OVERVIEW

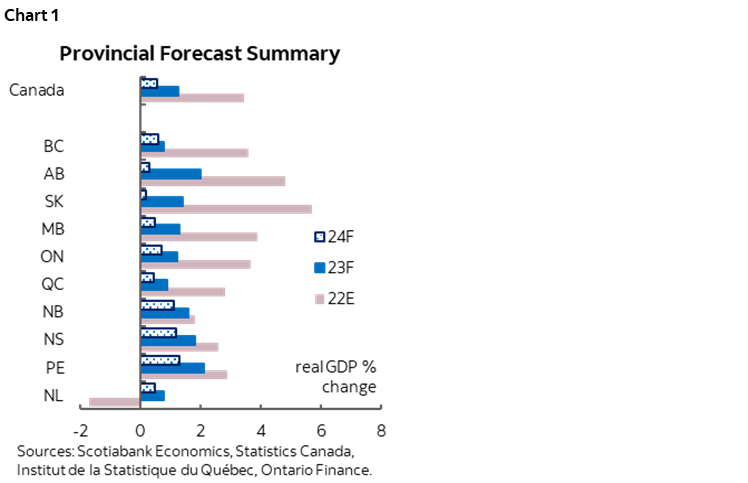

So far this year, provinces have displayed varying degrees of resilience in the face of higher interest rates with some faring better than others (chart 1). As expected, the Maritime provinces have remained largely insulated from the downturn thanks to their comparatively low household indebtedness and continued population ascent. Meanwhile, weakness in oil prices may have undermined the anticipated advantages for provinces reliant on commodity production. Economic growth in BC should continue trailing behind its peers, weighed down by the rapid slowdown in consumption compounded by further tightening in the policy rate, though a premature recovery in housing activity could soon cease to be a drag on growth.

CONSUMPTION: MARITIME PROVINCES THRIVE, BC STRUGGLES

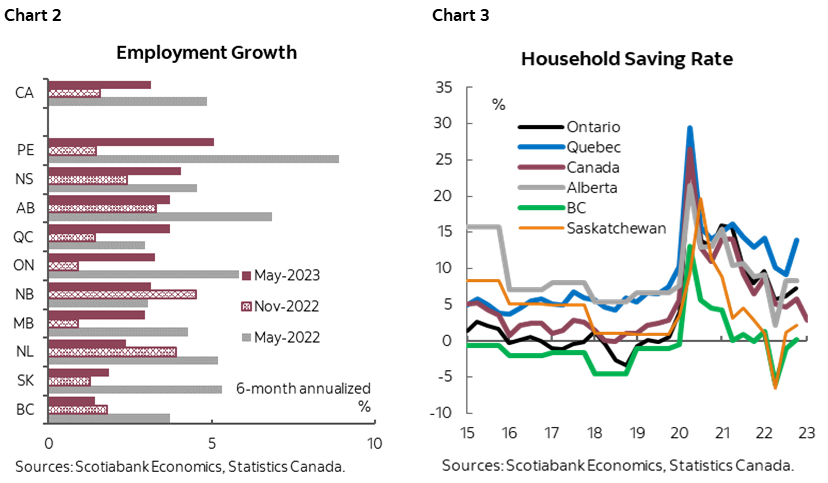

Despite the lack of material signs of a slowdown thus far, consumption is anticipated to gradually taper off as tailwinds in some provinces dissipate. Household consumption regained momentum in Q1 in both goods and services—following a lackluster performance in the previous quarter—supported by a buoyant labour market. Hiring slowed in the second half of last year but has rebounded across the board this year despite aggressive rate hikes (chart 2). The Maritime provinces and Alberta have seen the strongest employment gain relative to last year. BC and Saskatchewan have witnessed a significant deceleration in hiring, combined with low saving rates in these two provinces (chart 3), could lead to a sharper slowdown in consumption as labour markets continue to cool.

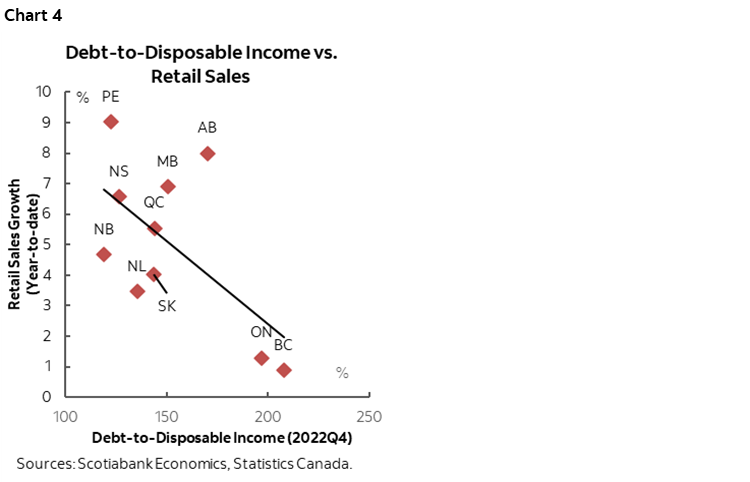

Continued monetary tightening should further dampen demand for goods and services and eventually lead to a deceleration in growth. Robust consumer spending poses challenges for the Bank of Canada in its fight against inflation. Core inflation remains sticky, reinforcing the need for further rate tightening ahead to reign in spending in order to bring inflation back to target. As intended, higher interest rates curbs demand in rate-sensitive sectors while simultaneously raising the costs of debt servicing, thereby impeding consumption effectively. Compared to same quarter last year, retail sales growth slowed the most in Ontario and BC where household debt-to-income well exceeded that of other provinces (chart 4).

