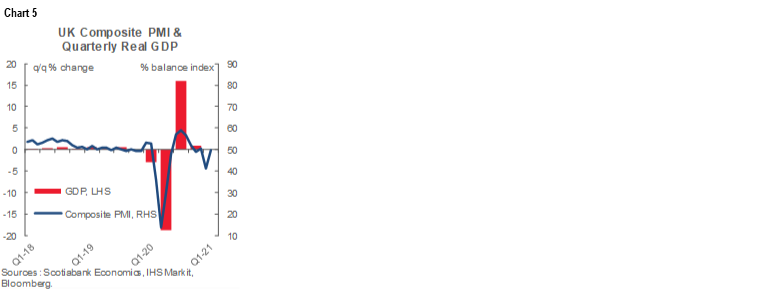

The UK composite PMI climbed by 8.6 points to 49.8 (42.6 consensus) and was mainly driven by a ten point gain in the services PMI and a 0.8 point rise in the manufacturing PMI. The improvement suggests GDP weakness is in the process of being reduced (chart 5).

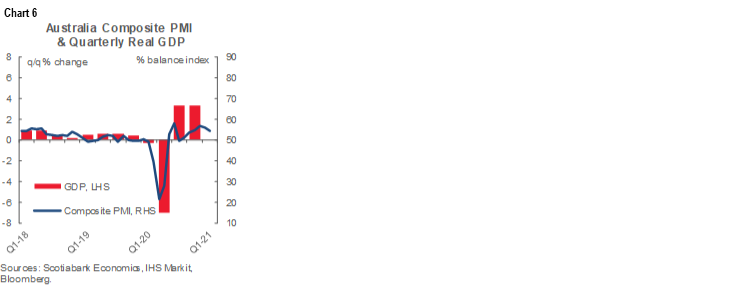

Australia’s composite PMI fell 1.5 points to 54.4 as both the services and manufacturing PMIs slipped. The reading continues to indicate correlated GDP strength (chart 6).

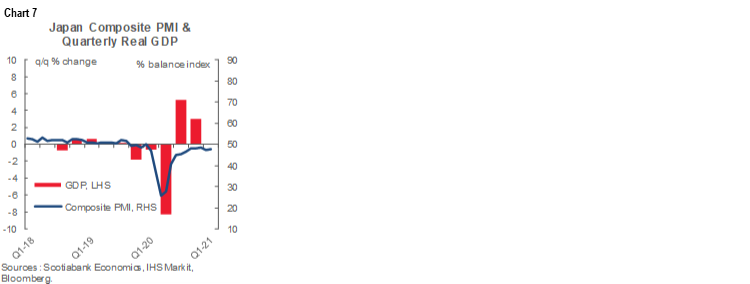

Japan’s composite PMI remained little changed in contraction territory at 47.6 with manufacturing slightly returning to mild expansion offset by contraction in services. The more modest connection with GDP is shown in chart 7.

Offsetting the UK PMIs was that retail sales plunged by much more than expected (-8.2% m/m, -3% consensus). Ex-gas also fell -8.8% m/m. Food sales were up 1.4% m/m but everything else collapsed during the lockdown.

CANADA

Well, that’s about what one would have expected in an environment of lockdowns, restrictions, stay-at-home orders and curbside shopping with dine-in eating banned. Retail sales fell sharply over the December and January period, but in the process this is creating a wicked pent-up demand argument into the Spring.

CDN retail sales, headline / ex-autos, m/m % change, SA, December:

Actual: -3.4 / -4.1

Scotia: -2.6 / -2.0

Consensus: -2.6 / -2.4

Prior: 1.8 / 2.9 (revised from 1.3 / 2.1)

January guidance: -3.3

The dollar value of sales fell by more than initially guided by StatsCan, but that was because of upward revisions to the prior month. Sales fell 3.4% m/m in December after StatsCan had previously guided they fell by 2.6% m/m, but the prior month was revised up by a half point to explain most of the disappointment in December.

