SOLID REBOUND TO FOLLOW DEEP DROP LAST YEAR

- We expect early-year momentum and base effects to support very strong growth in Alberta this year.

- Among non-energy sectors, forestry, chemicals, and agriculture have sanguine near-term outlooks.

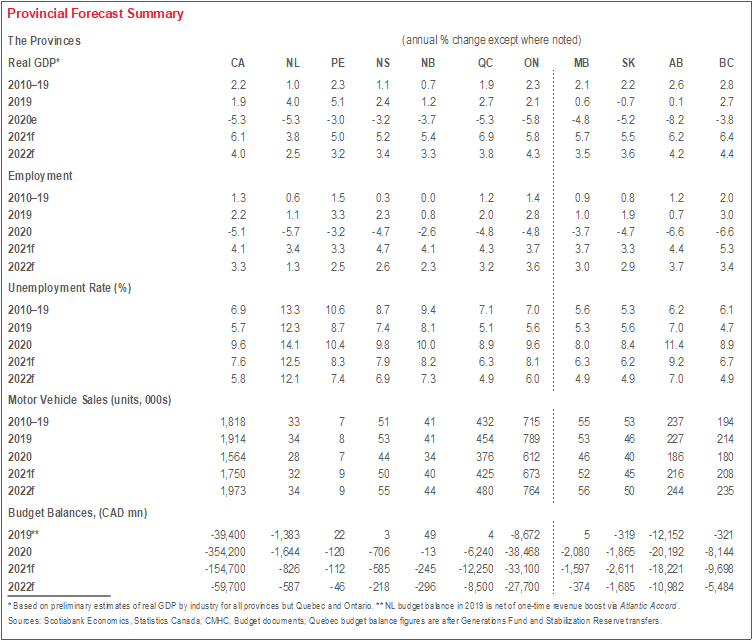

Incoming data continue to highlight the spillover effects of oil prices on Alberta’s economy. Last year’s estimate of an 8.2% real GDP decline was anchored by crude price plunges and the deepest drop of any province; construction and manufacturing saw even steeper declines than oil and gas extraction. Yet by May of this year, WCS and WTI had returned to pre-virus levels. Supported by that improved pricing backdrop, Alberta oil output is up on a y/y ytd basis as of April, and drilling activity has surged, though it remains historically low. Preliminary Q1-2021 non-residential business investment data suggest that private-sector capital outlays rose to begin the year, an idea reinforced by the 64% (q/q ann.) climb in national-level oil and gas spending. Still, the latter is at its fourth-lowest recorded since at least 2013.

We expect early-year momentum and base effects to result in strong growth in Alberta in 2021, though longer-run prospects are less certain. For oil production, we assume growth in the 7% range this year and about 2% in 2022—in line with recent provincial government projections. That should drive solid 2021 export growth. For investment, we await a strong advance this year, but not one in the range of what might have historically been expected in a year of 50%-plus oil price gains. Capital discipline is widely expected to be the industry trend after last year’s price volatility and amid greater international producer competition plus investor appetite for clean energy sources, though work is proceeding on several renewable projects in Alberta.

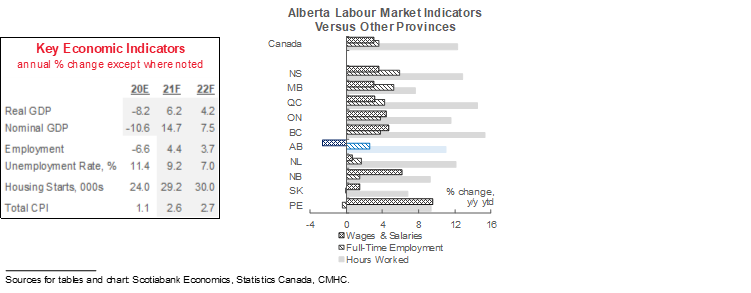

Alberta’s labour market looks to have gotten off to a slow start relative to other provinces. In 2020, Alberta witnessed the steepest drop in wages and salaries, and the second-largest falls in full-time employment and hours worked among the provinces. To date in 2021, Alberta is lagging national-level gains across all of those indicators. Lingering effects from lockdown measures put in place to control a severe third pandemic wave may hinder the recovery, but we are encouraged by the recent pace of infection rate decline and the province’s accelerated reopening plan.

Among non-energy sectors, forestry, chemicals, and agriculture have sanguine near-term outlooks. Lumber prices have eased of late but remain historically strong; Alberta production is trending higher as mills aim to meet voracious North American home construction demand. Work continues at the Heartland Petrochemical Complex despite reports of recent COVID-19 outbreaks; as we noted last quarter, chemical manufacturing investment intentions are nearly 25% higher than preliminary estimates for last year. Crop receipts climbed a hefty 31% y/y in Q1-2021—supported by strong wheat and canola prices—and we expect livestock producers to benefit from rising cattle prices and stronger output after plant shutdowns last year. Broadly speaking, the industrial sector should gain from the hefty US expansion forecast this year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.