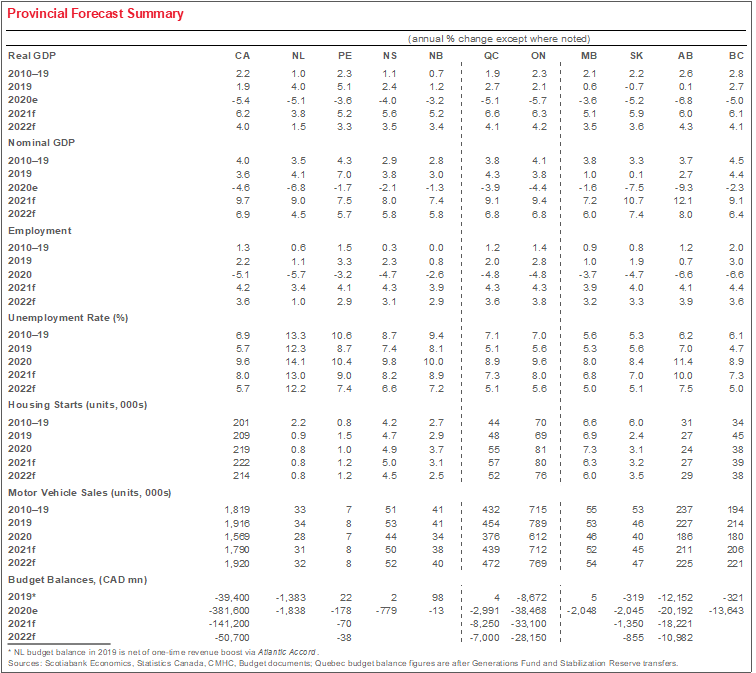

HIGHLIGHTS

We expect all of Canada’s provinces to experience strong economic growth this year as they rebound from pandemic lockdowns*.

The Canadian outlook has improved: commodity prices and recoveries from the second wave have generally surprised on the upside; the new US stimulus package and vaccination prospects offer a further boost.

We expect Quebec and Ontario to witness the strongest expansions this year, but we have also revised Alberta’s forecast growth higher in light of rallying oil prices.

In most provinces, we anticipate that consumer spending and residential investment will be the principal drivers of growth this year.

Industry divergences continue: tourism and food and accommodations are bearing the brunt of pandemic restrictions; remote-work-capable sectors are leading the rebound.

Fiscal policy remains accommodative. Some provinces have laid out tentative consolidation plans to follow pandemic spending increases, but all incorporate a degree of flexibility given the present uncertainty.

Recent commodity price gains—particularly those of crude oil—bode well for Canada’s net oil-producing regions, though it will likely take time for sectoral investment to fully recover.

We explore several macroeconomic themes and risks affecting the provinces in greater detail on pages 2 and 3.

* Forecasts completed on March 10, 2021.

PROVINCIAL MACROECONOMIC THEMES AND RISKS

COVID-19

Though this commentary tends to focus on relative infection rates and lockdown stringency levels, we emphasize that COVID-19 has profoundly impacted every provincial economy. In most cases, economic contractions witnessed last year were the deepest ever recorded. Even at this juncture, each province’s expansion will ultimately depend on its ability to get through the pandemic. Individual jurisdictions’ caseloads and restriction severities are provided in the appendix.

The outlook for the virus’ spread has improved in recent months, but remains uncertain. Second wave lockdown measures appear to have had their desired impacts and infection rates are now trending lower across most of the country. Our base case forecast assumes that widespread vaccination will enable wider reopening as the year progresses, and that even in the event of a third wave, the economic hit will be small relative to prior rounds of restrictions. Still, risks remain around the vaccine resistance of new variants, and the timing of second wave reopening.

K-SHAPED RECOVERY

The “K-shaped” name reflects the fact that some segments of the economy are growing steadily while others continue to soften; we still observe divergences across industries, and in provinces with different industry mixes. Activity in arts, entertainment, and recreation and food and accommodations services experienced a more pronounced dip during both the first and second waves (chart 1), but could witness a more meaningful the recovery as reopening proceeds. Meanwhile, higher-wage, remote-work-capable industries such as finance and insurance and professional, scientific, and technical services are above pre-pandemic levels and trending higher in many regions. Provincial economies with higher concentrations of the latter group have tended to witness the least severe downturns.

Since our last Outlook, the broad-based climb in commodity prices has also improved prospects for mining and oil and gas. Natural resources-producing provinces are reporting generally stronger production and investment intentions than just a few months ago. For oil and gas, it will likely take more time for sectoral investment to recover given the depth of the downturn last year and increasing appetite for less carbon-intensive energy production. However, the forthcoming decarbonization shift may benefit prices for certain industrial metals, and renewable energy project activity is progressing in some jurisdictions.

