ON DECK FOR THURSDAY, DECEMBER 16

KEY POINTS:

- European rates sell-off as BoE surprises, ECB slows support

- The highly erratic BoE surprises again—this time with a hike

- ECB mostly met expectations…

- ...by guiding an end to the PEPP in March…

- …that probably won’t use its full envelope…

- …providing a temporary boost to the APP….

- …with PEPP and APP combining to sharply slow asset purchases over 2022...

- …but extending a longer reinvestment period…

- …while leaning against 2022 hikes again

- Norges hikes, guides another hike in March

- Banxico expected to hike today

- Global PMIs generally soften

- Australia recaptured all jobs lost over 4 months in one report

- Round up of other CBs from the zany to the unchanged and predictable

- Minor US, Canadian data

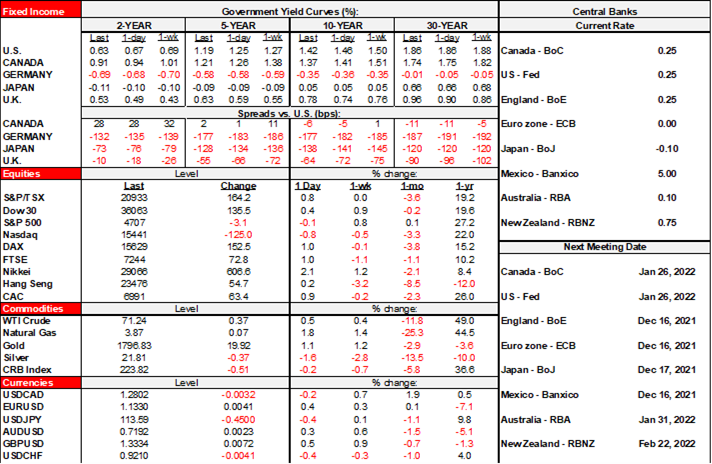

Central banks and PMIs are dominating global developments as monepalooza week kicks into higher gear today. See here, here and here for recaps of the Federal Reserve and Bank of Canada developments yesterday and today we have European central banks as the primary focus.

Stocks are rallying primarily in Europe and Canada with US equities little changed on balance. Sovereign yields are rallying in the US and Canada partly on continued relief that there wasn’t a faster pace of rate hikes telegraphed by the Fed yesterday, notwithstanding the fact the dots are partly geared toward managing markets and more of that debate will be focused upon future meetings alongside other balance sheet plans. European curves are selling off on a surprise BoE hike and slowing ECB supports. The USD is a touch softer on net as European crosses gain but alongside traditional safe havens like the yen and Swiss franc. Oil is up by about half a buck.

