ECONOMIC OVERVIEW

- With the Fed’s policy decision in the rear-view mirror, beaten-down global markets may find some comfort in a relatively quiet data calendar in the US and Europe.

- In Latin America, Banxico and BanRep’s policy decisions are the highlight of the region’s upcoming trading week where we expect respective rate increases of 75 and 150bps.

- We forecast another increase in Chile’s unemployment rate and a sharp year-on-year decline in retail sales. Peru’s week ahead is quiet as markets and economists turn less optimistic about a material softening of inflation.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

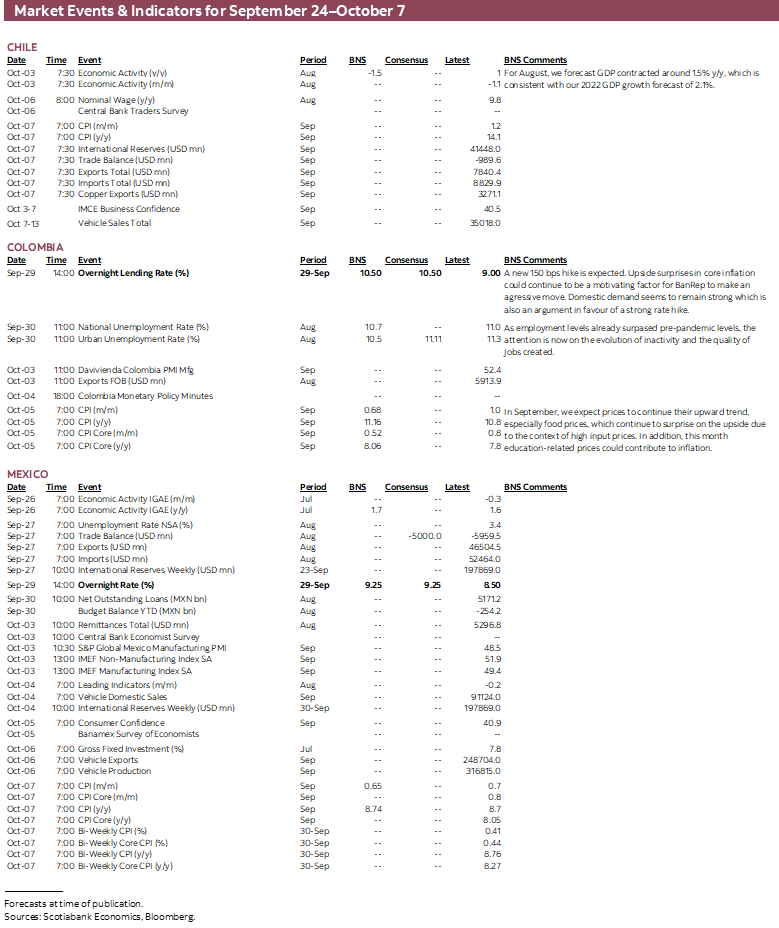

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period September 24–October 7 across the Pacific Alliance countries and Brazil.

Economic Overview: Banxico and BanRep to Stick to Large Hikes

Juan Manuel Herrera, Senior Economist/Strategist

+44.207.826.5654

Scotiabank GBM

juanmanuel.herrera@scotiabank.com

- With the Fed’s policy decision in the rear-view mirror, beaten-down global markets may find some comfort in a relatively quiet data calendar in the US and Europe.

- In Latin America, Banxico and BanRep’s policy decisions are the highlight of the region’s upcoming trading week where we expect respective rate increases of 75 and 150bps.

- We forecast another increase in Chile’s unemployment rate and a sharp year-on-year decline in retail sales. Peru’s week ahead is quiet as markets and economists turn less optimistic about a material softening of inflation.

With the Fed’s policy decision in the rear-view mirror, beaten-down global markets may find some comfort in a relatively quiet data calendar in the US and Europe—at least until the release of September inflation prints on Friday (PCE and CPI, respectively). On Friday, the UK government’s “mini-budget” that presented a number of fiscally unsound policies on top of energy bills support for households and businesses lit up gilt yields (2s rose up to ~45bps on the day) and pulled global rates even higher from post-Fed levels while injecting an extra dose of risk aversion in markets.