What matters more is January’s advance guidance based upon the preliminary 51% ‘flash’ estimate that showed a 3.3% m/m sales decline. Again, about what one would expect. As we move toward gradually reducing restrictions and ramp up vaccinations, the stage is likely being set for a strong rebound when better Spring weather returns.

Sales volumes (-3.6% m/m) drove all of the December decline. We don’t know the volume figures for January yet, but it’s likely the same argument will hold.

Chart 1 provides a depiction of where we are in terms of the level of sales in dollar and volume terms that have lost ground but retain most of the rebound.

Chart 2 shows tracking of growth in sales volumes. They were up by about 3.3% q/q at a seasonally adjusted and annualized rate in Q4 and are tracking an 18.9% annualized drop in Q1. The uber-strong caution on the Q1 tracking, however, is that it is based solely on the Q4 jumping off point, the hand-off effect of weakness in December and hence the way the quarter transitioned into Q1 and is also based on the assumption that all of the guided drop in the dollar value of sales in January was due to lower volumes. Some of this plunge is likely to be reduced if the quarter ends more positively, but it’s still likely to be a bad quarter that sets up a probable violent swing in the other direction as sales rebound into Q2.

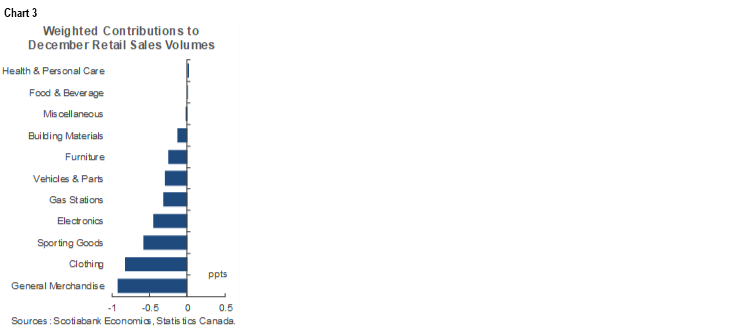

Chart 3 shows which types of retail sales drove the decline in overall sales volumes on a weighted contribution to growth basis.

Regarding the question of on-line sales, they are included if domestic, not if from foreign sources, but that wouldn’t have made a difference here. Domestic e-commerce sales were up by 69.3% y/y and are included. If you ordered off a foreign e-commerce site then that wouldn’t have been. A proxy for the latter is imports of goods through postal services and couriers in the trade accounts. That amounted to about C$598 million in December which was down from C$1.1 billion in November. A caution is that the figures are not seasonally adjusted which should have helped seasonally adjusted December numbers. A bigger caution is that the first stab at the figures is usually heavily revised. Still, the ‘normal’ monthly amount is around C$1 billion/month which is a trivial amount in comparison to total retail sales of C$53.4 billion in December.

I’ll write more about the coming consumer rebound in the Global Week Ahead later today including emphasis upon evidence surrounding the argument over if and how consumer behaviour might respond to vaccines.

UNITED STATES

The Fed’s MPR arrives later today ahead of Powell’s testimony on Tuesday–Wednesday. It’s not like the BoC’s MPR that includes full forecast updates and guidance. The Fed’s doesn’t contain forecasts and is largely descriptive in nature with just Fed staffers writing about what’s happened for the most part. It’s Powell’s opening statement on Tuesday that matters and the early part of the Q&A before it goes all political.

Light US releases include a flat Markit composite PMI at 58.8 in February and existing home sales for January that slightly increased by 0.6% m/m (consensus –2.4%) with a small upward revision. Recall the Fed prefers the ISM measures over Markit’s partly because Markit’s combine international operations of US companies whereas the Fed is more purely interested in the state of the domestic economy reflected in the ISM metrics. Home sales might follow the softening in pending home sales.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.