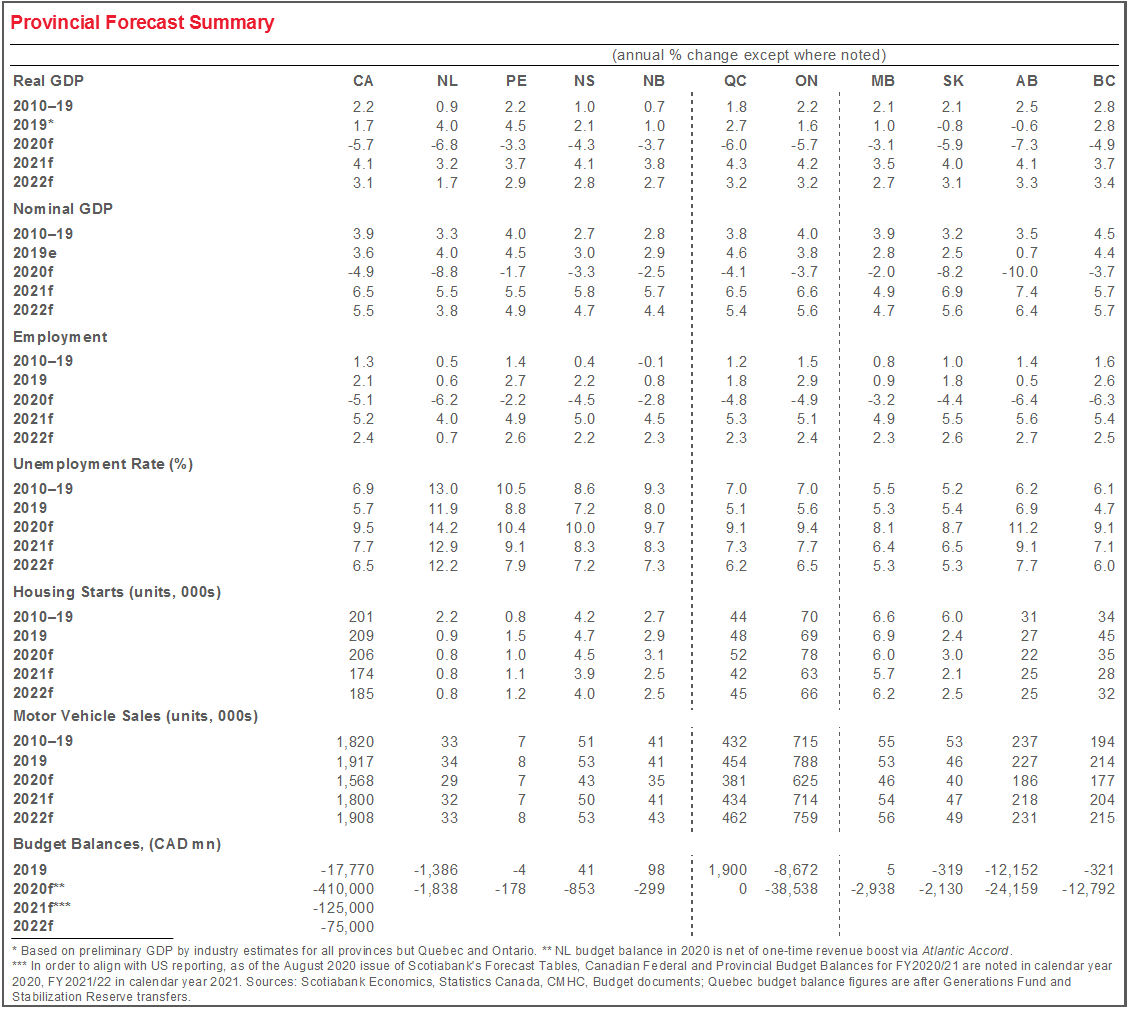

DIVERSIFICATION ONCE AGAIN CUSHIONS AGAINST RECESSION’S BLOW

Having withstood the peak of the initial phase of the pandemic, Manitoba’s diversified economy again looks to be in position to come out of a recession relatively unscathed. The Province’s broad industrial base helped keep its decline to just 0.2% at the height of the Global Financial Crisis (GFC).