POPULATION GROWTH AND THE HOUSING MARKET

Population growth—especially immigration—is far off its pre-pandemic pace, and this poses downside risk in every province. Resuming pre-COVID population flows is critical to compensate for the expected aging of Canada’s population and address future labour shortages. We are cautiously optimistic that widespread vaccination, higher national immigration targets, and Canada’s status as a desirable destination for newcomers will eventually lead to a recovery*. As it stands, our forecast assumes a resumption of steady population growth this year, but there is clearly significant uncertainty on that front.

Despite the slowdown, most Canadian housing markets enter 2021 with significant momentum. For sales and housing starts, the pandemic essentially amounted to a two-month pause in March and April that was followed by some of the strongest purchasing volume gains on record (chart 2, p.1). Many cities are reporting extremely tight supply-demand balances and affordability is once again becoming stretched. Persistent softness in population growth may eventually undermine further gains. Yet, we begin this year with high-wage sectors on firm footing, low borrowing rates, household transfer supports in place, and widening supply shortages, all of which should contribute to strong residential investment and price gains this year.

FLEXIBLE FISCAL POLICY

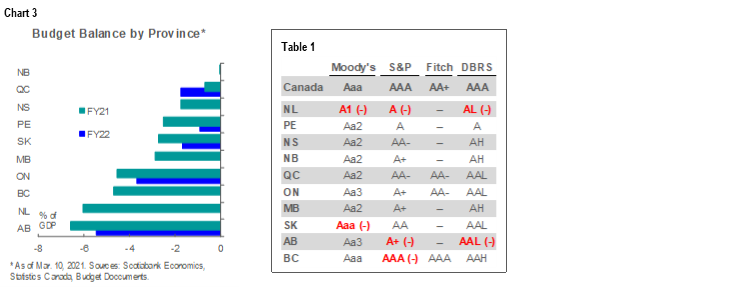

Budget season will begin in earnest shortly, which means that many Provinces will soon release their first multi-year plans since the pandemic reached Canadian shores. Those that have already released outer-year blueprints have tended to incorporate significant contingencies for cost overruns and emphasize the fluid nature of the pandemic and economic situation, and avoided concrete timelines for a return to surplus. This is likely wise given the present uncertainty and the need to balance long-run fiscal sustainability goals while bolstering the economic recovery. Still, providing reasonable medium-term fiscal anchors will be critical to signal discipline to creditors; Current provincial budget balance projections are provided in chart 3, while credit ratings are summarized in table 1.

NEW US PRESIDENTIAL ADMINISTRATION

We note four key impacts related to plans outlined by the Biden Administration. First and foremost, we expect a boost to US growth via the new fiscal stimulus package to generate meaningful gains in Canadian exports and industrial activity. Second, the imposition of “Buy American” rules to support the domestic economy may displace some Canadian firms from cross-border supply chains of which they would otherwise have been part, though the sheer strength of US growth will likely dominate. Third, clean energy development could have adverse effects on Canadian crude oil exporters, though the renewable energy sector stands to benefit alongside firms that supply inputs into the decarbonization transition. Finally, more open US immigration policy could mean more competition for skilled newcomers as reopening proceeds.

Sources for charts and tables: Scotiabank Economics, Government of Canada, Bloomberg, Rating Agencies.

* See BCG’s Decoding Global Talent, Onsite and Virtual, which ranks Canada as the preferred work destination among foreign workers.

NEWFOUNDLAND AND LABRADOR

CHALLENGING ROAD AHEAD DESPITE BETTER-THAN-EXPECTED 2020

Although we foresee a strong rebound this year, Newfoundland and Labrador’s medium-term prospects are limited by major project activity.

Last year, virus containment, crude production, and gains in other commodity prices kept the province’s decline in line with the national average (chart NL1).

Longstanding fiscal and demographic challenges remain.

What explains 2020’s results? Full-time employment recovered well in H2-2020, in part due to earlier reopening from spring lockdowns. Production of key commodities was also not as adversely impacted as in other natural resources economies. Offshore oil benefited from ramp-up of the Hebron field, while iron ore production also held up.

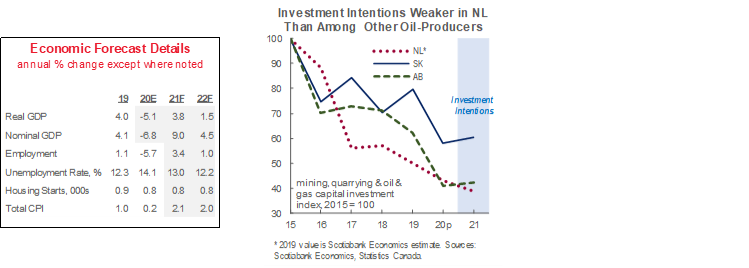

We anticipate a strong rebound in 2021, but one that is less pronounced than in other provinces. Though it has eased, a large second pandemic wave gets 2021 off to a slow start, having prompted stringent containment restrictions. Crude values have surged to start 2021, but may not immediately translate into investment and employment gains given the energy sector’s tilt towards large, long lead-time projects. NL’s soft investment intentions versus the other oil-producers appear to reflect that fact (chart). On that note, the West White Rose extension project—important for long-run output at the offshore oil field of the same name—has received a pledge of government support but work is delayed until at least 2022. Terra Nova field operations remain suspended despite support from the Province.