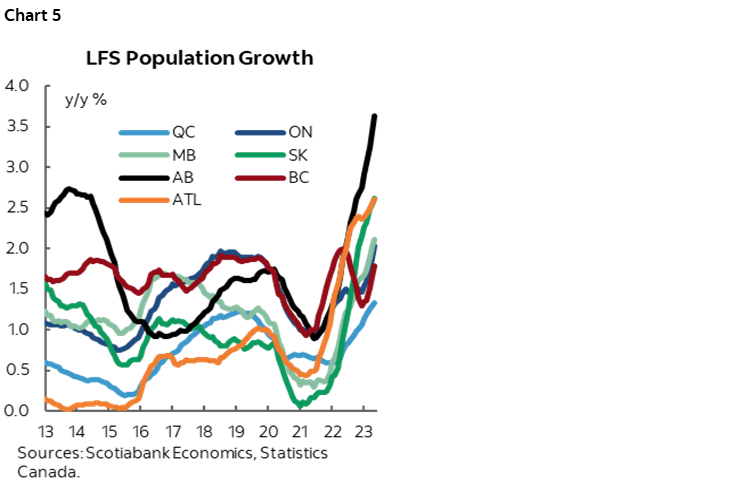

Population growth from both international and interprovincial migration has been particularly strong in the Maritime provinces and Alberta (chart 5). The influx of international migrants, over half of which are non-permanent residents, has led to the population boom this year, pushing the Canadian population to 40 mn as of June 2023. This surge in population has bolstered consumer spending and stimulated growth in an environment of high interest rates. Additionally, immigrants helped fill job vacancies and alleviate some of the labour market tightness, although growth in labour force still struggles to keep up with labour demand.

Overall, household spending plays a pivotal role in driving real growth with a disproportionate impact on the Maritime provinces and BC. Resilient consumption provides a boost to economic growth in the Maritime provinces. On the other hand, weaknesses in consumption, coupled with sluggish housing-related activity, have posed a pronounced slowing effect on BC’s economy this year.

BUSINESS INVESTMENT: SLOWING ACROSS THE BOARD, YET STILL BURGEONING IN SASKATCHEWAN AND QUEBEC

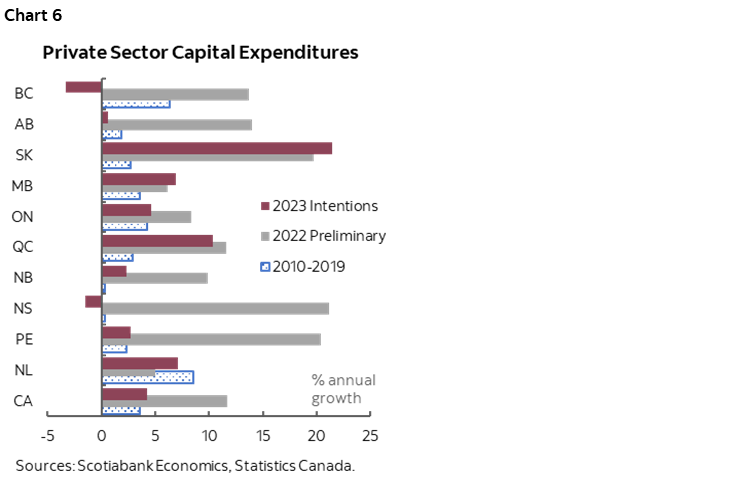

Declining capital investments, particularly in machinery and equipment, have been a drag on growth in some provinces despite a slight reprieve in Q1. In Alberta, investment intentions for 2023 appear weak outside of the oil and gas industry (chart 6). Both BC and Nova Scotia expect some drag on growth from lower capital expenditures. Saskatchewan has stood out as the outlier with significant investments planned in its key sectors such as mining, oil and gas, and manufacturing which should bolster its economic growth this year. Quebec, Newfoundland and Labrador, and Manitoba should also benefit to varying degrees from robust capital expenditures.