The Fed’s hawkish missive saw markets take the yield on 2-yr UST notes through 4% for the first time since 2007, up about 30-35bps over the week, and market participants will monitor comments from Fed officials for clues on the size of their next move and the bank’s terminal rate.

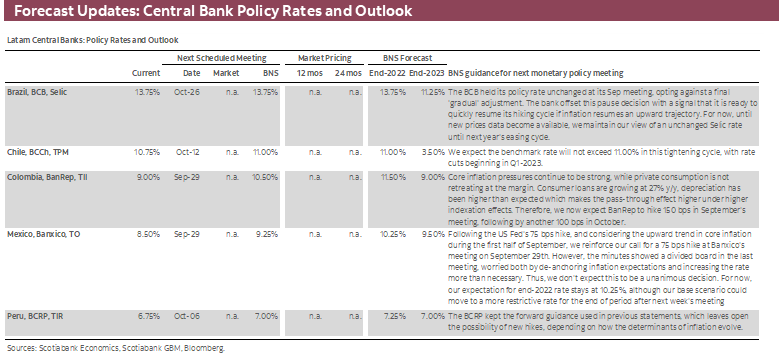

In Latin America, Banxico and BanRep’s policy decisions are the highlight of the region’s upcoming trading week.

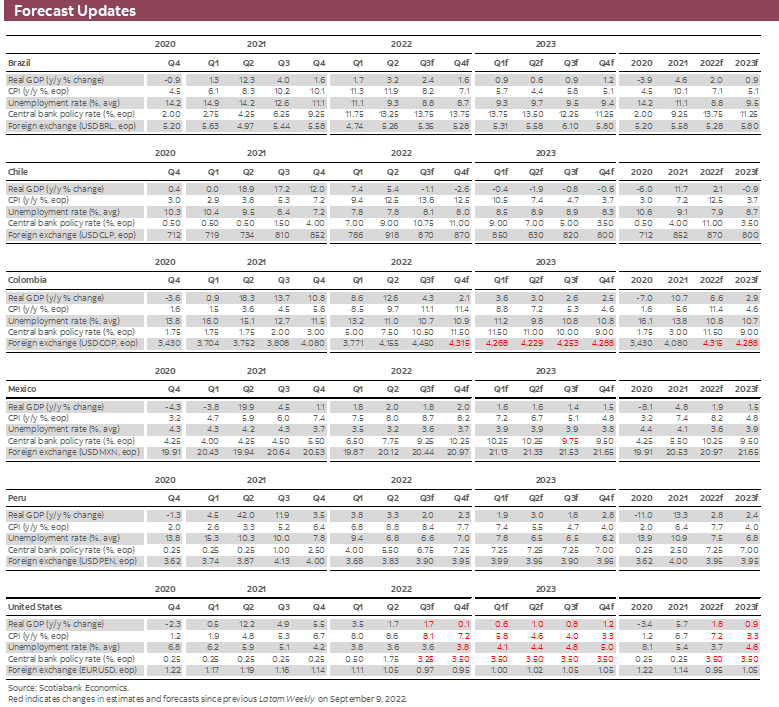

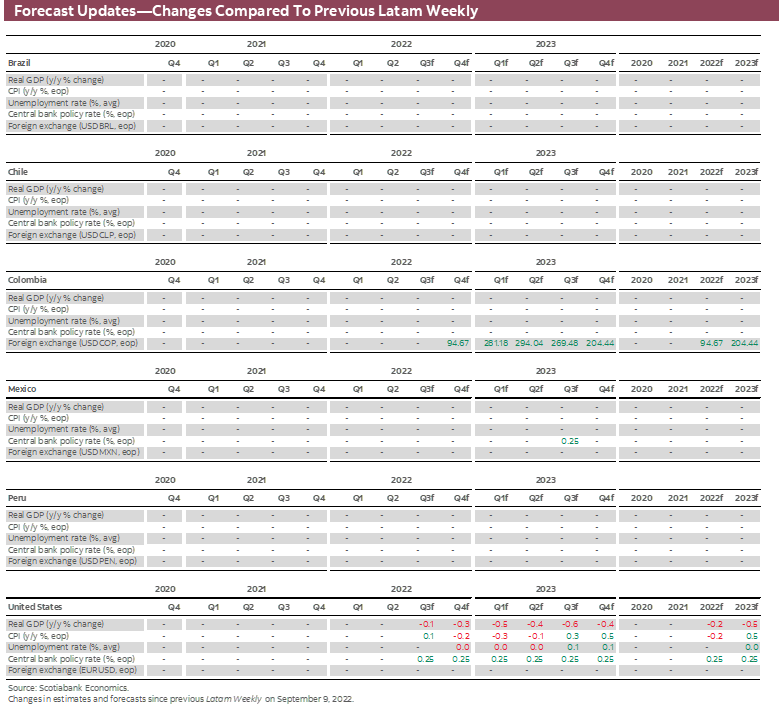

On Thursday, we expect Banxico to match the Fed’s three-quarter point hike given persistent inflationary pressures at home that continue to challenge Banxico’s projections (see our Mexico team’s write-up below). Data released this week showed bi-weekly core CPI rising by 0.44% 2w/2w and 8.27% on a year-on-year basis, and headline annual inflation has practically shown no moderation. We think the bank will follow this week’s 75bps move with another cumulative 100bps in rate hikes by year-end to 10.25% that will culminate its hiking cycle—though rate risks are tilted to the upside.

As for BanRep, we anticipate a 150bps move on Thursday that matches the median submission to Bloomberg, though with about 40% of economists expecting a 100bps move (see Colombia section). Inflation in the country continues to surprise higher and price pressures are becoming more widespread—as reflected in core CPI measures. Meanwhile, economic growth remains above potential. Combined, these circumstances give BanRep plenty of justification to launch another large hike.

Chile releases labour market data next Thursday where we expect to see another slight increase in the country’s unemployment rate as momentum in jobs growth lags that observed in the expansion of the labour force (see Chile section). Economic activity figures published on Friday are projected to show a sharp decline in retail sales as the central bank’s rate increases (alongside steep inflation) restrain household spending. Boric’s Ministry of Finance will also present its 2023 budget bill to Congress next week which, according to guidance provided by officials, should include only a ‘moderate’ increase in spending next year.