Fiscal challenges remain. Pre-pandemic growth prospects were limited by an uncertain oil and gas sector outlook and an aging and declining population; reining in the province’s highest-in-the-nation net debt burden and eventually returning to balance would have proved exigent. We are encouraged by federal support of $320 mn for the offshore energy industry and the contours of a deal with Ottawa for payment assistance related to Muskrat Falls hydroelectricity project debt. In the medium-term, it will be crucial for the province to safely restart immigration flows—the only consistently positive contributor to its headcount over the last several years.

The search for a buyer for the Come By Chance refinery continues. Closed since March 2020, it provided more than 400 high-wage jobs and was the sole fuel upgrading facility in the province—in 2019, petroleum refinery shipments made up over 20% of nominal exports. The shutdown was met with a surge in energy imports, which eroded gains in other sectors of the economy. Provincial funding to keep the refinery in idle mode and recent expressions of interest are positive developments.

Continued strength in key metals prices is also encouraging for export values and mining sector activity. With iron ore prices hovering at post-2011 highs, the Labrador Iron Ore Royalty Corp. expects output gains of up to 15% this year. Gold remains well-supported by accommodative global monetary policy. Moreover, output from the Voisey’s Bay nickel-cobalt mine may benefit from the coming decarbonization shift.

PRINCE EDWARD ISLAND

INDUSTRY MIX MAY HOLD BACK EVEN STRONGER RECOVERY

Prince Edward Island’s success in containing COVID-19 sets up strong growth this year, though challenges remain in some key sectors.

Homebuilding, capital outlays in the manufacturing sector, and stepped-up infrastructure spending are expected to bolster the recovery.

PEI has held the lowest per-capita COVID-19 caseload of any Canadian province for much of the last year and has yet to report a COVID-19 death. As such, lockdown measures have generally been among the least restrictive in Canada, and mobility has improved more than in most other regions. This reflects a small population and island status as well as early and decisive policy action.

Yet labour market results were mixed in 2020. PEI’s relatively subdued 3% full-time jobs loss in 2020 largely reflected pre-pandemic momentum that carried into Q1; the jobs recovery since late last summer has been among the softest of any province. Ditto for hours worked, though some improvement in hiring since October looks to have translated into Q4-2020 wage and retail sales gains stronger than the national mean.

Challenges remain in some key sectors. Tourism plays an outsized role in the Island economy; out-of-province visits are way down with travel restrictions in force. Agriculture accounted for 6% of full-time jobs before COVID-19 versus just 2% across Canada and has also held back hiring. The dairy sector—which last year made up 15% of farm cash receipts versus just 10% for Canada—is grappling with pandemic storage issues, while weak potato yields were also reported amid inclement weather. Finally, lockdown-resilient financial and technical services made up just 9% of 2019 full-time jobs versus a 16% national mean.

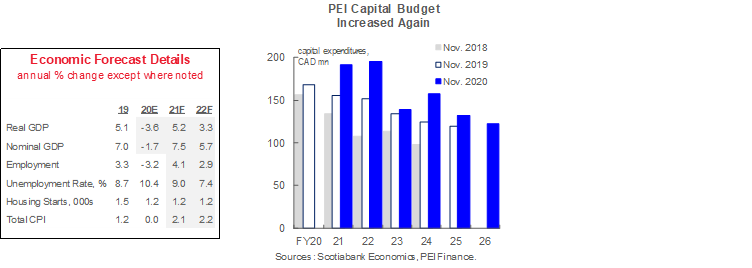

Capital spending trends are more auspicious. With a relatively sound fiscal position—its latest projections included a deficit at just 2% of output and an easing debt-to-GDP ratio—PEI raised its infrastructure budget by $45 mn in FY22 (chart). Alongside housing market tightness, social housing initiatives likely contributed to the expected 2021 capital outlay gains reported in Statistics Canada’s latest intentions survey results. That dataset also implies solid business investment gains this year for aerospace and chemicals manufacturing—two of the Island’s niche products—as well as food processing. Demand for the latter held up well during lockdowns.

The Asia-Pacific region—especially China—held an important role in PEI’s pre-pandemic trade profile. The pace of vaccination and recovery in said region should continue to influence Island trade prospects, alongside any lockdown-related logistical challenges—especially in the seafood industry.

The safe resumption of immigration flows is particularly important. PEI experienced the strongest population growth of any province during 2015–19, and newcomers accounted for three-quarters of those gains—a higher share than in any other province. Downside risk with respect to our baseline forecast therefore has potentially outsized negative consequences for the Island over the longer-run.

NOVA SCOTIA

WELL-POSITIONED AFTER STRONG SECOND HALF SHOWING

Nova Scotia bounced back from a pronounced economic hit during the first wave of the pandemic and is now positioned for very strong growth in 2021.