EXPORTS: LOSING MOMENTUM IN BC, REMAINING A TAILWIND IN ONTARIO… FOR NOW

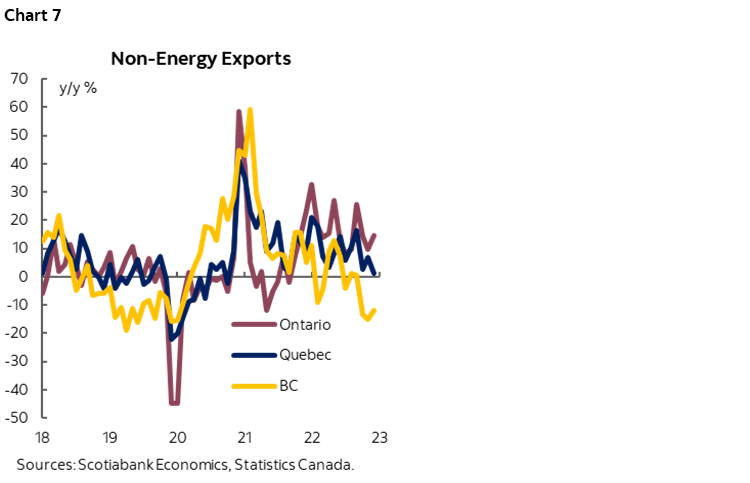

Exports have been more resilient than previously anticipated, with non-energy exports supporting growth so far this year. A delayed recession in the US, along with the softness in CAD against USD, supports demand for Canadian goods and services—before the expected shift in tides in the latter half of the year. Solid manufacturing shipments persist in Ontario, PEI, and Manitoba, while a slowdown in exports has materialized in BC, primarily driven by declining demand for forestry products (chart 7). While the recovery in the auto sector provides a tailwind to Ontario’s exports this year with motor vehicle and parts exports returning to pre-pandemic levels in value terms, the impressive growth in the province’s exports extends beyond the automotive industry. Anticipate further headwinds as the pace of auto recovery remains slow and bumpy, accompanied by uncertainties such as rising financing costs and declining vehicle affordability.

Continued weakness in commodity prices could cast some shadow on the otherwise promising growth outlooks of Alberta and Saskatchewan, eroding some anticipated advantages over their peers. The two provinces heavily rely on exports that constitute over 60% of their real GDP. Value of energy exports tapered off from last summer’s highs as oil prices ease over -35% from the peak, with WTI fluctuating around US$70/bbl in May and June. WTI could average around US$78/bbl this year although with a wide range of variability—the OPEC+ production cut puts a floor under weakening demand, though uncertainty around potential Chinese stimulus could counter this effect. Anticipated momentum in energy prices supports continued strong activity in the oil and gas sector. Alberta Energy Regulator anticipates 8% increase in oil and gas capital spending this year, following last year’s 56% gain. Crude output remains in line with last year’s elevated levels in Alberta and edged up further by 2.5% year-over-year in Saskatchewan in Q1.

HOUSING: PREMATURE RECOVERY PICKING UP SPEED IN ONTARIO AND BC REFLECTING STRUCTURAL SHORTFALLS

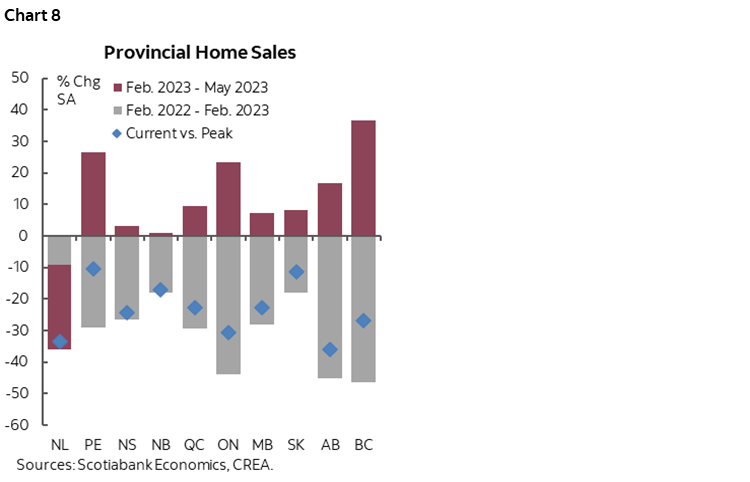

Housing markets recovered earlier than anticipated albeit from weak levels, reversing some lost ground experienced throughout the majority of last year, particularly in Ontario and BC. National resale activity started the year at -28% below its peak, and has been picking up since February. Ontario and BC have seen the most significant pickup in sales, yet they still face the largest loss relative to their respective peaks when compared to their peers (chart 8). Although the rapid rebound could potentially be quelled by additional rate hikes combined with further tightening in longer-term borrowing costs, housing activity may soon cease to be a drag on growth as cyclical headwinds give way to robust structural forces. Growth in Ontario and BC could receive a boost from their prominent residential real estate sectors if the current ascent continues.

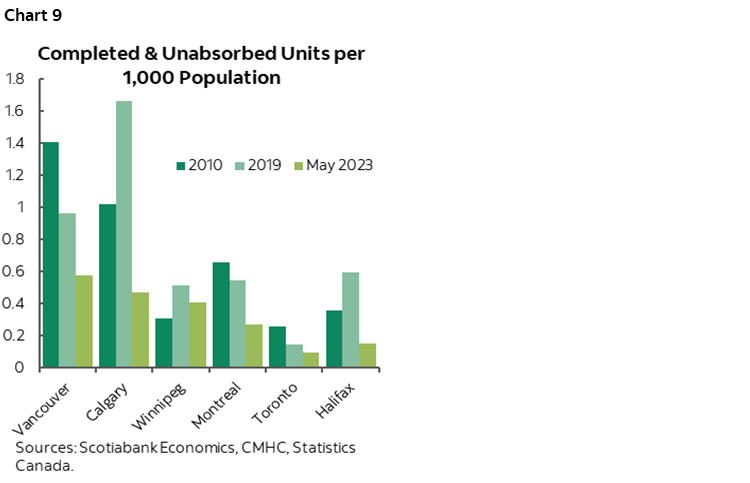

Construction activities remain robust on the back of still favourable structural factors despite housing markets being under stress for the majority of last year. Housing starts held up steady in Ontario and BC but have been declining in the rest of the country, mirroring the trend observed in residential investments. Structural factors support continued growth of investments in the residential sector—the population-adjusted housing stock reached its lowest levels in decades from coast to coast, with the undersupply of housing especially acute in major CMAs in Ontario and Nova Scotia (chart 9).

