ON DECK FOR TUESDAY, AUGUST 31

KEY POINTS:

- ECB taper in play?

- China’s PMIs crater

- The case for looking through inflation base effects is strongest in the eurozone…

- …but an ECB hawk lights up taper talk…

- …and we may hear alternative ECB views shortly

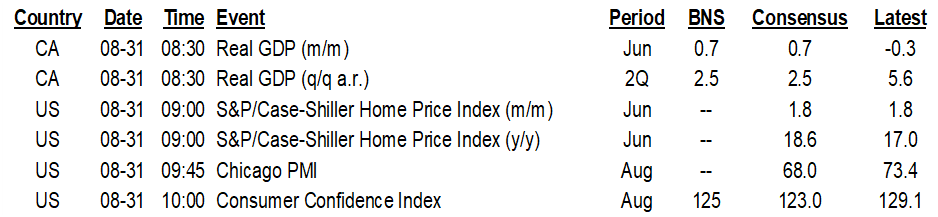

- CDN GDP to inform fresh starting point for forecasts

- Will US CB confidence fall as much as UofM?

- Chile’s CB expected to hike

- CDN elections: rates, FX and the TSX

- More auto price hikes coming

Well, global markets took the unexpected cratering of China’s economy pretty well I’d say, perhaps viewing it as transitory like everything else these days. They are not taking ECB talk as well. Anyway we have most major currencies gaining over the USD and yen safe havens. The biggest moves in sovereign bond markets are in EGBs where curves steepened as they didn’t take a spike in Eurozone inflation as transitory as perhaps they should have. There is less follow through into US Treasuries and Canadas. Stocks were doing alright with most exchanges in the black including mild gains in N.A. futures until a known ECB hawk indicated support for reducing bond buying in Q4 (Holzmann) but we could hear a different perspective from another ECB official shortly.

China’s state PMIs fell by more than expected and the broad composite PMI slipped into contraction. The composite PMI fell to 48.9 (52.4 prior) as the non-manufacturing PMI plunged by 5.8 points to 47.5. The manufacturing sector stalled with its PMI at 50.1 (50.4 prior). A reading above 50 signals expansion, below 50 contraction. While domestic COVID-19 restrictions drove much of it, export orders also weakened in both sectors. The broad details were weak. Watch the private PMIs starting tonight and Thursday night as they are more focused upon smaller non-SOE producers particularly in coastal export-oriented centers.

Eurozone inflation spiked a little higher than expected but the euro initially ignored it based on the well understood drivers and has since gained somewhat on ECB headlines and in line with other crosses to the dollar. Core inflation climbed to 1.6% y/y from 0.7% the prior month but the base effect driver was largely anticipated. Prices fell a year ago in part due to Germany’s sales tax cut. Base effects will keep inflation high until year-end when they turn the other way and so the ECB has made it clear they will look through the effects. ECB Chief Econ Lane speaks a little later (8:30amET) and is likely to reaffirm this point which could assuage any concern that the ECB is going to do anything other than bump up this year’s inflation forecast in mark-to-market fashion. Headline climbed to 3% y/y (2.2% prior) partly for the same reason and with a 0.4% m/m assist (0.2% consensus).

Germany’s labour market continues to improve. Unemployment claims fell by 53k in August (-40k consensus) for the fourth straight notable drop. There have been only two increases in claims dating back to a year ago.

French consumer spending plunged by 2.2% m/m in July (+0.2% consensus). All types of spending were weaker except energy.

Most (8 of 11 in consensus) expect Chile’s central bank to hike by 50bps with 3 expecting 25bps including Scotia’s Santiago-based economist (6pmET). Why? Inflation and with COVID-19 cases declining across LatAm. Inflation hit 4.5% y/y in July with core up to 3.6%, versus BCCh’s inflation target set at 3% over two years.

If you’d like more signs that inflation isn’t transitory and that supply chain problems are getting worse then check out headlines from Suzuki this morning. They are indicating that production is running at about 40% of normal due to semiconductor shortages and other challenges and that they are hiking prices across the board with the roll-out of new year models in September. We’ll probably see multiple car cos doing likewise and driving greater price increases than is seasonally normal. And semiconductors are hardly the only supply chain challenge affecting auto companies.

UNITED STATES

After UnivofMich consumer sentiment tanked, will the Conference Board’s measure follow suit (10amET)? I put in a decline and consensus is in the same ballpark but the decline could be much milder than the UofM measure. There are different drivers. CB is more driven by jobs. Watch the jobs plentiful reading for one of the advance nonfarm clues, plans to buy measures, and of course the inflation signal that is toward the high points of its history since 1987.

CANADA

Canada updates GDP figures this morning (8:30amET). They probably won’t matter a whole lot to forward-looking markets, but they’ll inform debates economists fret over like jumping off points for forecast revisions we are considering. A strong gain of 0.7% m/m was guided in the flash June estimate subject to revision and Q2 growth around 2½% is expected compared to the BoC’s 2% revised Q2 forecast in the July MPR. Key will be July ‘flash’ guidance with hours worked up smartly (+1.3% m/m) and very few other readings that were generally soft like advance guidance for headline retail sales and existing home sales.

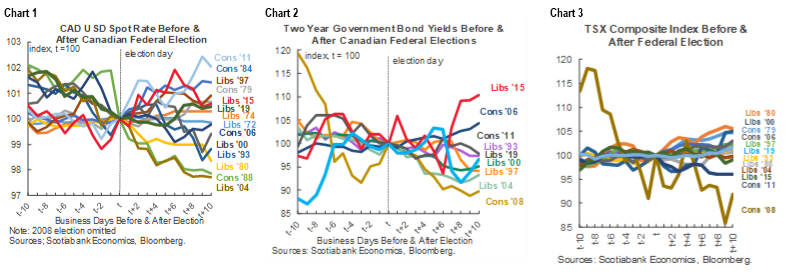

So you wanna trade the Canadian election do ya? Well, I take no responsibility whatsoever for anything that anyone sees in the Rorschach blots shown in charts 1–3. The charts follow up what I wrote in the Global Week Ahead on trading the Canadian election (hint: buy a lottery ticket instead). They show what happened to the Canadian dollar relative to the USD (falling is appreciating), Canada’s 2 year yield and the TSX starting 10 days in advance of the election day and ending 10 days after in order to provide a reasonable depiction of the event play at hand. Basically it’s a 50–50 chance whether these measures go up or down. A purist would say you have to control for a lot of other things going on each time, which is kind of the point in that a pure play on the election alone is tough to come by. This is likely truer now given relatively little substantive difference in terms of the macroeconomic, fiscal and monetary policy frameworks that would likely fall out of the election results. There may be a bit more sector differentiation, however, as party platforms surrounding the energy sector are deviating.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.