The presence of high-wage services industries in Nova Scotia bodes well for population growth and labour market gains.

Two key factors underpinned Nova Scotia’s outsized first half plunge. The first was its concentration of wholesale and retail trade and accommodation and food services jobs, which were disproportionately impacted by lockdowns. The second was the pre-pandemic closure of the Northern Pulp mill in Pictou County, which weighed heavily on nominal external shipments in the staple paper manufacturing industry.

Both factors appear to be easing, which contributed to a strong H2-2020 rebound. The mill’s closure is undoubtedly a blow to the community in which it operated, but the drag will likely be diminished this year. Nova Scotia’s success in limiting COVID-19’s spread—like PEI, it experienced fewer cases during the second wave than during the first—has allowed life to continue with relatively few restrictions. That, in turn, has enabled a significant labour market recovery. In January 2021, Nova Scotia was one of only two provinces in which full-time employment had returned to pre-pandemic February 2020 levels. It achieved that mark in November of last year—earlier than any other province.

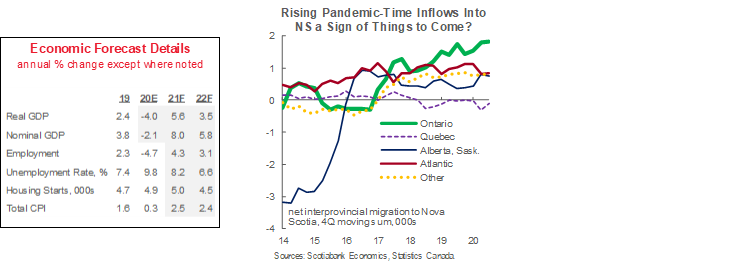

Nova Scotia’s status as Atlantic Canada’s high-wage services hub remains a key advantage. Prior to COVID-19, inflows into the province from other Canadian jurisdictions helped drive the steepest population gains in nearly 50 years, supporting labour force growth and real estate activity. Net inflows have increased since the pandemic began (chart), reflecting steady inflows and weaker outflows. Our hypothesis is that this reflects: a) a light COVID-19 caseload, and b) the presence of technology and professional and financial services that make Nova Scotia a draw to workers in other jurisdictions. These sectors tend to be more remote-work-capable and were key drivers of the province’s H2-2020 labour market rebound. Longer-run, Federal shipbuilding contracts will support the manufacturing sector.

With healthy pre-pandemic books, Nova Scotia expects to avoid record deficits and debt burdens in FY21. On the latter, it is well-positioned relative to most other provinces. Infrastructure spending was increased almost 90% versus FY20.

International immigration prospects remain uncertain as in the rest of the country. We noted the extent to which Nova Scotia has benefited from successful attraction and integration of skilled newcomers in many of our previous Outlooks.

Trade with China is another important element of the province’s outlook. Nova Scotia benefited significantly from foreign sales to the Middle Kingdom—especially in the seafood industry—before COVID-19

NEW BRUNSWICK

STRONG EXPANSION AFTER RELATIVELY MODEST CONTRACTION

New Brunswick experienced one of the smallest contractions of any province last year.

Recovering fuel consumption and surging forestry prices should support exports this year.

A small budget deficit leaves room for more fiscal policy support if needed.

Most data suggest that New Brunswick experienced one of the smallest contractions of any province last year. Full-time employment and hours worked fell by less than in any other jurisdiction. Wages and salaries rose by 0.6%—with y/y gains throughout H2-2020—versus a 1.5% national-level decline. Its business closure rate was also among the lowest in Canada. This reflects both successful COVID-19 containment—in the first wave and a resurgence in the fall—and a relatively minor level of exposure to industries most vulnerable to lockdowns.

We anticipate a strong expansion this year, though it may not reach the 6% range forecast at the national level. That partly reflects growth off of a larger base following the softer-than-average decline in 2020. As well, though a large second pandemic wave has eased, but creates a relatively soft handoff into 2021.

More optimistically, capital expenditures now appear poised for solid gains. The 10% annual jump forecast in Statistics Canada’s latest investment intentions survey was the second-highest of any province. Extremely tight supply-demand conditions in the Saint John and Moncton housing markets look to be behind the surge of almost 30% penciled in for the real estate industry. Wind power projects also look to be contributing to an expected surge in utilities industry investment.

New Brunswick is also carrying a very modest budget deficit. The Q3-FY21 fiscal update projected a deficit of just $13 mn (0.03% of nominal GDP)—the smallest output share reported by any province this year—and a still-manageable 37% net debt-to-GDP ratio. Much of the result reflects a spending undershoot related to “funding held centrally in the Supplementary Funding Provision, Investment in Climate Change Initiatives, Gaming Revenue Sharing Agreements, and pensions.” It is unclear whether these savings will persist in later years, but the province nonetheless has fiscal room to address unexpected costs or bolster its recovery where necessary. The latest capital budget raised planned outlays through FY26 (chart), with the bulk of the increases allocated to highway, road, bridge, and building improvements.