WEAKER GROWTH ANTICIPATED NEXT YEAR IN ALL PROVINCES

With early momentum in 2023 the much-anticipated technical recession is again pushed out towards the end of the year resulting in weaker expected output next year across the board. Declining exports resulting from a stronger CAD, softer commodity prices and weaker growth prospects in the US could potentially pose a drag on growth next year. As headwinds from consumer demand continue to play out and the economy enters excess supply, the manufacturing sector should also face further challenges. On the other hand, with interest rate cuts starting next year, we could expect some rebound to take hold in residential and business investments.

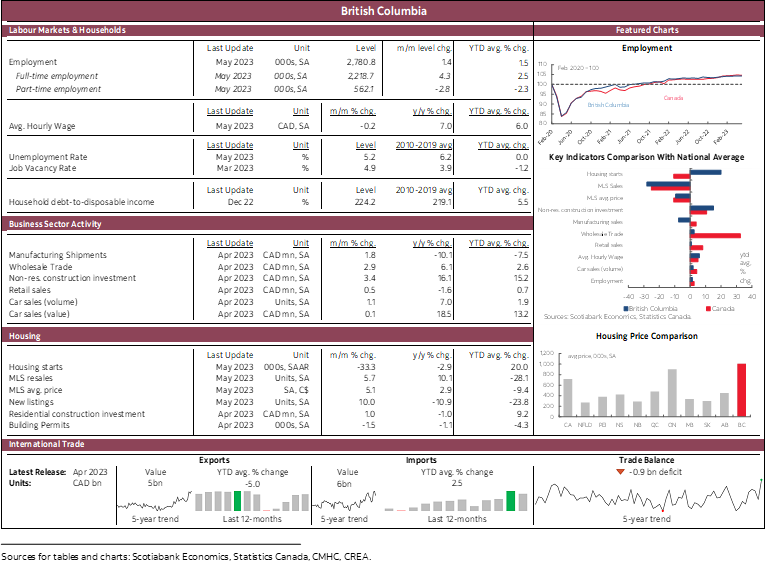

BRITISH COLUMBIA

So far this year, BC’s economy has seen the most cooling among the provinces, reflected in notable deceleration in key indicators such as employment growth and retail sales, both lagging behind the national average. This, combined with the province’s high household debt-to-income ratio, indicate a rapid slowdown in consumer spending, which poses a material drag to the province’s growth this year particularly considering its significant contribution of around 64% to real GDP, surpassing that of other provinces outside of the Maritime provinces. Population growth continues to accelerate this year following the +2.5% gain last year, but with some headwinds—the share of immigrants landing in BC dropped to 10% in Q4 last year, compared to 14% average during the past decade, indicating that BC might be losing some advantage attracting international migrants to provinces such as Alberta and the Maritime provinces.

Natural resource exports took a hit from weak commodity prices. Forestry products exports drove the descent with lumber prices down over -30% from a year ago, compounded by reduced production due to several mill closures. The sector now accounts for only 20% of total exports—a sharp decline from over 50% in the early 2000s. In contrast, energy exports picked up speed and should continue to expand with the completion of major LNG projects in the medium-term.

BC’s growth this year might benefit from a premature recovery in housing activity. Sales rebounded sharply in BC after plunging by -46% from peak to trough, with sales rate returning to 2019 levels in May. Meanwhile, despite the housing sector being under stress due to rising interest rates, residential investment and construction activity persist at high levels, supported by public funding via the government’s refreshed 30-point Plan for Housing Affordability. Non-residential investment has maintained steady growth in real term, fueled by booming construction activities for major projects such as LNG Canada and Site C dam, surpassing the pace seen in the rest of the country.

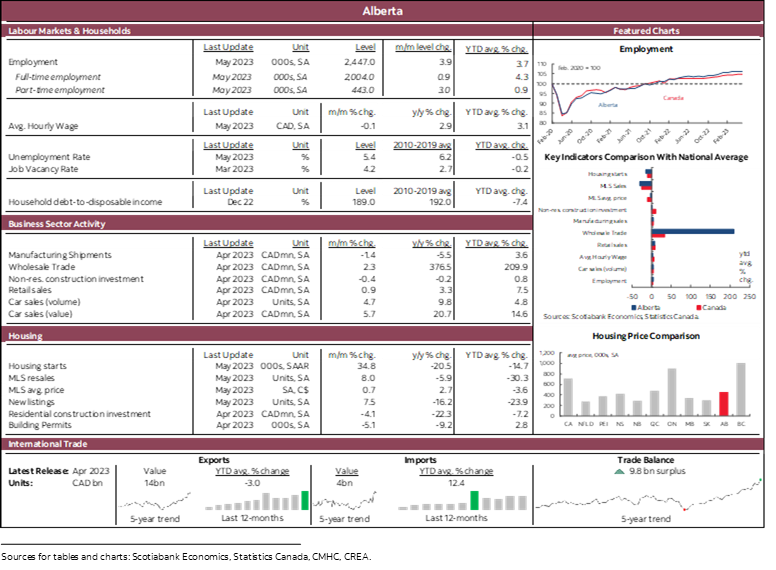

ALBERTA

Similar to the rest of the country, Alberta is not spared an anticipated economic slowdown this year and next, but the strong economic indicators so far this year suggest the wild rose country may continue to lead growth this year. The province boasts higher employment gains than other parts of the country, primarily driven by the construction sector, along with the continued momentum from the “‘Alberta is Calling’ campaign that significantly lifted employment in professional, scientific and technical services last year. The province’s population grew by a robust 3% last year, and the pace continues to accelerate, surpassing most maritime provinces and could reach 4% y/y by the end of 2023. Strong population growth and a buoyant labour market support consumption amidst high interest rates and elevation price inflation.

