AVOIDING THE WORST

Though not immune to the pandemic or without its own unique challenges, Prince Edward Island has avoided the worst of the first wave.

The province’s small population and island status have helped it keep COVID-19 infections to a minimum and begin reopening earlier than most other jurisdictions; this is perhaps its greatest advantage going forward. To date, there have been no hospitalizations or deaths in PEI, nor have there been signs of a second wave within its borders, though physical distancing and travel restrictions remain in place.

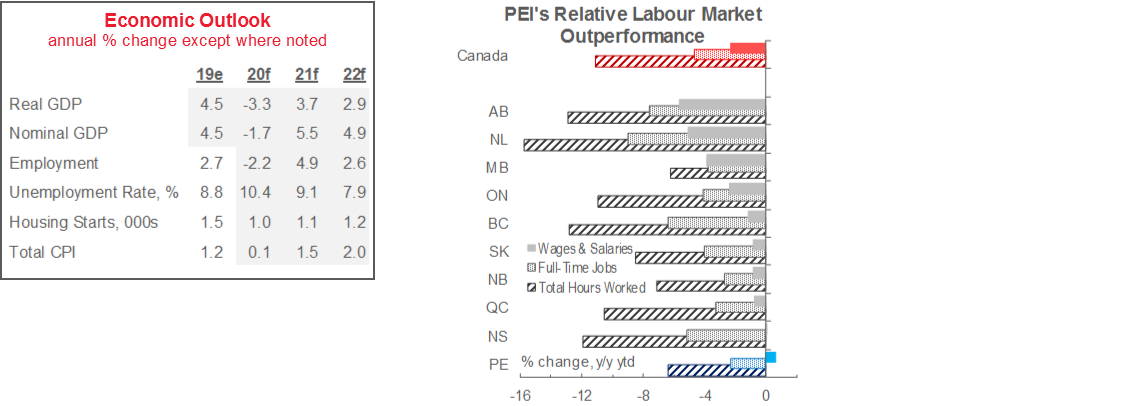

In line with these successes, PEI’s y/y ytd declines in full-time employment and hours worked are among the most muted of any province (chart). Though some of that strength reflects January and February gains, the Island was the only region in which Q2-2020 wages and salaries rose versus the same period in 2019. The retail & wholesale trade sector appears to have benefited from particularly strong activity at food and merchandise stores during lockdowns that may prove transitory. However, resilience in construction and manufacturing also contributed. The former mirrored housing market strength vis-à-vis the release of pent-up pre-pandemic demand. The latter reflects operation of the food manufacturing segment and rise in food prices during lockdowns, which have also lifted sectoral exports.