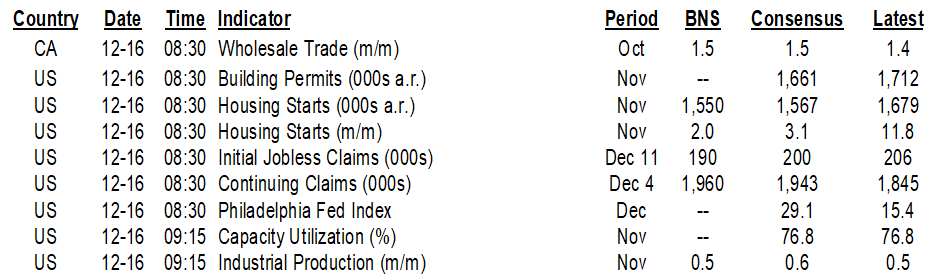

The Bank of England raised its Bank Rate by 15bps to 0.25% which surprised market pricing for no change and surprised about 80% of economists within the Bloomberg consensus. Markets reacted by bumping up expectations for future hikes (chart 1). There was a solid case for hiking now given how jobs are holding up well after the conclusion of the furlough support program, given soaring inflation and given concern that if they didn’t begin to tighten monetary policy then inflation expectations could become entirely unmoored. Omicron concerns leaned against hiking now from a growth standpoint but adds to inflation risk. But the real issue is central bank communication whereby the Bank of England has a thing or two to learn from most other central banks—outside of Turkey. After Governor Bailey guided toward a hike and then did not at the prior meeting before omicron came along, most folks had read comments from MPC members into this meeting as setting a high bar against hiking today in the face of omicron worries and raging delta + omicron cases. Here is a look at the tone of comments from MPC officials ahead of the meeting around matters like omicron’s impact and rate hike timing. My takeaway is that credibility damages market functioning, raises uncertainty and should merit setting an extremely high bar against taking strong positions in sterling or gilts ahead of BoE meetings. Companies and households cannot manage rate and FX risk affecting their operations with such an erratic central bank.

- “What are you going to do to interest rates is simply not answerable.” Ben Broadbent, December 6th.

- “…there could be particular advantages in waiting to see more evidence on its possible effects on public health outcomes and hence on the economy.” Michael Saunders, December 3rd.

- “…there are still impacts that we are feeling quite strongly.” Andrew Bailey, December 1st.

- “…it is premature to even talk about timing, much less how much,” Catherine Mann, November 30th.

- “…it will be necessary over coming months to increase Bank Rate for the inflation target is to be achieved in a sustainable manner.”

Right, so an 8–1 vote to hike after that kind of guidance makes perfect sense!!!

The European Central Bank, however, generally performed as expected but still drove a bear steepener across the EGBs curves as 10 yield yields climbed by between 1–5bps and led by Italian and peripheral spread widening over bunds. The policy decision (here) confirmed expectations on the following counts when compared to the prior statement (here).

The reason why EGB curves bear steepened was probably because the math of the combined PEPP and APP purchase programs implies less buying support not only by probably not using the full available envelope of the PEPP program but also by not replacing its purchases when the PEPP expires in March with enough of an increase in buying under the APP. Here are more details on what the ECB did:

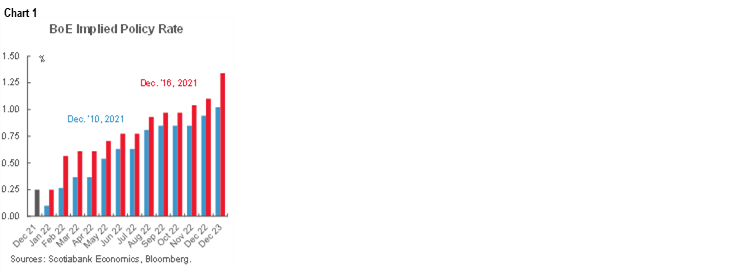

- it shifted guidance around its pandemic emergency purchase program (PEPP) from running to “at least” March to now saying “it will discontinue net asset purchases under the PEPP at the end of March 2022.” The ECB also guided that net purchases under the PEPP would be lower in Q1 than in Q4. The PEPP’s €1.85 trillion envelope is unlikely to be fully utilized. Chart 2 shows the weekly net purchase trend needed to exhaust the size of the program by the end of March versus what would happen if 2021Q1 purchases equalled the 2021Q4 average and what would happen if 2022Q1 purchases were materially lower than the 2021Q4 average.

- They also extended the PEPP reinvestment horizon “until at least the end of 2024” compared to prior guidance “until at least the end of 2023.”

