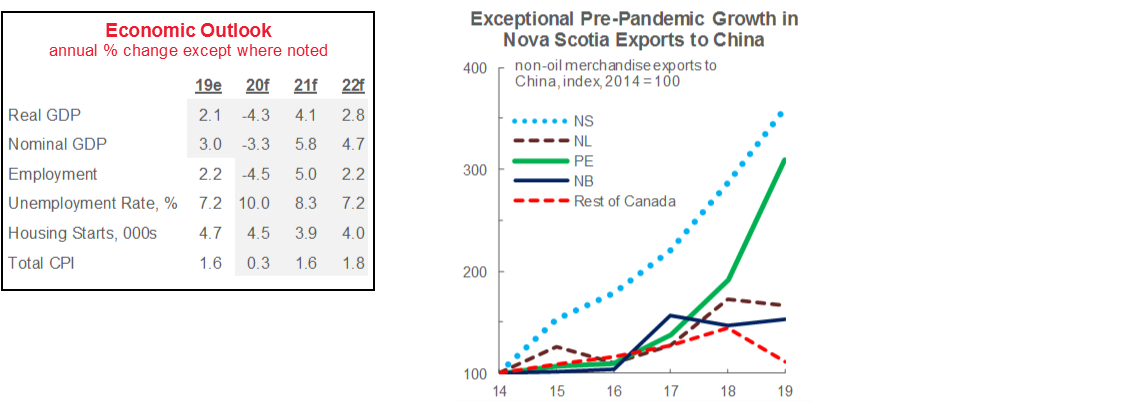

PANDEMIC ADDS TO 2020 TRADE CHALLENGE

A number of unique factors likely mean a more challenging 2020 for Nova Scotia than for its Maritime counterparts, but a relatively solid fiscal position and diversified economy should bolster its eventual recovery.

Despite a clear triumph in containing the first wave of COVID-19—no more than three new daily cases have been reported since May—Nova Scotia’s labour market has not fared as well as other COVID-light regions. This reflects its industrial structure: wholesale and retail trade accounted for more than 15% of full-time jobs last year—more than any other province—and its 16.2% retrenchment is thus far worse than anywhere else. And at almost 6%, accommodation and food services—hammered by lockdown measures—last year made up more of the full-time workforce in Nova Scotia than in any other Canadian jurisdiction. Room bookings have improved somewhat since the inception of the Atlantic Bubble, but remained well below 2019 levels heading into the fall shoulder season.

The global nature of this downturn also neutralizes the diversified trading linkages that could normally be counted on as a cushion. Nova Scotia’s nominal exports to the US, China, and Europe are all down significantly through August. Adding to this challenge are broadly weaker seafood prices during the pandemic and the closure of the Northern Pulp mill in Pictou County prior to the pandemic. In the first eight months of 2020, external shipment values for staple paper manufacturing were more than 50% lower than year-earlier levels. Over the longer-run, the trading relationship with China will be key: Nova Scotia has arguably benefited more from sales to the Middle Kingdom in recent years than any other Canadian province (chart)

As in PEI, potential downside vis-à-vis weaker population growth could be significant in Nova Scotia. Immigration, interprovincial migration, and net non-permanent resident attraction contributed to a nearly 50-year high in population growth in 2019, with labour market outcomes for newcomers generally improving since 2015. Going forward, it will be important for the province to balance safely resuming population flows with the need to prevent pandemic outbreaks.

Expected to offer near-term support for Nova Scotia’s growth outlook is a significant increase to infrastructure spending plans. With an additional boost of almost $250 mn announced in July, provincial capital plan outlays are now projected to climb to about $1.3 bn (2.9% of 2019 nominal GDP)—nearly 90% higher than in FY20. This may help fill the void left by soft private-sector investment, and while it generates fiscal pressures, the Province is on pace to avoid a record debt burden following several strong surpluses and attention to debt management pre-pandemic.

Challenges this year notwithstanding, Halifax remains Atlantic Canada’s high value services sector hub. Within Atlantic Canada, ICT, the financial sector, and professional, scientific, and technical services account for the largest share of output and employment in Nova Scotia. With greater capacity for work to be carried out remotely, these industries—and therefore the province—are likely to be more resilient to an extended lockdown situation.