Finally, Peru’s calendar is bare of major data or events next week, but we think markets and economists (including ourselves and those at the central bank) are turning less optimistic about a material softening of inflation in the country (see Peru section). This may keep inflation expectations elevated and the BCRP on a longer tightening path, but for now we maintain our view of only two more 25bps hikes in this cycle (in October and November). On Friday, Bloomberg publishes the results of its September economists survey on Peru.

Elsewhere in the region, markets will monitor polls ahead of Brazil’s first round presidential election next Sunday. As polls stand, the most likely outcome is that neither Lula nor Bolsonaro will garner the simple majority vote required to be declared victorious without the need for a second-round vote. However, recent polls (e.g. DataFolha at 47% Lula, 33% Bolsonaro) have increased the odds of former president Lula achieving this feat.

In Europe, Ukraine war risks will figure in the market’s radar with annexation ‘referendums’ in South and East Ukraine planned over the next few days as Russia tightens its grip on the region and threatens a nuclear response to attacks on its ‘territory’.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Weak Economic Indicators, Good Political Signals

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Chile’s statistical agency (INE) will release labour market data for the quarter ending in August on September 29. We expect the data to show another slight increase in the unemployment rate as employment growth lags the expansion in the labour force.

On Friday, sector-level economic activity data will be released by the INE, including retail sales for August. Based on our tracking of credit and debit card purchases we forecast a 15% y/y (2% m/m) decline in retail sales. Overall, we observe a normalization in consumer goods imports, a significant replenishment in inventories, and a strong deceleration in banking credit.