Prospects for key commodities look solid. Rising industrial activity and fuel demand south of the border should support refined crude shipments. Robust US homebuilding activity and sky-high wood prices are also positive for New Brunswick’s lumber industry, as are strong prices for Kraft pulp—used in tissue paper and packaging and in high demand amid a pandemic-induced shift to e-commerce. The orientation of provincial exports towards these commodities also limits potential downside from “Buy American” provisions and reinforces our view that US fiscal stimulus will outweigh any dampening impacts related to protectionist policy.

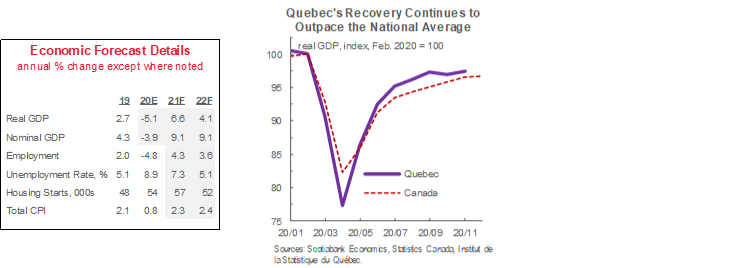

QUEBEC

WAVE 1 REBOUND AND POLICY SUPPORT DRIVE QUEBEC GROWTH

We expect Quebec’s economy to be among the top performers this year.

Despite elevated COVID-19 caseloads and strict lockdowns in the first and second waves, the province has thus far rebounded very strongly.

Downside is limited by fiscal policy support.

Though Quebec held the highest absolute and per-capita COVID-19 caseload in Canada for much of the last year, the economic data have also shown robust rebounds from every period of contraction thus far. Earlier pandemic restrictions led to output falling by more than the national mean in H1-2020, but the torrid 61% (q/q ann.) gain reported in Q3 was more than 20 ppts higher than for Canada as a whole. Similarly, Quebec’s November GDP rebound—second wave restrictions first came into effect in October 2020—leave it closer to recouping its losses than most of the rest of the country (chart). The arithmetic is such that that momentum pushes annual growth in 2021 above the national mean, even with the softer Q1 built into our forecast to reflect second wave restrictions.

Early capital spending intentions are strong and broad-based. The 7.5% increase in private-sector outlays anticipated in Quebec in 2021 as of the latest investment intentions survey trailed only Ontario; hefty gains were expected across mining, transportation and warehousing, and financial services. Infrastructure outlay boosts and pre-pandemic policy plans also look to be behind the healthy increases planned in education, health, and public administration. Over the medium-term, Quebec’s tech and financial services presence mean that its labour market is relatively able to withstand lockdown- and remote work-related challenges.

We continue to anticipate that fiscal policy will help to reinforce the recovery as vaccination efforts proceed. In addition to stepped-up infrastructure spending plans, the Province will implement a range of workforce training measures that aim to facilitate the hiring of workers as firms restart operations post-lockdown. It has also built in sizeable contingency reserves throughout its planning horizon, which should keep Quebec on track to reduce its debt load over the longer-term. This also leaves room to address the costs and economic effects of any unexpected virus resurgence.

The hefty US expansion forecast for this year bodes well for Quebec exports, even in the shadow of potential “Buy American” policies. Alongside the typical demand impacts usually associated with US growth, a shared North American energy system and vehicle supply chain may facilitate eventual resolution of any issues. We also noted throughout negotiations with the Trump administration that the US relies heavily on imports to meet its domestic needs for aluminum—a key export for Quebec. Broadly, prospects for aerospace are limited so long as travel restrictions remain in place.

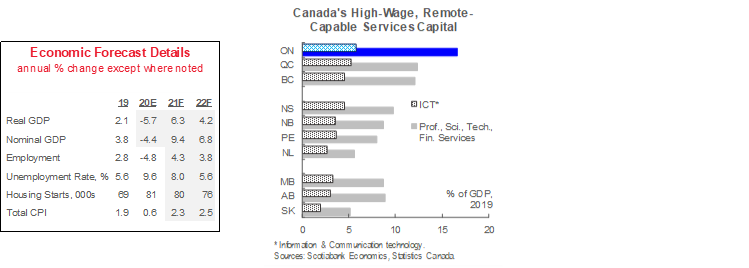

ONTARIO

AUTOS, REMOTE-CAPABLE SERVICES SET UP STRONG GROWTH

Ontario’s contraction paced the national mean last year, despite pandemic lockdowns that lasted longer than in much of the rest of Canada.

Our base case forecast assumes growth above 6% this year, with support from remote work capacity and an export rebound.

Persistently slow population growth represents an important downside risk.