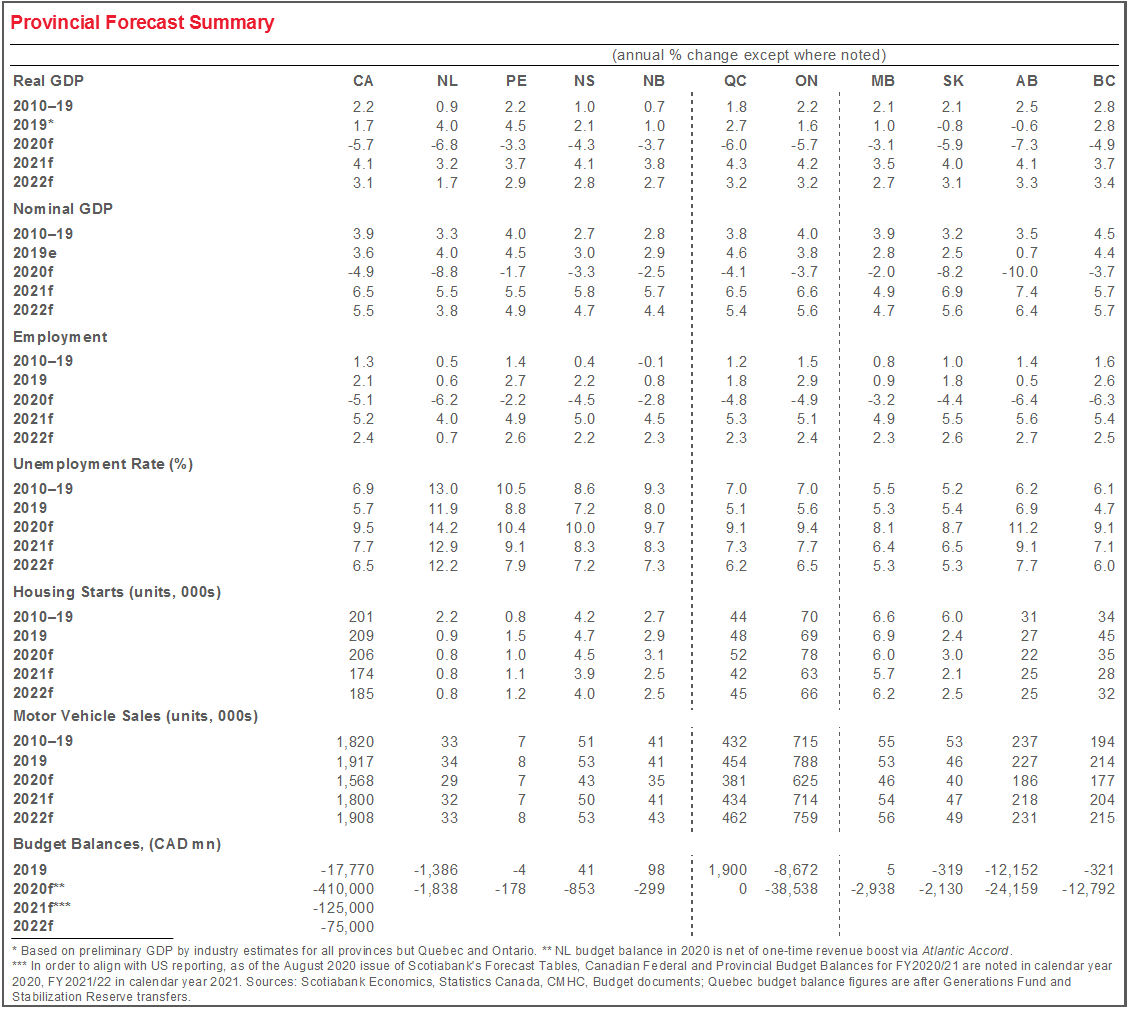

Sources for chart and table: Scotiabank Economics, Statistics Canada, CMHC, NS Finance, Industry Canada.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.