- Banco de México’s Governing Board decided to keep the reference interest rate at 6.50%, in a unanimous vote.

- The Governing Board expects economic activity to expand during Q2 2026, with downside risks persisting.

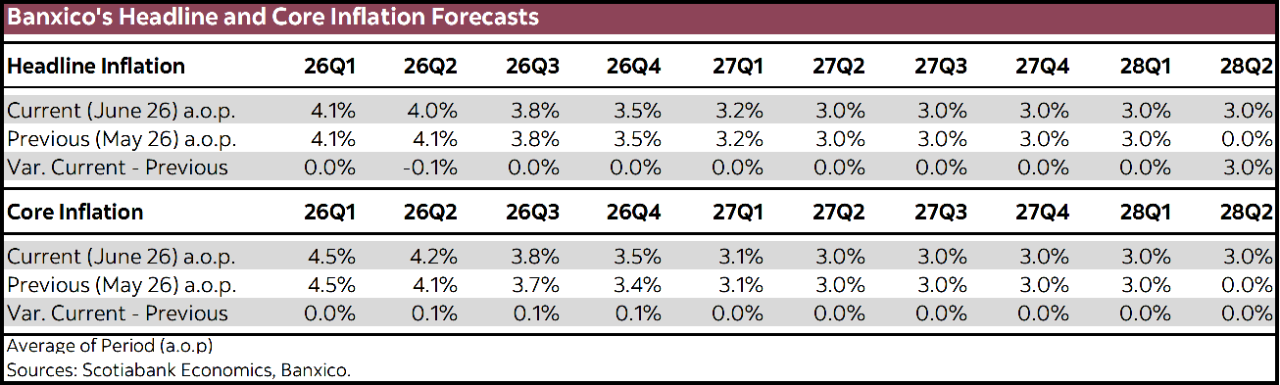

- Headline inflation forecasts remained unchanged for the remainder of the year, with convergence to the target expected in Q2 2027.

- We maintain our view that the target interest rate will close the year at 6.50%, subject to the path of inflation, the exchange rate level, and the interest rate differential between Mexico and the United States.

Banco de México’s Governing Board unanimously decided to leave the reference interest rate unchanged at 6.50%. This decision was in line with market expectations, after the previous decision explicitly brought to an end the easing cycle that began in March 2024 and accumulated 475 basis points. In addition, the Board marginally revised upward its core inflation projections, while keeping unchanged its headline inflation estimates, as well as the expected convergence to the 3.0% target by the second quarter of 2027.

The statement noted that, during the first quarter of 2026, global economic activity expanded at a pace similar to that of the previous quarter. This occurred despite an increase in headline inflation in some advanced economies as a result of higher energy prices, while core inflation showed mixed behaviour across countries. It highlighted that the Federal Reserve kept its reference rate unchanged at its June meeting, that financial markets showed volatility, and that commodity prices declined, alongside an appreciation of the dollar and increases in most U.S. Treasury yields. Finally, the statement reiterated the persistence of an uncertain outlook regarding the conflict in the Middle East and its repercussions, although recent negotiations suggest that a solution may be on the horizon.

Regarding domestic conditions, the Governing Board noted that, since the last monetary policy decision, interest rates on government securities in Mexico declined across most maturities, while the peso depreciated. The Mexican economy is expected to expand during the second quarter of 2026 after contracting in the previous quarter; therefore, a greater degree of slack than previously anticipated continues to be expected, along with persistent downside risks going forward.

As for inflation, short-term forecasts were marginally revised downward (table 1), anticipating an average level of 4.0% during the quarter (vs. 4.1% expected in the previous decision) due to the moderation observed in the non-core component, especially agricultural products, in the reading for the first half of June when inflation slowed from 3.77% to 3.55%, surprising analysts. However, the short-term forecast for the core component was revised slightly upward to 4.2%, in line with observed persistence. The Governing Board reiterated that it expects headline inflation to converge to the target in Q2 2027, with the balance of risks skewed to the upside, including: disruptions from trade policies, inflationary effects from geopolitical conflicts, persistence of core inflation, climate-related impacts, cost pressures, and a depreciation trend in the peso. On the other hand, downside risks mentioned included: weaker-than-anticipated economic activity, a lower pass-through from cost increases, and lower pressures from the peso appreciation observed since last year.

We believe that the monetary policy decision reflects a neutral stance, although the balance of inflation risks remains skewed to the upside. This is because the statement reiterates that the Governing Board believes it is appropriate to keep the reference rate at its current level to address the challenges of the macroeconomic environment. In this context, it will be important to monitor the evolution of inflation and developments in the Middle East conflict, as well as the impact of higher energy prices and potential second-round effects on goods and services, in addition to domestic economic weakness, exchange rate behaviour, and the relative stance versus the Federal Reserve. We maintain our projection of a 6.50% rate by end-2026, as long as second-round effects from increases in taxes, tariffs, the minimum wage, and energy prices do not materialize. Finally, it will be relevant to analyze the minutes to be published on July 9th, 2026.

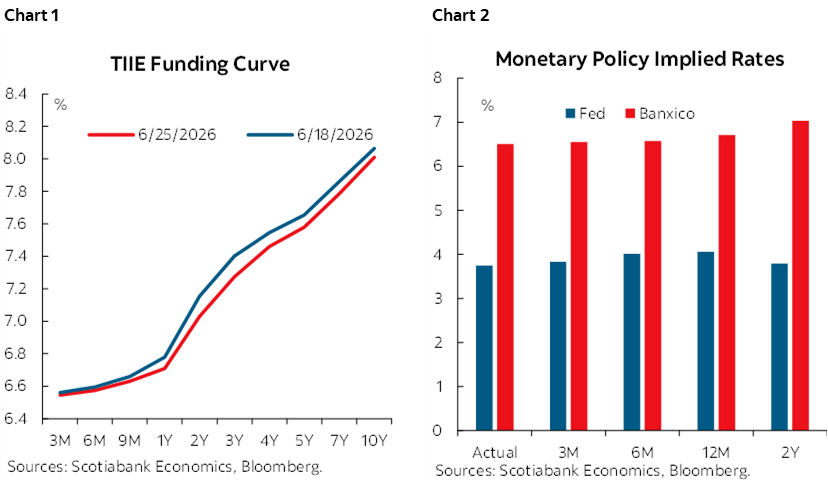

Regarding the market reaction, the exchange rate moved marginally and stood at MXN 17.50 per dollar. Meanwhile, the TIIE Funding curve (chart 1) showed limited moves. The short end (up to 1 year) declined between 3 and 1 bp, while the rest of the curve up to 30 years declined between 2 and 4 bp. The three-month implied curve stood at 6.55% (chart 2), while the one-year rate stood at 6.71%, implying market expectations for upward adjustments one year ahead.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.