That same day marks the deadline to present the 2023 Budget Bill to Congress with the government signaling “moderate” austerity. The Ministry of Finance has indicated that public spending would expand by between 4% and 5% ‘only’. It is highly likely that during the coming months, when economic activity and employment figures show a weak economy, with still high inflation, high short-term interest rates, and less private investment, several congresspeople will demand new universal aid. We estimate that the Government will resist these pressures by calling for fiscal prudence and instead provide targeted/limited aid to lower-income households.

On September 22, in New York, the Finance Minister indicated that USD12bn in sovereign debt would be issued in 2023, directionally very much in line with our call that debt issuance next year would not exceed USD16bn (see our Latam Insight). More details will be provided in the Budget Bill due to Congress at the end of September but we anticipate that this news will be welcomed by long-term interest rates (lower) in Chile in an international context where important increases in external interest rates have materialized.

In the political field, the constitutional process remains in a path of moderation. For now, talks continue between the political parties, with the expectation that an agreement will be reached in the coming days. Right-wing parties are attempting to institute “limits” on the work of the body drafting the new constitution, thereby significantly minimizing the likelihood of having a new far-left constituent assembly. We believe that the market is still attentive to these signs of moderation that could support better relative performance of Chilean assets compared to those of other emerging markets.

Colombia—Monetary and Fiscal Policy in the Spotlight; 150bps Hike Expected from BanRep

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

María Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

After last year’s presidential election, monetary and fiscal policies in Colombia have been in the spotlight. BanRep remains under pressure since headline inflation in August surprised to the upside again, while core inflation continues to show signs of demand-driven price pressures. In fact, YTD ex food inflation has increased 4.4ppts. Additionally, indexation effects have lifted the market’s and the analysts’ consensus’ inflation expectations for 2023 to between 7% and 9.5%—significantly higher than BanRep’s target range (2–4%). What’s more, economic activity, despite showing some marginal deceleration, still is above its long-run potential, mainly owing to much higher-than-expected private consumption.

Amid resilient growth and stubbornly high inflation, the market is anticipating a 150bps hike at the September 29 meeting followed by a 100bps hike at the October meeting, while the analyst consensus in the latest BanRep survey anticipates a 100bps move at next week’s meeting and another 100bps in October.

At Scotiabank Colpatria, we are more closely aligned to market expectations of 150bps since we do not see a sufficient cooling of the economy that would warrant a reduction in the speed of tightening. Meanwhile, many central banks such as in Chile, Sweden, and New Zealand, among others, had to show a more hawkish stance due to stronger and more persistent inflation—also present in Colombia. Beyond the debate on how high to take the policy rate, Colombian policymakers will need to decide how long higher rates will last. With GDP growth remaining solid, and inflation continuing to point north, markets have moved to discount a higher terminal rate in a still aggressive movement.

As for fiscal policy, the 2023 budget in tandem with tax reform will be the first subject of discussion for Petro’s administration. Congress approved a COP405tn budget for 2023, which is COP14tn higher than the original plan presented by Duque’s Government. This additional spending is lower than the expected extra revenues from the tax reform, but according to the fiscal rule committee, additional budgetary room would also be supported by better economic activity. In fact, on an investors’ trip to New York, Minister Ocampo stressed that 33% of the ‘new’ revenues from the tax reform will be used for a reduction of the fiscal deficit and towards net debt reduction, while 66% of additional revenues will be used in investment and social expenditure to comply with the president’s program. Additionally, Ocampo said that external debt will mostly be contracted with multilaterals, which should reduce the pressure on market pricing of Colombian debt, while domestic issuance is not expected to change. Meanwhile, Ocampo also said that for the first time in four years Colombia will have a primary surplus balance, in line with the fiscal rule path of 0.2% of GDP. Therefore, although the space for countercyclical fiscal policy is almost zero, next year’s fiscal accounts apparently will likely not be the source of asset volatility. On the contrary, they may bring provide some comfort to the COLTES market.