The oil and gas industry is well positioned to have another year of strong activity while recent volatility in commodity prices could erode some gains. Energy exports dropped by -12.5% (sa) since the beginning of this year due to falling oil prices, influenced by weakening demand from a sluggish Chinese recovery, and have remained volatile, fluctuating around US$70/bbl since May. The WTI-WCS spread narrowed by half from close to US$30/bbl late last year, supporting profitability of Albertan producers. Production and investment remained strong in the sector—Alberta’s Budget 2023 expects investment in oil sands to grow by 17% in 2023. Drilling activity reached record highs prior to the outbreak of wildfires in March, which led to temporary production halt in certain rigs; however, the overall production level remained largely unaffected.

High borrowing costs and elevated construction prices should weigh on private non-energy investment, which has been lagging the rest of the country in real term so far this year, and is expected to moderate this year by -4.7% after two years of strong growth. On a positive note, continued expansion of emerging industries such as clean tech and aviation provides opportunities for sustained growth in the province.

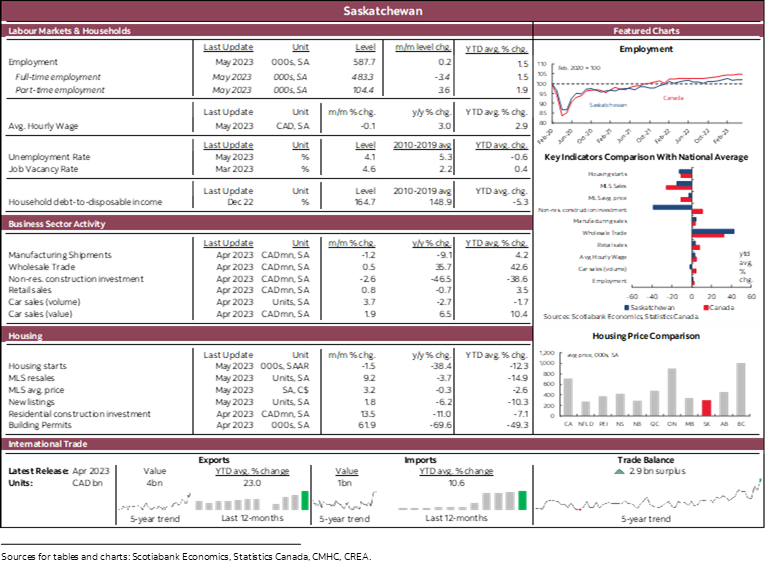

SASKATCHEWAN

Major capital investments and a booming commodity sector set the stage for another year of robust growth in Saskatchewan. The province expects capital investment to grow by another +21.5% in 2023—the highest among the provinces—with major spending boosts in mining (+61%), oil and gas (+16.3%), as well as the manufacturing sector (+32%). Despite prices coming down from their highs last year following Russia’s invasion of Ukraine, production in the mining sector persisted at high levels, particularly in uranium production which grew by close to 80% year-to-date. Potash and salt production both saw a light decrease of around -10% during the same period. Substantial investments have been made in the construction of the Jansen potash project's two mine shafts, which are expected to commence production in 2026, contributing to the province’s growth and employment. Oil production increased by +2.5% y/y in the first quarter, reflecting strong activity in the sector although recent weakness in crude prices could erode some growth upside this year and next.

Some parts of the economy have inevitably slowed. Employment growth decelerated quickly in 2023 with an annualized rate of 1.3% gain in the first five months of the year—well below the national average of 2.8%. Retail sales contracted even in nominal terms since the beginning of the year, while the rest of the country saw relatively flat retail sales over the same period. The province witnessed robust population growth of 1.9% last year with the influx of international migrants offsetting losses from interprovincial migration. So far this year, Saskatchewan saw the largest population gain outside of the Maritime provinces and Alberta, providing a buffer to household consumption.