Ontario grappled with longer and stricter COVID-19 restrictions that disproportionately impacted the key auto manufacturing sector, but suffered a dip in output only slightly worse than the national average. Two principal factors explain that result. One is Ontario’s high concentration of industries such as finance, technology, and professional, scientific and technical services (chart). More able to adapt to remote work arrangements and deemed essential in some cases, these sectors were resilient to lockdowns and have largely resumed their upward pre-pandemic trajectories. Another, related, driver was the strong housing market, which benefited from resilient high-wage employment, policy support, and apparent pandemic-time desire for more space outside of the largest population centres.

We are optimistic about the province’s growth prospects this year, assuming more progress on virus containment. Its high-wage services presence could again mitigate the impacts of second wave lockdowns. Even flat automobile output this year would remove the considerable drag related to last year’s 16% plunge, which weighed heavily on Ontario exports. Metals—Ontario’s second-most important export by value—should benefit from the strength expected for gold, silver, and base metals prices this year. Broadly, the recovery in the US industrial sector can reasonably be expected to bolster manufacturing activity, even in the event that “Buy American” policies are widely adopted. Residential investment remains supported by low borrowing costs and tight supply-demand balances.

The prospect of slowing population growth is especially pertinent to Ontario’s outlook. The province had seen some of its strongest headcount gains in two decades before the pandemic. Lockdowns and border restrictions have since resulted in plunging immigrant and admissions, to the point that Ontario’s population declined on a quarter-over-quarter basis late last year. In-migration from other Canadian jurisdictions—another source of pre-pandemic headcount gains—also fell off considerably towards the end of 2020, and international student arrivals remain well below 2019 levels. We are cautiously optimistic that widespread vaccination, higher national immigration targets, and the province’s status as a desirable destination for workers will eventually lead to a recovery, but there is clearly uncertainty on this front.

Ontario’s 2020 Budget—released late last year—assumes sizeable deficits and a rising debt load throughout the next three years. However, the plan built in conservative economic forecasts and large contingency reserves that present upside for budget balances and may help ease the pace of post-pandemic consolidation. Key policy supports to boost long-run growth include energy cost reductions, support for transit, and broadband infrastructure investments.

MANITOBA

STEEP SECOND WAVE LOCKDOWNS ERODE EARLY 2020 SUCCESS

A steep second pandemic wave provides a soft handoff for Manitoba in 2021.

Virus control and a diversified economy blunted pandemic impacts last year.

Agriculture and food manufacturing are key sources of strength.

Manitoba’s successful taming of the first wave of COVID-19 in 2020 contributed to one of the smallest economic contractions of any province. Full-time jobs and hours in nearly every large industry in Manitoba performed better than they did at the national level in 2020, particularly in the summer and early fall months. Early reopening supported better-than-average residential and non-residential building outlays in the third quarter. Meanwhile, with strong price growth, decent output increases for key crops such as wheat, soybeans, oats, and canola also lifted agricultural merchandise export advances, while demand for processed foods was firm during lockdowns. Generally, Manitoba’s economy is not especially exposed to any one industry (chart), which helped blunt last year’s downturn and sets up steady growth going forward.

The second wave was more severe, and led to more restrictive containment measures than during the first wave. Many indicators suggest a sharper late-2020 slowdown than in much of the rest of the country. Manitoba was the only province to shed full-time jobs in both November and December 2020—losses were tilted towards accommodation and food services. Housing and business investment also performed worse than the Canadian mean in Q4-2020. The good news is that infection rates and some restrictions have since eased. Hiring bounced back in January 2021, with gains reported across industries. Looking forward, in a rising metals price environment, investment intentions in Manitoba’s mining industry are up over 30% versus 2020.

Agricultural prospects will continue to be impacted by Chinese actions. The Middle Kingdom significantly increased its purchases of Canadian agricultural products last year, though they remain below the heights of 2017–18 when soybean imports surged. Chinese demand is also supporting agricultural prices.

Prospects are mixed for transportation equipment. The strong economic rebound expected south of the border could reasonably be expected to drive a recovery in related shipments. For aerospace, the outlook depends fundamentally on the extent to which air travel returns from the pandemic-induced lockdown. More positively, electric bus manufacturing—a niche industry in Manitoba—may benefit from the shift towards decarbonization, especially Ottawa’s efforts to electrify mass transit.

Fiscal policy remains supportive. On a per-capita basis, Manitoba had offered the third-largest package of COVID-19 support measures as of late last year. Federal transfers will also help reduce the size of its FY21 deficit by roughly $900 mn versus the projections released in September 2020. Eventual balance will likely involve spending control—mean annual gains of just 1.4% were built into a pre-pandemic FY21–24 plan to return to black ink by the latter year. For now, we support and anticipate continued efforts to tackle the pandemic and bolster the economic recovery.

