- The South Korean economy has weathered the COVID-19 storm relatively well, yet a new surge in infections brings new clouds to the horizon. We expect the country’s real GDP growth to average 3.6% and 2.7% in 2021 and 2022, respectively.

- Strong global demand for South Korean electronics exports has provided significant support to the economy’s recovery momentum; the rebound has recently become broader with a solid pickup in domestic demand.

- Expansionary fiscal policies will continue to complement the Bank of Korea’s accommodative monetary policy stance.

- Consumer price inflation will stay elevated in the next few months largely due to base effects, before stabilizing around the central bank’s annual inflation target of 2%.

ECONOMIC GROWTH OUTLOOK

The South Korean economy is on a solid growth trajectory as it is emerging from the COVID-19 crisis less-harmed than most of its regional peers. The economy avoided large-scale lockdowns in 2020 thanks to a relatively successful virus-containment strategy; accordingly, the nation’s real GDP contracted by only 1% in 2020. An economic rebound has been underway since mid-2020, with output surpassing the pre-pandemic level in the first quarter of 2021. The country’s real GDP expanded by 1.6% q/q (non-annualized) and 1.8% y/y in Q1 (chart 1), with activity becoming more broadly based across external and domestic parts of the economy. Pent-up demand at home, continued supportive monetary and fiscal policies, strong global demand for South Korean exports, combined with base effects from weak activity last year, will continue to boost economic activity over the coming quarters; we forecast the country’s real GDP to expand by 3.6% and 2.7% in 2021 and 2022, respectively.

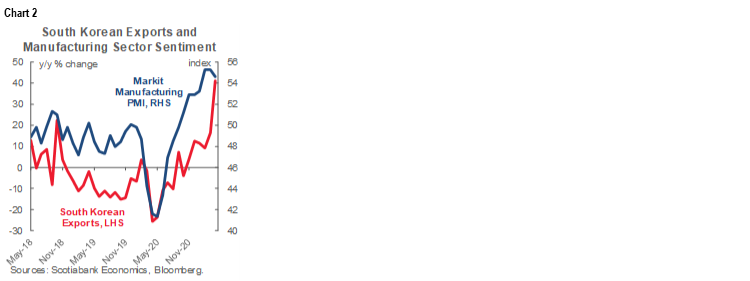

The external sector will continue to play an important role in South Korea’s growth story. Sentiment in the export-oriented manufacturing sector as well as Korean shipments abroad have rebounded strongly (chart 2). China and the US—the engines of the global economic recovery—are South Korea’s two most important markets, purchasing 29% and 12%, respectively, of South Korean total exports (as of 2020). Simultaneously, South Korea is benefiting from strong global demand for electronics products, which account for around 30% of the country’s exports. Moreover, demand conditions for South Korean exports of petroleum products as well as automobiles and auto parts remain favourable; nevertheless, the global chip crunch will likely have some adverse impact on related exports, such as mobile phones and auto parts. We expect Korean net exports to provide a boost to the country’s real GDP growth through 2022.

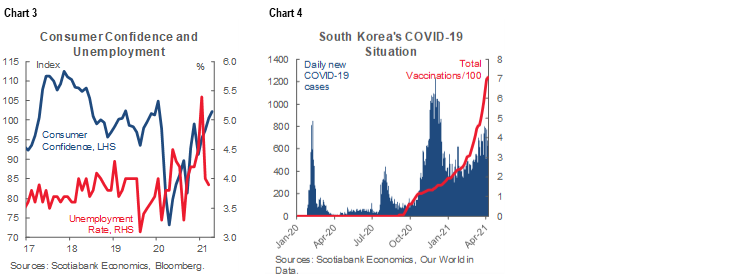

The outlook for private consumption has improved in recent months as consumer confidence and the labour market have strengthened (chart 3). Indeed, retail sales growth has picked up and South Korea’s unemployment rate has dropped to below 4% in after peaking at 5.4% in January. Nevertheless, we note that the most recent surge in COVID-19 infections (chart 4) poses a significant downside risk to household spending prospects; a worsening virus situation and an introduction of tighter virus-related movement restrictions and business closures could significantly dampen and delay South Korea’s economic recovery momentum. Moreover, South Korea’s vaccine rollout has been relatively slow, yet recent official communications imply that the country should be able to speed up its inoculation campaign significantly over the new few months.