Mexico—After the Fed’s Hawkish Message, Another 75bps Hike is the Obvious Choice for Next Week’s Banxico Meeting

Luisa Valle, Deputy Head Economist

+52.55.5123.1725 (Mexico)

lvallef@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Considering the Fed’s latest 75bps hike and local headline inflation coming in higher than consensus (with the core component rising), we have no doubt that Banxico will raise its policy rate by 75bps for the third consecutive time, to 9.25%, matching the Fed’s pace of tightening. However, several factors (which we cover below) lead us to believe that there are upside risks to our 10.25% year-end Banxico rate forecast, though for the time being this remains our expectation.

Though the tone of the statement was virtually unchanged, the Fed’s outlook now has a more restrictive sense, even suggesting a terminal rate near 5%, which could mean an additional 75 bps and a further 50 bps increase later this year (see Scotiabank Economics’ recap here). In addition, the Fed’s inflation path is now higher and more persistent as the FOMC expects some stickiness in inflation at elevated levels, reaching its 2% target only as late as 2025.

Regarding inflation in Mexico, annual headline inflation again exceeded expectations (see here) in the first fortnight of September, although it slightly edged lower from its previous reading (8.76% vs 8.77% previous, 8.71% consensus), and core inflation continues on the rise. In this regard, the country’s consumer protection agency (PROFECO) indicated that in the coming days, President López Obrador will release an update to the anti-inflation plan (PACIC), with which the government plans to curb further increases in food and energy items. However, the plan has been successful in slowing increases only in energy prices. As for the prices of other goods, the effectiveness of the plan has been quite limited.

Mexican inflation also has certain domestic characteristics and factors that make it different from inflation in the US. Further to the imbalances observed in the economy owing to disruptions in supply chains, other factors in Mexico include problems with the rule of law and insecurity, wage cost pressures, and adverse climate events. In this sense, we take as positive the news that according to the Regional Economic Report for Q2-2022 recently published by Banxico (see here), a higher proportion of business agents in April–June expected input and sales prices to increase at lower rates, or remain unchanged in the next 12 months compared to the previous quarter.

Nonetheless, inflation expectations continue to rise; analysts participating in the Citibanamex survey now expect inflation to end 2022 at 8.36% from 8.20% previously. Therefore, we expect Banxico to update its outlook in next week’s communiqué, showing a higher inflation peak than its previous forecast, keeping it at elevated levels for a longer period, and only approaching the 3% target after Q1-2024, in line with the Fed’s new expected inflation trajectory.

Regardless of these factors, we do not expect the decision for a 75bps increase to be unanimous. One reason for this is that at the August meeting the Board removed the word “forceful” from the statement regarding the measures to be taken as conditions require. In addition, the minutes revealed not only the Board’s concerns about the de-anchoring of expectations but also about growth, including worries related to weather events such as summer droughts in northern states. The regional report also highlighted crime and security concerns as a downside risk to growth.

Although the median economist in the Citibanamex survey expects the bank’s rate to be at 10.00% by the end of the period, a handful of analysts expect a rate higher than 10.00%, including us (5/33 surveyed, charts 1 and 2). After H1-Sept inflation figures and a more hawkish Fed, the TIIE swap curve shows a market split between 75 and 100bps for the September decision, and a rate higher than 10.25% at the end of 2022, which has undoubtedly been crucial for the peso’s performance, which has appreciated by ⅔% during the year—making it the only major currency alongside the BRL to strengthen against the USD in 2022. For now, we maintain our 10.25% rate forecast for end-2022.

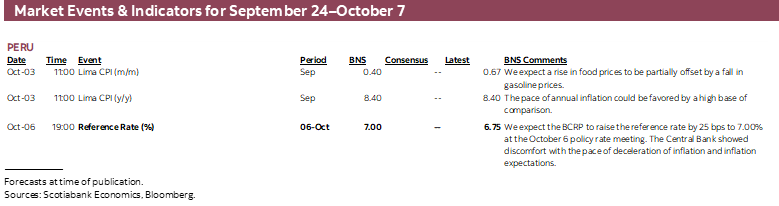

Peru—The Declining Trend in Peru’s Inflation Lacks Conviction, Worrying the BCRP

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Monetary authorities have seemed disappointed lately. In recent events, monetary authorities have suggested: first, the high levels reached by inflation were unexpected—both by the BCRP and others—and second, that although inflation had started to slow—declining from 8.8% in June to 8.4% in August—it was doing so at a much slower pace than anticipated. We agree. Inflation is declining with very little conviction.