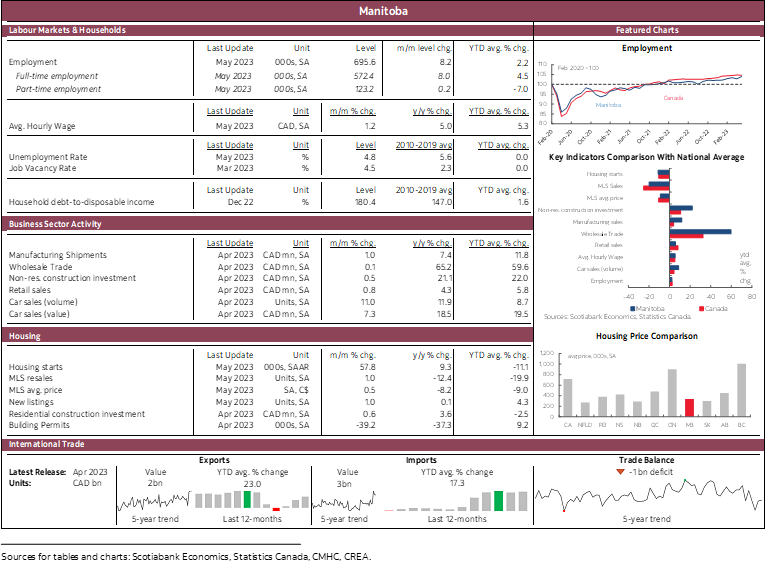

MANITOBA

Manitoba’s economy exhibited remarkable resilience against rate hikes and is expected to maintain a performance that aligns closely with the national average this year. Employment rose by +1.9% in the first five months of this year, well above the national average of +1.2% and among the highest growth across the country. Retail sales grew by +5.8% year-to-date in nominal term, reflecting robust consumer spending in the province. Manitoba gained +1.9% population last year with international migration offsetting the -0.5% loss due to interprovincial migration. Population growth continues to accelerate and could reach +2.5% y/y by the end of this year.

The province’s agriculture sector lost some steam this year from last year’s strong recovery but remained steady. Production levels for key crops such as wheat, oats and canola remained well above historical averages, while barley production notably declined. Global demand for Manitoba’s key agricultural products should fall this year, and prices have generally faced downward pressure from ample supply, yet still at favourable levels. Solid domestic demand should provide a buffer since half of Manitoba’s exports are towards other jurisdictions in Canada. Electricity exports in particular, which are sent to the US, Saskatchewan and Ontario, should give growth a boost as electricity generation remains above the historical average.

ONTARIO

Ontario led the deceleration in economic growth during the second half of last year and recorded a -0.8% annualized q/q retrenchment in real GDP in Q4, while the rest of the country collectively grew by 0.3% over the same period. While real GDP growth should continue to fall this year, the resilience observed in its labour market and exports so far this year suggests that Ontario’s economic growth still has some steam left. Employment in Ontario has shown strong momentum in the first five months of this year, outpacing the national average with an annualized rate of 3% —well above its long-term average annual growth rate of 1.4%. Exports grew by 14.6% year-to-date, primarily by strength beyond automotive, while the auto sector itself is undergoing a bumpy recovery. The province added 360k (+2.4%) population last year from surging international immigration, and over 60% were non-permanent residents. Population growth continued to accelerate this year, and if the trend persists, the province is poised to record even stronger population growth this year. The ongoing population surge, along with other factors, might provided a boost to Ontario’s housing market, as the province witnessed consecutive increases in resale activity, with the level of sales reaching 23% higher than the trough. These are all signs that Ontario has likely enjoyed a stellar start to the year, with the economy humming along as the policy rate approaches its cyclical peak.

As the anticipated curtailment in consumption and declining demand in exports continue to play out, the province’s growth prospects are projected to deteriorate rapidly, with real growth likely slowing to around 0.7% in the coming year.

The anticipated recovery in auto sales is expected to provide a boost to Ontario’s manufacturing industry, but the pace remains slow and accompanied by plenty of uncertainties, including rising financing costs and deteriorating vehicle affordability. With current sales rate still well below pre-pandemic levels in both Canada and the US, the bumpy recovery of auto sales could limit some of the growth upside for Ontario this year and next. On a brighter note, the province boasts significant capital spending and infrastructure investment, which helps offset some of the weaknesses this year.

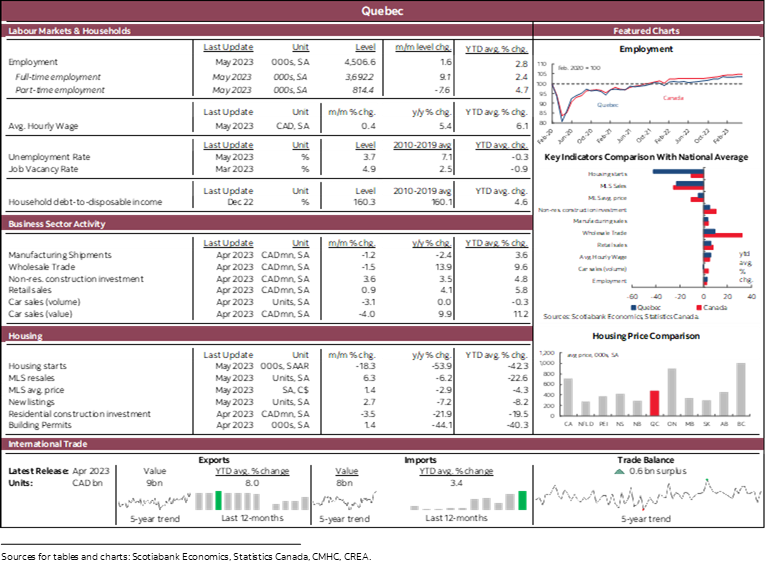

QUEBEC

Quebec’s economy continued to expand in the first quarter on the back of a strong service sector, but real growth struggles to keep pace with its peers. We expect real growth to slide to 0.9% in 2023 with a even softer growth projection of around 0.5% in 2024—both forecasts fall below the national average. The risk of a recession looms closer for Quebec relative to its peers.

Like the rest of the country, the province’s labour market remains resilient, combined with high savings rate, supported consumer spending thus far, but a deceleration is inevitable and necessary to bring inflation down to its target. Employment growth in Quebec is already cooling at a faster pace than the national average. In addition, population growth is not as strong as in other parts of the country despite the influx of non-permanent residents. The government plans to welcome up to 52.5k new permanent residents in 2023, along with robust increases in non-permanent residents, the province’s population growth is projected to continue at a steady pace of around +1.4%. The province is also grappling with a drag from the residential sector, with notable slowdowns recorded in residential investment and housing starts in the first half of this year. There has been an early return of momentum in home sales, reflecting robust fundamentals in the province.