On fixed investment side, signs are emerging that solid global demand for South Korean products is translating to stronger business outlays. While the outlook largely depends on the evolution of the virus-situation, we expect firms to continue to invest in new capacity over the coming quarters on the back of strengthening sentiment, low interest rates and a favourable fiscal policy backdrop.

An expansionary fiscal policy stance will continue to provide support to the South Korean economy. Over the course of 2020, the government passed four supplementary budgets to mitigate the adverse impacts of the COVID-19 crisis. According to the IMF, South Korea’s pandemic-related fiscal measures as of mid-March were equivalent to around 15% of GDP, consisting of 5% of GDP worth of additional spending and 10% of GDP of liquidity support. The first supplementary budget for 2021—of KRW 15 trillion, equivalent to 0.8% of GDP—was approved by the National Assembly on March 25. Extra public outlays will focus on supporting small businesses, the labour market, and the nation’s COVID-19 containment efforts.

MONETARY POLICY, INFLATION AND CURRENCY OUTLOOK

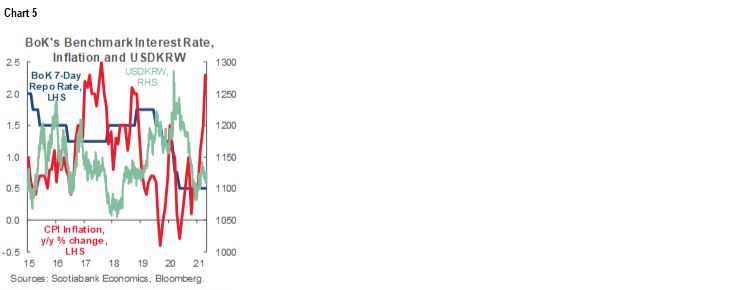

The Bank of Korea’s (BoK) monetary policy stance will likely remain unchanged until mid-2022, as it continues to assess the recovery’s strength and sustainability and as fiscal stimulus continues to work its way through the economy. The central bank has highlighted that it will maintain the accommodative monetary policy stance in order to support economic activity and stabilize consumer price inflation near the BoK’s annual inflation target of 2%. Meanwhile, the BoK’s policymakers will pay close attention to changes in financial stability conditions, such as fund flows to asset markets and household debt growth. We expect the central bank to start normalizing monetary policy with gradual interest rate hikes in the third quarter of 2022, taking the benchmark interest rate from the current level of 0.50% to 1.0% by the end of 2022.

Inflationary pressures in South Korea have picked up in recent months; the headline CPI increased by 2.3% y/y in April (chart 5). Meanwhile, price pressures at the core level (excluding agricultural products and oil) remain more muted with the core CPI rising by 1.4% y/y in April. Reflecting mostly base effects, headline inflation is expected to exceed the BoK’s 2% target over the next few months before easing to 1.8% y/y by the end of the year. We expect inflation to stabilize around the 2% y/y mark in 2022 in line with the BoK’s monetary normalization efforts.

Following pandemic-related market turmoil in early 2020, the South Korean won (KRW) strengthened by around 15% vis-à-vis the US dollar (USD) between May and December 2020 on the back of broader USD weakness. Since the beginning of 2021 the won has stabilized—and lost some of the earlier gains—reflecting investor expectations regarding US monetary policy normalization. We expect the KRW to remain range-bound versus the USD over the coming months, hovering between USDKRW 1100 and 1130. The KRW will find support from South Korea’s solid economic recovery amid strengthening global trade. Meanwhile, changes in international investors risk appetite and speculation regarding relative monetary policy trajectories are set to instill periods of a weakening bias on the KRW. We expect USDKRW close 2021 and 2022 at 1120 and 1160, respectively.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.