Conviction may weaken further in September. A couple of government institutions that track key agricultural and fuel prices allow us to get an early peek at how inflation is trending. Currently, this partial snapshot suggests a monthly inflation reading of between 0.34% and 0.4% m/m for September. If so and given that inflation for the month of September last year was 0.4%, this would keep twelve-month inflation at close to its current level of 8.4%.

Velarde also suggested that the BCRP expects inflation to continue above the ceiling of the BCRP’s target range (the target range is 1–3%), for longer. Basically, the view is changing, both at the central bank and, we believe, in the market, regarding the pace at which inflation will soften going forward. This will likely affect the inflation expectation figures that are so important for the BCRP. Inflation expectations (twelve months out from now) have declined, but also without conviction, from 5.3% in June to 5.1% in August.

If inflation forecasts by analysts and businesses for 2023 tick higher in line with changing sentiment, then inflation expectations for 2023 could easily stop correcting downward and may even rise. We won’t know that for sure until the BCRP’s policy meeting on October 6. Having said that, we are inclined to believe two things: that there will be a pause in September in the downward trend in inflation and that there is a good chance that inflation expectations will rise, if only marginally, in their next print or two.

Additional issues have emerged that complicate Peru’s inflation picture further: 1) soft commodity prices are no longer clearly declining; 2) freight costs have rebounded; 3) the prices of certain staples, including potatoes, are starting to face the impact of fertilizer shortages at accessible prices to small farmers; 4) bad weather is affecting fuel shipments (this is a temporary issue, but could impact inflation in September). Although these issues are being compensated by the global decline in fuel prices, it’s not clear how the different factors will balance out in the months ahead. Meanwhile, the decline in inflation will continue to lack conviction. Under this scenario, a 25bps increase in the BCRP reference rate in October continues to be the most likely scenario.

POLITICS: REGIONAL AND MUNICIPAL ELECTIONS ARE COMING UP

Regional and municipal elections will be held on October 2. This could potentially colour the political spectrum differently. Or not. Regional and local elections tend to be a very mixed bag, where the left-right axis is muddled by regional groups and interests within their own parties and representatives, and by individual candidates of local color and importance. This makes the results of these elections hard to read from a national political perspective. Local groups and individual candidates do not fit into the left-right or national party frameworks easily.

However, there are a few things to look out for. Who will win Lima will be key. How strong a showing the left will have in the country, and what will be the preferred alignment, whether with the more centric Juntos por el Perú (JPP), or the more radical Perú Libre will also be a major focus. How well candidates from national parties will do in general, compared to local regional independents is another important consideration.

Currently, the race for Lima is very biased towards the right. The three leaders, who according to a September 9 poll by Ipsos combine for two-thirds of voting intentions, are candidates that are right-of-centre and, in general, opposed to the Castillo Government. Meanwhile, the two leftist candidates don’t have more than 6% of the vote combined. This is a strong statement against the Castillo Government, but it is only Lima. The true proof of how sentiment has moved along the left-right axis will be voting outside the capital region.

In Lima, Daniel Urresti (Podemos) and Rafael López Aliaga (Renovación Popular) are the more controversial of the three leaders, as they are closer to the radical right. They would conceivably use the Lima City Hall as a platform to magnify a greater anti-Castillo message. The third-place candidate, George Forsyth (Somos Peru), who is lagging a bit, but gaining ground, is less confrontational and less prone to political posturing, and more likely to actually dedicate his time to do the job he would be elected for.

In Lima, about 20% of voters are still undecided. The proportion is greater in the rest of the country. One wonders whether even those who have decided their vote have done so with conviction.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.