Weaker US demand poses strong headwinds to exports and manufacturing in the province, which is expected to further compound with an anticipated US recession in the latter half of the year and the strengthening of the Canadian dollar. With the economy moving into the state of excess supply, a softening manufacturing sector could have greater drag on Quebec’s growth compared to its peers—the manufacturing sector accounts for around 12% of Quebec’s real GDP, the highest among the provinces.

Robust non-residential investments and enhanced government spending provide some support for growth this year. Non-residential investments picked up sharply in 2022 and remained elevated this year. Despite the rollback of most affordability measures this year, low-income households can expected further relief through tax measures. Public investment through the Quebec Infrastructure Plan received another significant boost, offsetting some of the drop in private investments due to tightening credit conditions.

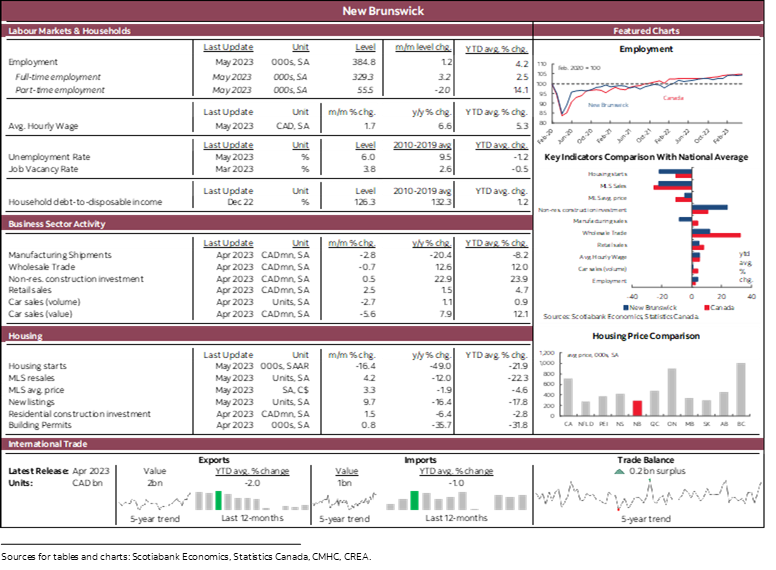

NEW BRUNSWICK

As anticipated, New Brunswick’s economy has been relatively insulated from the interest-rate induced slowdown, especially given the strength in the consumer sector. The province also benefits from a historic population boom driven by immigration (including non-permanent residents), giving near-term growth a boost through consumption and labour market contributions. The province’s population grew by +3.1% last year, with one-third attributed to interprovincial migration and the remaining driven by immigration, and continues to grow at a rapid pace this year, potentially reaching +2.6% y/y by the end of 2023. The province saw the smallest correction in home sales since early last year and has shown durable signs of bottoming in recent months. Average sale price sat only slightly below last year’s peak, compared to the national average that is still -10% below peak. Employment growth accelerated again this year, outpacing the national average, and retail sales maintained a steady pace of growth closely tracks the national average.

Headwinds on exports have been dampening the province’s growth, with weakness observed across key export sectors. Volatile energy exports and soft pulp and paper prices have contributed to the decline, while chemical products have also been losing momentum. New Brunswick’s growth prospects could be further restrained as the province’s main trading partners, namely the US and the EU experience a further slowdowns in the back half of 2023, coupled with a stronger CAD, will likely exacerbate the headwinds facing the province’s exports.

New Brunswick’s strong fiscal position enables the government to increase investment in infrastructure, particularly the improvement and construction of schools and healthcare facilities. Public infrastructure spending is projected to growth by 22% in 2023, which should bolster construction activity in the region.

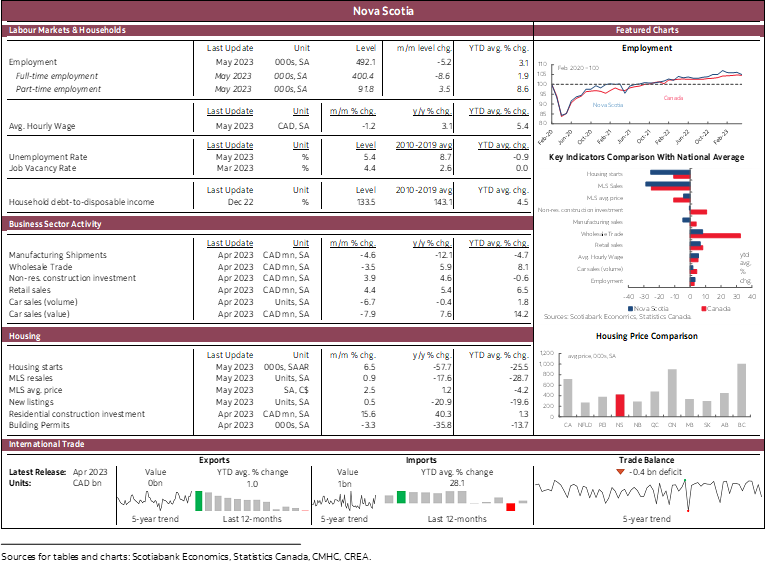

NOVA SCOTIA

Nova Scotia holds some advantages that keep growth above to the national average this year and next. The province benefited from a substantial population surge of 3.3% in 2022, and with continued influxes of immigrants, the province could see a year-over-year population increase of 2.6% by the end of 2023, slightly above the national average. This combined with the province’s low debt-to-disposable income ratio support robust consumer spending thus far. Retail sales have performed strongly year-to-date, with an increase of 6.5% relative to the same period last year, outperforming the national average. Nova Scotia’s tourism industry should return to pre-pandemic norms and strong travel demand, especially from the rest of Canada and the US should provide additional support to the province’s overall economic growth.