Success containing the virus’ first wave has enabled early reopening and broadly supported labour market outcomes. Jobs in retail & wholesale trade, information, culture & recreation, and accommodation & food services—the sectors most adversely impacted by lockdowns—took a significant hit but account for small employment share relative to other provinces. Meanwhile, the rise to date in full-time, high-wage finance & insurance and professional, scientific & technical services jobs bodes well for a recovery in related incomes.

Data released to date for the agriculture sector suggest a soft start to the year, but the months ahead may yield better results. Excluding direct payments, farm cash receipts were down 6.8% y/y in H1-2020, second-worst among the provinces. Yet prices for cattle, corn, soybeans, and canola—all key products in the Keystone Province—have all seen firmer prices in more recent months amid tight world market supplies, and farmers are reporting above-average harvests due to favourable weather. Sino-Canadian diplomatic tensions remain a challenge—canola and soybean shipments have slowed to a trickle since 2018, though they have seen improvement this year amid lockdown removal and broadly rising Chinese buying.

For trade, Manitoba has been held back by the transportation equipment manufacturing industry as in Ontario. Related shipments—though improving since the summer—appear to have been hit hard by early-year auto sector shutdowns, dominating gains in agriculture and food manufacturing. Aerospace prospects face a particularly uncertain outlook given the near-stop of the travel and airline industries. As well, Manitoba’s well-documented interprovincial export relationships are unlikely to provide much respite from this downturn given the widespread nature of the pandemic, though a solid rebound can reasonably be expected as demand recovers.

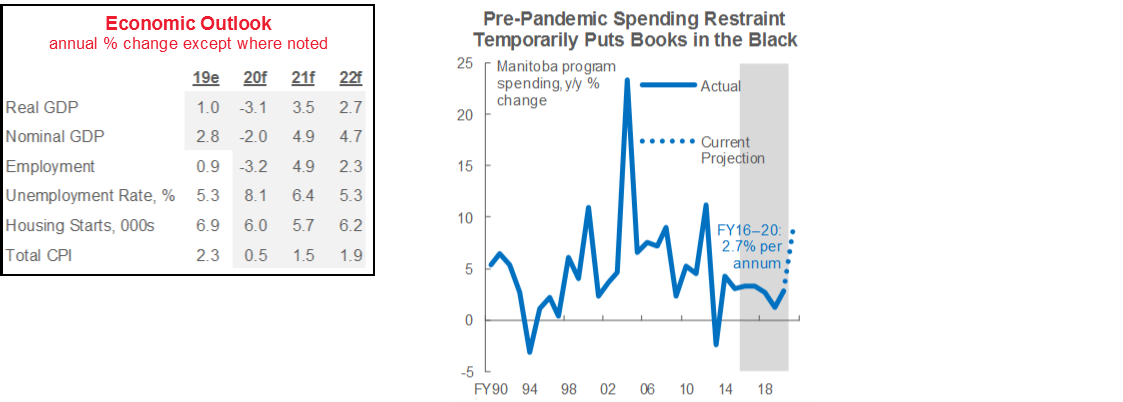

Manitoba recently recorded an unexpected $5 mn fiscal surplus in FY20—its first since before the GFC. An income tax revenue windfall—attributed to pre-pandemic household income gains—were the primary driver of the result. Manitoba also kept program spending growth to an annual mean of just 2.7% over FY16–20, the third-lowest rate of any Province over that period and its second-slowest pace in a five-year span since the 1990’s (chart).

Last year’s black ink puts the Province’s balance sheet in a stronger-than-anticipated position entering the pandemic, but fiscal pressures will nonetheless be significant over the medium term. This year, Manitoba expects to run a record $2.9 bn (4% of nominal GDP) shortfall and carry an all-time high net debt burden of 37% of output. Those figures reflect expectations of an historic 8% decline in total revenue and a sizeable 8% jump in total expenditures. Still, the generous spending package—including funds for medical supplies, infrastructure outlays, wage subsidies for students, and workforce participation incentives—may bolster the recovery so long as second wave containment efforts are successful.

Sources for chart and table: Scotiabank Economics, Statistics Canada, CMHC, MB Finance.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.