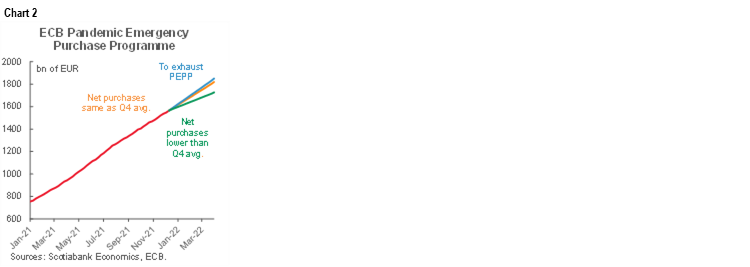

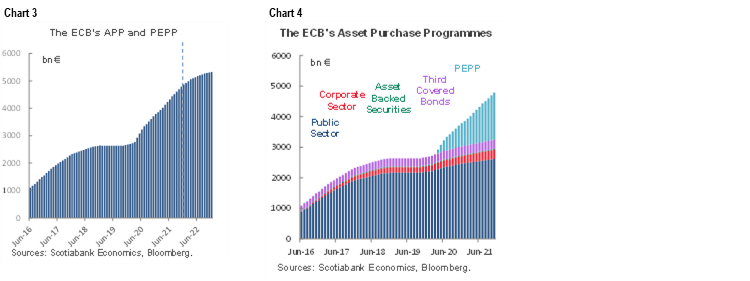

- The flow of purchases under the Asset Purchase Program (APP) was doubled from €20B/month now to €40B/month starting in Q2 after the PEPP expires. Then the ECB has guided it will taper APP purchases again toward €30B/month in 2022Q3 and then back down to the present €20B/month pace starting in 2022Q4 “for as long as necessary.” The APP boost is not enough to make up for the expiration of the PEPP’s flows and so chart 3 shows the slowing of the pace of increase in the combined purchase programs in 2022. Recall that the APP embodies the four purchase programs shown in chart 4 along side the PEPP up to the present sizes.

- The ECB leaned against 2022 hike pricing with this guidance to continue purchases and also noted it intends to reinvestment “for an extended period of time past the date when it starts raising the key ECB interest rates.”

- During her press conference, President Lagarde repeated prior guidance that it is “very unlikely” the ECB will raise its policy rate in 2022.

The Eurozone’s composite PMI fell two points to 53.4 mainly due to a 2.6 point drop in the services PMI as the manufacturing PMI continued to signal solid growth.

Australia’s rates curve underperformed others overnight after 366k jobs were gained in November. That’s enough to regain all of the jobs lost over the prior four months during which COVID-19 cases rose and lockdowns were put in place. 65% of the November gain was in part-time jobs which isn’t great, but that’s where the bulk of the jobs had been lost. The unemployment rate dropped to 4.6%.

Australia’s composite PMI slipped to 54.9 (55.7 prior). The manufacturing PMI fell the most (57.4, 59.2 prior) and the services PMI slipped to 55.1 (55.7 prior).

Japan’s Jibun composite PMI also fell by 1.5 points to 51.8 as both the services and manufacturing PMIs slipped, but especially services.

Norges Bank hiked its deposit rate by 25bps to 0.5% as universally expected. It guided that another rate hike is likely at the March meeting (skipping January). Forward rate guidance was little changed (chart 5).

Swiss National Bank held at -0.75%. Bank Indonesia held its 7-day reverse repo rate at 3.5%. Philippines also held its overnight rate at 2%. CBCT held at 1.125%. All as expected.

Turkey’s laughable central bank cut its one-week repo rate by 100bps to 14% this morning as expected.

On this side of the pond, Banxico will be the main focus across our footprint. It is expected to raise its overnight rate another ¼% to 5.25% with a minority expecting 50bps.

The US should settle back down with only relatively minor releases being taken down. Initial jobless claims were little changed at 206k (188k prior) but probably continue to be affected by seasonality issues. Housing starts soared 11.8% m/m (consensus 3.1%) in November. The Philly Fed’s volatile business gauge fell back to 15.4 (39 prior). Industrial production increased by 0.5% m/m in November (consensus 0.6% m/m) including a 0.7% m/m rise in manufacturing output for the second consecutive solid gain after a late-summer lull. Markit’s US PMIs softened a touch and drove the composite gauge down only 0.3 points to 56.9.

Canada is quiet with only a 1.4% m/m rise in wholesale trade during October to consider and that was in lien with prior guidance.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.