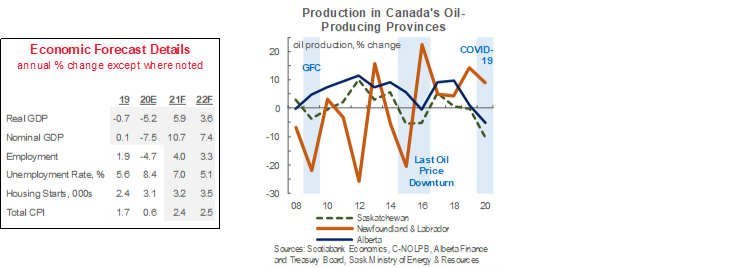

SASKATCHEWAN

MOMENTUM STALLS AFTER CHALLENGING SECOND WAVE

Though Saskatchewan’s economy took a hit from energy sector weakness last year, agriculture and other mining helped prevent a deeper contraction.

Momentum stalled late last year, but improving commodity prices and production should help reverse course.

A low debt burden remains despite the pandemic hit to budget balances.

The blow to Saskatchewan’s oil and gas sector was significant last year. Crude production fell by more than 10%—almost twice the plunge witnessed in any single year during the last oil price downturn (chart)—and led to steep a drop in full-time mining and oil & gas extraction employment. That, in turn, translated into weakness in servicing industries such as manufacturing and construction, as experienced in past downturns. The surge in second wave infections—after successful control in the first round—was also an unfortunate development. Recent oil price gains should eventually support a recovery in oil production and job creation in natural resources and adjacent sectors, but the latest intentions survey suggests muted prospects for capital outlays this year.

The good news is that other commodities have helped to mitigate oil and gas weakness. Potash production rose 8% last year and is expected to enjoy further price and output increases this year. The latest Scotiabank metals price forecast update assumed that uranium production would restart and ramp up at the Cigar Lake mine in the coming years.

For agriculture, hefty Chinese purchase volumes remain the dominant trend. This has persisted since the autumn of 2020, to the extent that it has raised fears of shortages, and boosted prices for staple crops wheat, canola, and lentils to multi-year highs. The African swine fever’s impact on the domestic herd has also necessitated greater meat imports by the Middle Kingdom. Whether the pace of recent gains continues to support nominal export values and farm incomes in the face of Sino-Canadian diplomatic tensions is the key question. Gains stalled somewhat to close out 2020, which looks to be translating into agricultural employment weakness.

Early signs in the leadup to the April 6, 2021 budget are that a return to balance may be delayed beyond FY25 as previously planned; Saskatchewan still maintains a modest debt burden. Citing a still-fragile recovery from the pandemic, the government has indicated that it may not embark on the outer-year spending reductions that had been a key plank of the blueprint released in August 2020. Promises outlined in last year’s election campaign—including electricity rate cuts across the spectrum of users, small business tax reductions, and funding for more health care sector hiring—will likely also be factored into the coming fiscal plan. In any case, the Province will likely maintain a net debt-to-GDP ratio in the 20–25% range in the coming years, having managed to reduce program spending from FY16 to FY20.

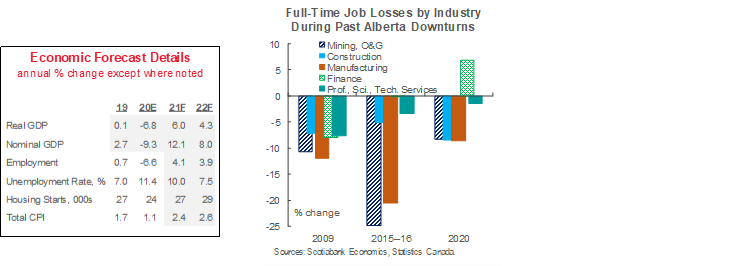

ALBERTA

LIFTED BY OIL PRICE GAINS

Alberta experienced the deepest recession of any province last year as it dealt with the effects of COVID-19 and a plunge in oil and gas activity.

Rising crude values to begin this year bode well for a solid rebound in 2021, but the pandemic extends recovery from the last downturn to eight years.

For non-energy industries, petrochemicals and forestry face the best near-term prospects, but full economic diversification remains a long-run goal.

Alberta was harder-hit than any other provincial economy in 2020, a result of its oil and gas industry intensity. It witnessed the steepest drop in wages and salaries last year, the second-largest reductions in hours worked and active businesses, and as of January, its full-time workforce was further from its February 2020 peak than any other jurisdiction. Crude production fell by 5%—more than in 2016 at the height of the last commodity price correction—and drilling activity at one point reached an all-time low, driving a 38% decline in oil and gas investment at the national level in 2020.

As in prior economic downturns, the oil and gas downturn extended to adjacent industries (chart). Full-time employment declines in construction, manufacturing, and professional, scientific, and technical services reflect the role played by energy in generating business for firms in those sectors. Commercial building outlays continue to be held back by the supply overhang accrued since the last oil price downturn.

