NEW HEADWINDS EMERGE AFTER SUCCESSFUL PHASE ONE

We anticipate that BC’s economy will be a relatively strong performer among the provinces this year, but region-specific challenges have emerged in the summer months. BC’s broad-based pre-pandemic expansion and fiscal health were the envy of the provinces: since the last commodity price drop began in 2014, BC’s 14.7% real output gains trailed only those of PEI, and its 13% job creation led all other jurisdictions. That resulted in seven consecutive annual surpluses beginning in FY14, one of the lowest net debt burdens of any Province, and a vaunted AAA credit rating.

BC’s labour market has lost more steam than other jurisdictions since the post-lockdown burst of activity. BC successfully contained the virus’ first wave and was able to ease lockdowns relatively quickly, but full-time employment and hours worked have generally lagged national-level results since April. That partly reflects BC`s industry mix. Information, culture & recreation and accommodation & food services—slammed by cratered tourist activity via COVID-19 restrictions—together accounted for about 10% of BC’s workforce last year—more than any other province. As well, construction, while resilient, is coming off of all-time highs in jobs and homebuilding early last year.

Home sales activity has recovered nicely from early-year lockdowns. Existing home purchases and listings gains in Southern BC cities—in the midst of strong population and employment gains plus elevated housing absorption rates pre-pandemic—have generally outpaced the national mean in the last two months. Pent-up demand appears to be supporting those markets alongside rock-bottom borrowing costs. Yet the outlook is murky. In particular, continued weakness in immigration amid border closures and apprehension about international travel is expected to weaken household formation. Population growth has already cooled to 1.1% y/y in Q2-2020, after hovering near two-decade highs of about 1.6% in 2018–19.

For trade, record prices in the staple lumber industry have helped to offset the drag from still-soft production volumes (chart) and cratered global export demand. Expecting a pandemic-induced plunge in demand, lumber producers cut back output by more than 50% y/y in April. Yet, with hardy US home building and output only beginning to ramp up, prices for Western lumber surged to all-time highs. We anticipate that prices will ease entering 2021, though much depends on pandemic impacts south of the border and producers’ ability to replenish inventories in the winter months.

Work related to the LNG Canada Coastal Gaslink Export Pipeline megaproject is ongoing—albeit with COVID-19-related delays—but the industry faces broadly less certain prospects in the weaker commodity pricing environment. The softer global backdrop has led to cancellations, postponement of construction and investment decisions, and difficulty obtaining funding around the globe; as such, sectoral upside risk that we previously identified in BC is far less likely than before COVID-19. Still, the province maintains advantages such as abundant reserves and shorter shipping distance to Asia than the US Gulf Coast.

With the October 24 provincial election looming, the Province last month released details of its economic recovery plan. Pillars of the plan include a refundable tax credit for firms that hire modest and medium-income employees, and a sales tax rebate on new purchases of new machinery and equipment. These targeted efforts have potential to support job creation and investment activity on the margins, though the course of the virus will undoubtedly be the primary driver of growth going forward.

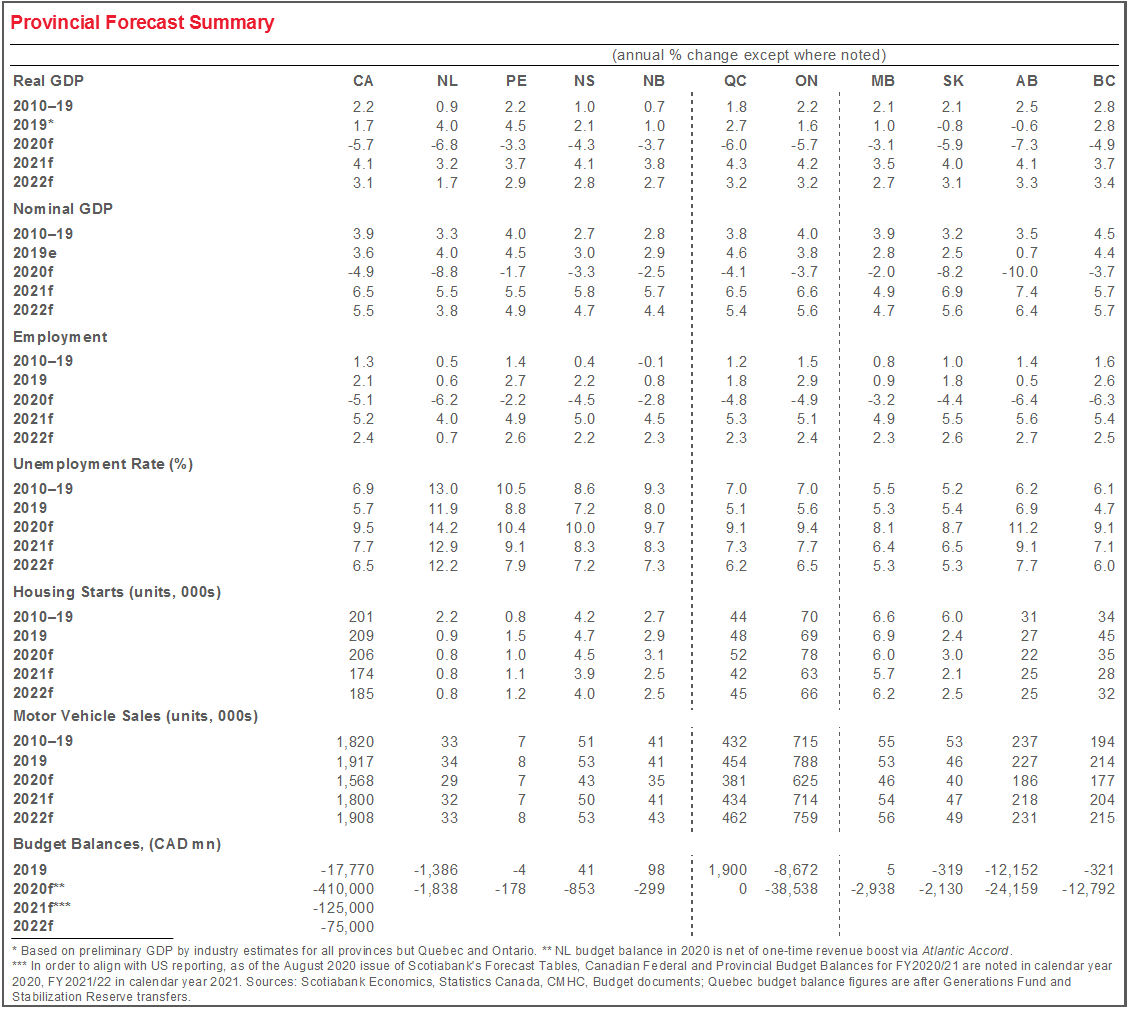

Sources for chart and table: Scotiabank Economics, Statistics Canada, CMHC, BC Finance, BC Stats, Random Lengths.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.