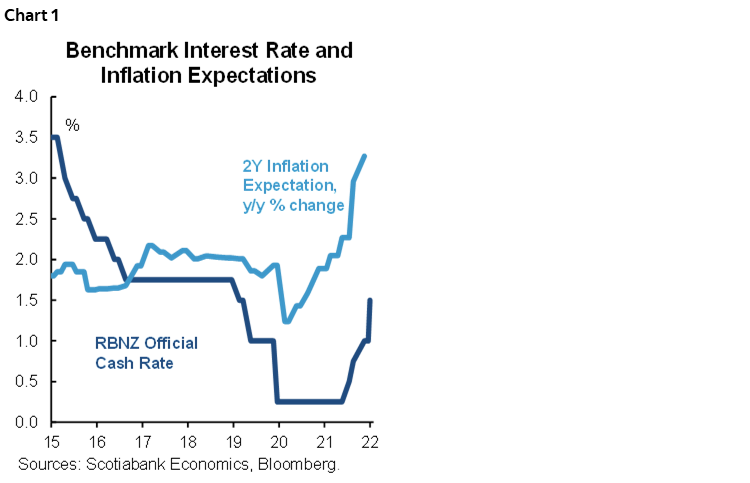

- The Reserve Bank of New Zealand raised the Official Cash Rate by 50 basis points to 1.50%, accelerating the pace of monetary normalization after three smaller rate hikes since last October.

- The central bank tries to reduce the risk of rising inflation expectations by bringing monetary tightening forward. The larger hike will also provide more policy flexibility for the coming quarters as the global economic environment is set to remain uncertain.

- As New Zealand’s inflation remains high and the labour market is tight, more interest rate increases are in sight. We expect the Cash Rate to reach 2.75% by the end of 2022.

The Reserve Bank of New Zealand’s (RBNZ) Monetary Policy Committee raised the Official Cash Rate (OCR) by 50 basis points to 1.50% following the April 13 policy meeting (chart 1). We—and the analyst consensus—had anticipated a 25 bps hike. Before this move, the central bank had lifted the policy rate by 25 bps at each of the prior three meetings (in February, November, and October). Continued monetary tightening is needed in New Zealand in the face of elevated inflation and a tight labour market. Indeed, the RBNZ’s policymakers assess that frontloading rate hikes is needed to help contain rapidly rising inflation expectations (chart 1). Moreover, the RBNZ sees that hiking more aggressively now builds policy buffers for the future given the uncertain global economic outlook. We expect further interest rate increases over the coming months, taking the OCR to 2.75% by the end of the year.

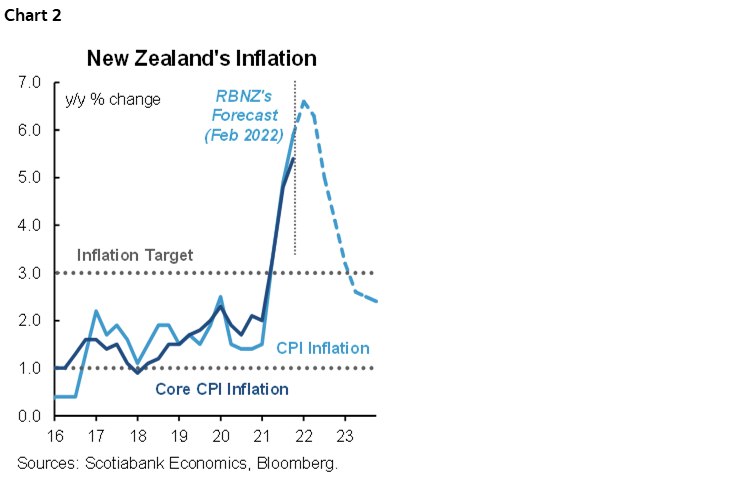

Inflation in New Zealand has picked up, and further acceleration is expected. Price pressures reflect both domestic and external factors, such as higher wage gains, rising capacity pressures, elevated inflation expectations, as well as global commodity price gains and supply chain bottlenecks. We estimate that headline prices rose 6.7% y/y in Q1 following a 5.9% gain in Q4 2021 (chart 2). Price pressures have intensified also at the core level, with the CPI excluding food, household energy, and vehicle fuels increasing by 5.4% y/y in Q4. CPI data for Q1 will be released on April 21. We expect headline inflation to remain in the 6.5–7.0% range in the first half of the year before starting to ease gradually thereafter. Inflation will likely return to the RBNZ’s 1–3% target around mid-2023. However, rising inflation expectations pose a notable upside risk to the forecast.

New Zealand’s economy is performing strongly on the back of still-low interest rates, solid balance sheets of households and businesses, supportive fiscal policy, as well as elevated prices for the nation’s exports. Nevertheless, some softening in activity is in sight as rising mortgage rates are dampening New Zealand’s real estate sector and global uncertainties are adversely affecting consumer confidence. Nonetheless, more cooling is needed to promote price stability as domestic capacity constraints persist. The RBNZ assesses that employment is above its maximum sustainable level. Therefore, the economy is facing labour shortages, which are causing rising wages and adverse impacts on economic output. According to the central bank’s assessment, the gradual reopening of New Zealand’s international borders will increase net immigration and labour supply only slowly. The country’s unemployment rate—at 3.2% in Q4 2021—is at its lowest level on record and wage inflation is accelerating as firms are competing for workers. The labour cost data for Q1 will be published in early May and will play a key role in determining the size of future OCR hikes by the RBNZ. The wage index increased by 2.6% y/y in Q4 and is expected to show further acceleration through 2022. Another indicator, the country’s average weekly wages, showed remuneration increasing by 5.7% y/y in Q4.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.