The surge in crude values to begin 2021—which prompted an upward revision to our price forecast—bodes well for a recovery this year. Crude output rose above year-earlier levels in November and December 2020, and should see further increases following the end of curtailment. With improving fuel demand, egress capacity will likely once again become a factor—we expect the eventual completion of the Line 3 and TransMountain Extension conduits to assist in this respect. Still, investment will likely stay below pre-pandemic levels for at least a few years; the pace and direction of an eventual Biden climate agenda poses additional risk. All told, we do not expect the province to reach the peak GDP it hit before the last oil price downturn until 2022.

Outside oil and gas, petrochemicals and forestry have strong prospects. Chemical manufacturing investment intentions are nearly 25% higher than preliminary estimates for last year, supported by work at the Heartland Petrochemical Complex. Forest product exports should benefit from strong lumber prices and housing market activity. The agricultural outlook is more mixed. Beef production will likely rise this year given early 2020 COVID-19 plant shutdowns. Wheat output could reasonably be expected to ease after stronger-than-average yields in 2020, though prices remain elevated alongside those of oilseeds. Stepped-up FY22 capital outlays concentrated in municipal infrastructure will likely lend further support to the province’s expansion. A number of renewable projects dot the economic landscape.

Budget 2021 announced several new economic diversification initiatives. These include: attraction and development of skilled workers in the technology industry, plans to boost agricultural investment, and efforts to reduce FinTech regulatory burdens. These efforts could help guard against future downturns, but will take time to bear fruit.

BRITISH COLUMBIA

POSITIONED FOR STRONG RECOVERY DESPITE TOURISM

BC’s economy was a mixed bag last year but carries momentum into 2021; we expect it to continue to modestly outperform the Canadian average.

Major projects, the tech sector, and a light virus caseload are advantages.

Key questions surround tourism-oriented sectors.

We noted the outsized tourism industry share of BC’s economy in our last Provincial Outlook; related challenges will likely hold back the province’s rebound. Firms in the sector—and in adjacent ones such as accommodation and food services, retail, and recreation—are unlikely to be able to operate at full capacity while COVID-19 remains a threat and physical gathering restrictions stay in place.

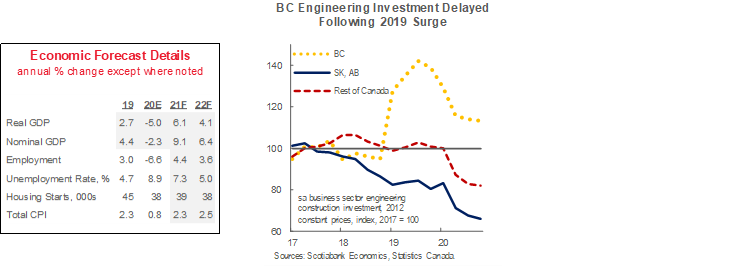

The liquefied natural gas (LNG) industry also held BC back last year, but we expect its fortunes to improve. Ramp-up of several ventures—including the LNG Canada Coastal Gaslink Export Pipeline megaproject in Kitimat—powered torrid engineering structures investment gains in 2019. Virus-related delays prompted a sharp early-2020 drop in related construction capital outlays (chart) and employment. We anticipate that the venture will eventually reach peak activity in the coming years as planned.

Though delayed and subject to new cost pressures according to the latest reporting, work on the Site C hydroelectric dam will continue, and that bodes well for related employment and capital investment. Geotechnical issues reported in H2-2020 raised fresh concerns about the project’s viability.

BC’s natural resources-oriented export profile looks poised for solid gains. Hefty US home construction—notably in lumber-intensive single-family units—should help BC lumber exports. This has already contributed to record high lumber prices. We also anticipate that prices and demand for copper, coal, and natural gas—key commodities in BC—will remain well-supported in 2021–22 amid a stimulus-led global recovery.

The technology sector is another advantage. BC’s tech industry output growth outpaced all other provinces in the pre-pandemic decade; the Province’s own data show favourable job creation relative to US tech hubs over the same period. The sector is broadly less vulnerable to any impending shift to remote work, and offers high wages in a jurisdiction where average weekly earnings lag the national average. Remote work’s ultimate impact on industrial and commercial buildings is still unclear: rents and investment have rebounded somewhat after weakness in summer 2020.

The Vancouver, Victoria, Abbotsford, and Kelowna housing markets begin 2021 with sales and price momentum and tight demand-supply conditions. This has the potential to encourage homebuilding and price appreciation, though immigration remains a wild card: admissions to BC were still down 30% y/y as of December 2020.

Though BC’s fiscal balances have taken a significant hit amid the pandemic, the province’s net debt-to-GDP ratio in the 20–25% range is among the lowest in Canada. That leaves room for further fiscal support should the need arise.

APPENDIX—COVID-19 CASELOADS, RESTRICTIONS, AND EMPLOYMENT RECOVERIES

COVID-19 INFECTION CURVES

OXFORD UNIVERSITY INDEX OF LOCKDOWN STRINGENCY

FULL-TIME EMPLOYMENT

Data current to March 10 2021. Sources: Scotiabank Economics, Government of Canada, Statistics Canada, Bloomberg, Oxford University.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.