INDUSTRY MIX MAY HOLD BACK EVEN STRONGER RECOVERY

Prince Edward Island’s success in containing COVID-19 sets up strong growth this year, though challenges remain in some key sectors.

Homebuilding, capital outlays in the manufacturing sector, and stepped-up infrastructure spending are expected to bolster the recovery.

PEI has held the lowest per-capita COVID-19 caseload of any Canadian province for much of the last year and has yet to report a COVID-19 death. As such, lockdown measures have generally been among the least restrictive in Canada, and mobility has improved more than in most other regions. This reflects a small population and island status as well as early and decisive policy action.

Yet labour market results were mixed in 2020. PEI’s relatively subdued 3% full-time jobs loss in 2020 largely reflected pre-pandemic momentum that carried into Q1; the jobs recovery since late last summer has been among the softest of any province. Ditto for hours worked, though some improvement in hiring since October looks to have translated into Q4-2020 wage and retail sales gains stronger than the national mean.

Challenges remain in some key sectors. Tourism plays an outsized role in the Island economy; out-of-province visits are way down with travel restrictions in force. Agriculture accounted for 6% of full-time jobs before COVID-19 versus just 2% across Canada and has also held back hiring. The dairy sector—which last year made up 15% of farm cash receipts versus just 10% for Canada—is grappling with pandemic storage issues, while weak potato yields were also reported amid inclement weather. Finally, lockdown-resilient financial and technical services made up just 9% of 2019 full-time jobs versus a 16% national mean.

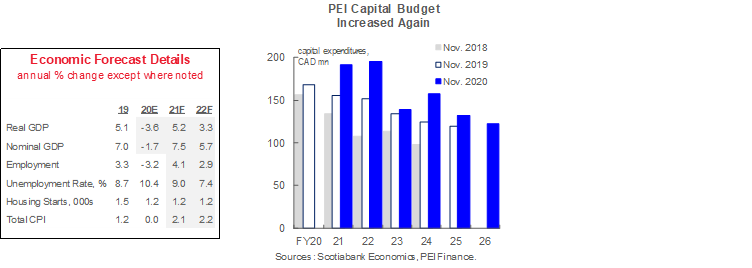

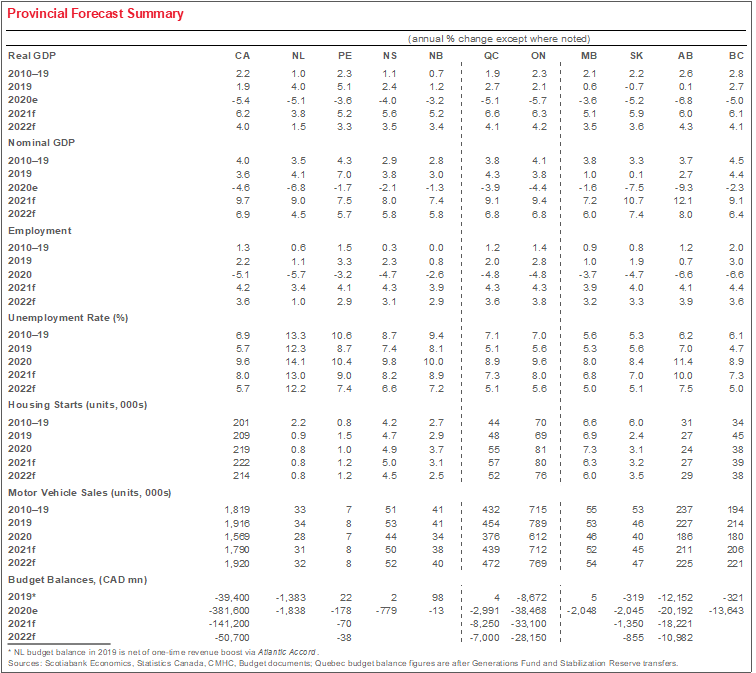

Capital spending trends are more auspicious. With a relatively sound fiscal position—its latest projections included a deficit at just 2% of output and an easing debt-to-GDP ratio—PEI raised its infrastructure budget by $45 mn in FY22 (chart). Alongside housing market tightness, social housing initiatives likely contributed to the expected 2021 capital outlay gains reported in Statistics Canada’s latest intentions survey results. That dataset also implies solid business investment gains this year for aerospace and chemicals manufacturing—two of the Island’s niche products—as well as food processing. Demand for the latter held up well during lockdowns.

The Asia-Pacific region—especially China—held an important role in PEI’s pre-pandemic trade profile. The pace of vaccination and recovery in said region should continue to influence Island trade prospects, alongside any lockdown-related logistical challenges—especially in the seafood industry.

The safe resumption of immigration flows is particularly important. PEI experienced the strongest population growth of any province during 2015–19, and newcomers accounted for three-quarters of those gains—a higher share than in any other province. Downside risk with respect to our baseline forecast therefore has potentially outsized negative consequences for the Island over the longer-run.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.