A moderate slowdown could be expected later this year, driven by weaker consumption as the result of restrictive interest rates and the broader erosion of purchasing power from high inflation. Employment has been consistently trending lower since the start of this year despite resilience in certain sectors. While housing resale activity remains weak in the region, average sale price has returned to its peak level, which could provide some support for residential investment this year, especially given the need for increased housing supply in Halifax to meet demand from its population expansion.

The government projects deepening deficits over the medium term, driven by substantial spending in healthcare. In addition, the province’s 2023 capital plan sets a new record, with infrastructure spending expected to be 10% higher than last year. These significant public investments, coming at a time of increased demand for public service from surging population, should enhance the province’s growth profile.

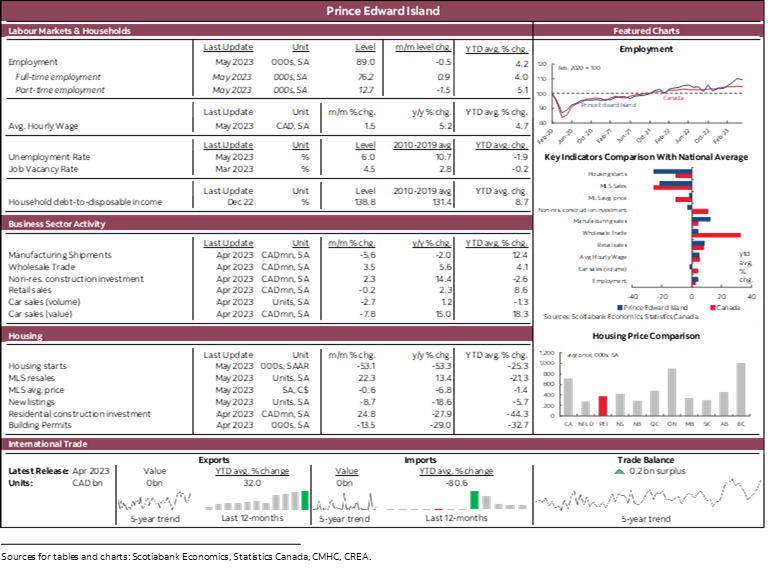

PRINCE EDWARD ISLAND

PEI’s economy is expected to perform strongly this year, albeit with a slight deceleration compared to last year. Exceptionally strong population growth underpins the province’s growth outlook, with its population expanding by 3.8% last year—the highest in the country. PEI could expect even higher population growth this year from continued immigration influx, and aims to reach a milestone of 200k by the early 2030s. PEI’s labour market benefits from this population boom. Employment has been picking up strongly in 2023, up +5.6% since the beginning of the year, well above all other provinces. Despite the influx of migrants contributing to a fast growing labour force, the province continues to have one of the highest job vacancy rates in the country, reflecting strong labour demand in various industries. Robust population growth and tight labour market conditions provide stronger fundamentals to consumer demand compared to other parts of the country. Retail sales have been churning out positive growth this year against strong headwinds, with a year-to-date increase of 8.6% compared to the same period last year, the highest among the provinces. Strong performance has also been observed in the province’s housing market, solidifying the province’s leading position in overall economic growth across the country this year.

Despite a slight loss of momentum compared to last year’s record-high export value, the island’s exports get a lift from the removal of the US potato export ban. Although price for grains have come off their highs in 2022, the overall pricing remains favourable and should support growth in the island’s agricultural sector.

With an optimistic growth outlook, the government has deployed considerable new spending to cater to the island’s growing population. The province’s ambitious FY23 capital plan targets spending above $1 bn for the next five years—38% higher than its last 5-year plan, aiming to improve the province’s climate resiliency, healthcare, housing affordability and education.

NEWFOUNDLAND AND LABRADOR

Following a -1.7% contraction in real GDP in 2022, Newfoundland & Labrador is poised for a slightly stronger real growth this year, backed by major capital investments, while significant headwinds faced by its main industries could lead to another difficult year ahead. Capital investment is expected to ramp up again by +8% in 2023 with major projects in oil and gas (West White Rose and Bay du Nord) and mining (Voisey’s Bay Mine Expansion).

Last year, oil and gas industry contributed negatively to real growth by -2.3% as production declined by over -10%, which means that the real economy grew by +0.6% outside of the oil and gas sector—still weak compared to its peers. Oil production will likely face further setbacks this year with Terra Nova reopening delayed to beyond 2023. Following two robust years in the value of mining exports, the province’s mining sector braces for more headwinds this year from lower iron ore prices and reduced nickel production.

The province saw its population grew by +1.2% in 2022—80% of the population gain came from international migration. Strong inflows of in-migration continue to support robust population growth this year (+1.3% year-to-date as of May).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.