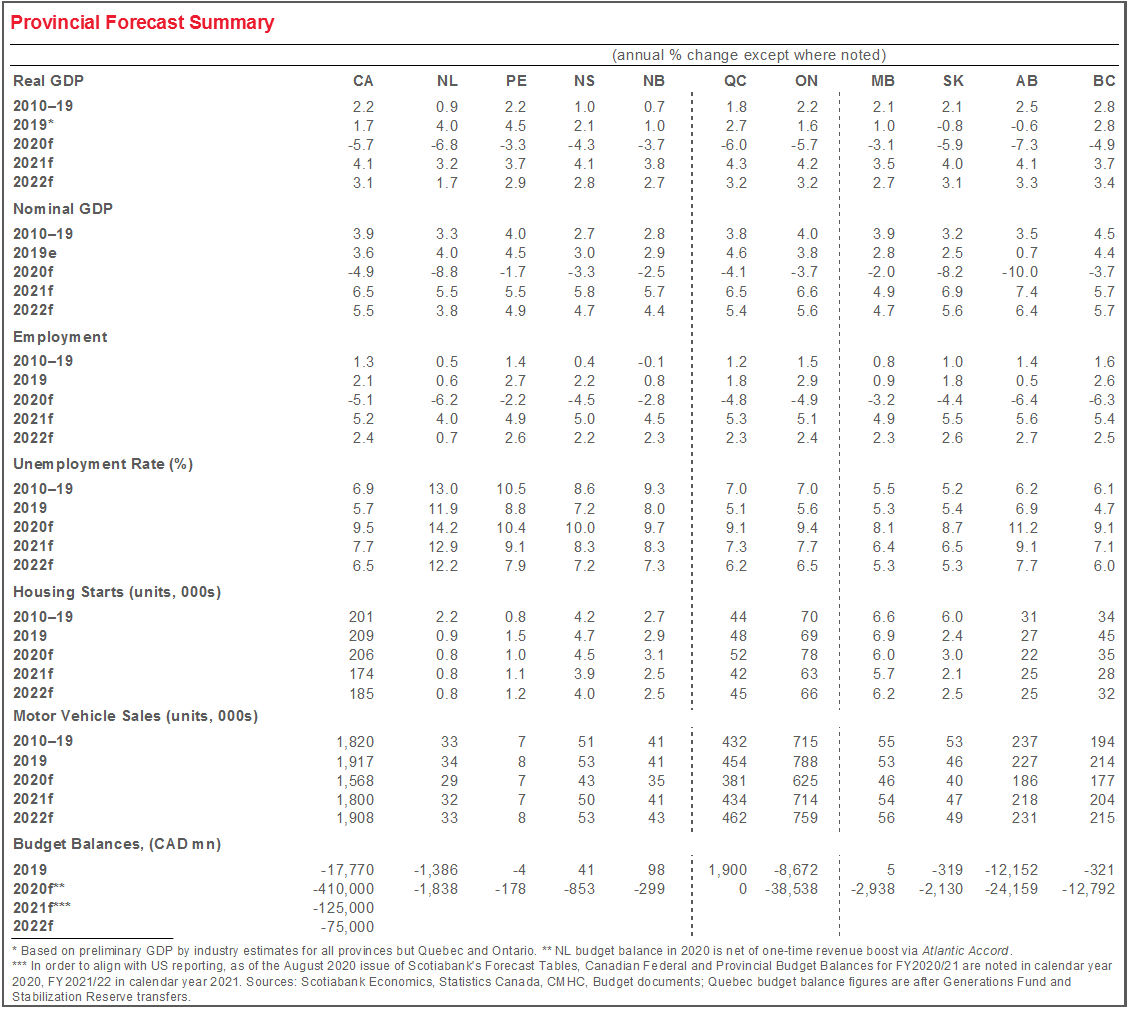

Also expected to cushion the Island economy from COVID-19-related blows in the coming months are ongoing infrastructure plans. Recall that the Province had already increased infrastructure spending plans before the pandemic in order to meet the needs of its rapidly growing population. The November 2019 Capital Plan assumed outlays of $156 mn (more than 2% of 2019 nominal GDP) in FY21, with a further $153 mn pencilled in for the next fiscal year.

The Island’s staple agriculture industry has also held up reasonably well amid the lockdown period, but faces an uncertain outlook. Crop receipts are up more than 20% ytd y/y in H1-2020, anchored by surging prices for staple potatoes. There are concerns that travel restrictions limiting inflows of a needed agricultural workers, summer drought, and early planting decisions reflecting expectations of softer pandemic potato demand will hold back production going forward. However, any resulting market tightness could further support prices in the coming months.

The trajectory of population growth is a key risk for province’s economy. From July 1, 2016 to July 1, 2020, PEI’s headcount advanced by over 10%—its steepest-ever recorded four-year climb and the most of any region in Canada—reflecting hefty immigration levels and, more recently, positive net migration from other provinces. Given these results, safe resumption of migration flows are critical for PEI’s longer-run prospects.

The tourism industry presents another vulnerability. The sector has been hit particularly hard by travel restrictions and limited movement around the globe, and this plays an outsized role in the Island economy. The good news for PEI is that activity has improved because of the Atlantic Bubble: the Province reports that bridge, air, and ferry traffic and overnight stays on the Island have improved since the Bubble opened in July.

Sources for chart and tables: Scotiabank Economics, Statistics Canada, CMHC, PEI Finance.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.