- The Japanese economy is set to enjoy solid real GDP expansion in 2021 and 2022 before it returns to a more normal growth trajectory in 2023.

- Rising vaccination levels and easing movement restrictions are underpinning consumer and business confidence, helping domestic demand to complement the export sector’s growth momentum.

- Japan’s fiscal policy is expected to remain supportive of economic growth over the foreseeable future.

- With significant inflationary pressures likely to remain absent, the Bank of Japan will maintain ultra-accommodative monetary policy well past other major central banks’ monetary normalization timelines.

ECONOMIC GROWTH OUTLOOK

The Japanese economy is emerging from a prolonged period of uncertainty arising from repeated waves of COVID-19. The nation is well-positioned to record two years of solid real GDP growth (by Japanese standards), after the pandemic triggered contraction of 4.7% in 2020 (chart 1). We forecast Japan’s output gains to average 2.5% y/y this year, followed by a 2% expansion in 2022, propelled by a low base—a factor particularly in 2021—as well as robust export sector activity and recuperating domestic demand. The economy’s momentum is likely to normalize by 2023, with real GDP growth slowing to 1.2% y/y, which is in line with the country’s pre-pandemic average growth between 2010 and 2019.

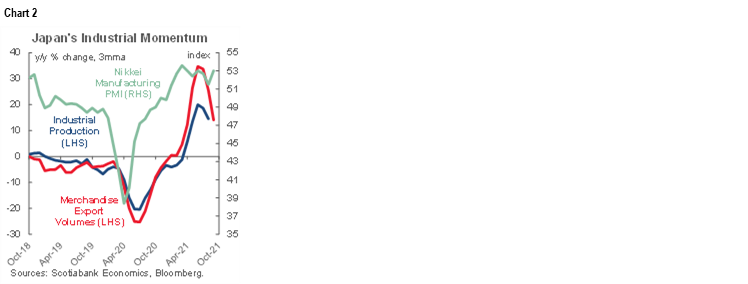

Japan’s external sector has played an important role in the country’s economic recovery, supported by strong overseas demand for Japanese electronics and automotive exports. Nevertheless, the global shortage of semiconductors, transportation bottlenecks, and high input costs have recently started to adversely impact Japanese manufacturing activity and shipments (chart 2). China and the US are Japan’s two most important export destinations, together purchasing 44% of the country’s shipments abroad; while demand dynamics are set to remain solid in the US over the coming quarters, China’s weaker growth trajectory will likely be felt among Japanese exporters. Once the Regional Comprehensive Economic Partnership (RCEP), the world’s largest trade agreement, becomes effective after its ratification is completed, Japanese exporters to China and South Korea (Japan’s third largest export market) in particular are expected to benefit from lower tariffs.

Easing movement restrictions and a rising COVID–19 vaccination coverage are brightening the outlook for domestic demand; currently slightly over 70% of the Japanese population is fully vaccinated. While uncertainties remain elevated, prospects for private consumption are improving as consumer confidence continues its climb toward pre-pandemic levels (chart 3) and as pandemic-related state of emergency measures are lifted. Pent-up demand will likely be reflected in household spending growth, supported by a rebounding labour market and elevated household savings. Meanwhile, in a supportive policy environment, fixed investment is expected to recover gradually over the coming quarters, along with strengthening business confidence and robust global demand.

Japan’s fiscal policy continues to underpin the economy’s recovery; the country’s pandemic-related fiscal response has been one of the highest among the G–20 group and another sizable stimulus bill is expected to be unveiled before the end of the year, once the nation’s new domestic political configuration is established. Japan will hold general elections on October 31. Polls suggest that the ruling Liberal Democratic Party (LDP) and its coalition partner Komeito will be able to maintain a majority. The LDP has a new leader, former finance minister Kishida Fumio, who became Japan’s Prime Minister on October 4, 2021 after his predecessor Suga Yoshihide resigned in September. We expect broad policy continuity over the foreseeable future to help with the economy’s recovery.

INFLATION, MONETARY POLICY AND JAPANESE YEN OUTLOOK

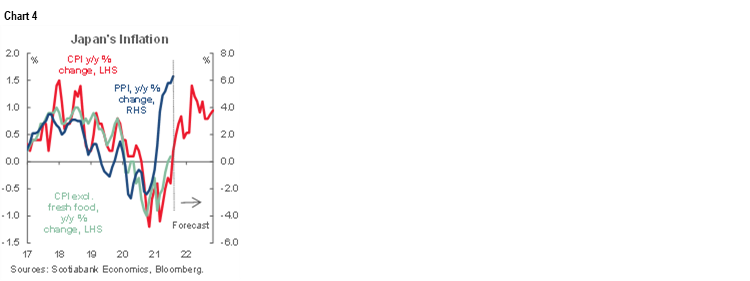

Japan may have finally defeated deflation, which took hold in October 2020, with headline consumer prices increasing by 0.2% y/y in September 2021 (chart 4). Prices excluding fresh food—the Bank of Japan’s (BoJ) preferred inflation measure—advanced by 0.1% y/y. While inflation remains very low, we foresee it climbing somewhat over the coming months. The depressed figures are partially a reflection of a government-initiated cut to mobile phone charges; once the impact fades away, headline inflation will likely temporarily approach 1½% y/y in the spring of 2022. Nevertheless, while higher input prices globally will have some spillover impact on consumer prices, demand-driven inflationary pressures are expected to remain absent in Japan. Accordingly, we see inflation remaining around 1% y/y for most of our forecast horizon, below the BoJ’s 2% inflation target.

The BoJ assesses that Japan’s inflation dynamics differ from the pressures experienced in other advanced economies on the back of three key factors:

1) a delayed domestic demand recovery; 2) Japanese companies’ unwillingness to pass higher costs to consumers; and 3) low wage pressures. Partially due to Japan’s employment practices, Japan is not facing significant labour shortages and wage inflation, which are becoming increasingly evident in many of its peer economies. In Japan, the preference for long-term employment kept the unemployment rate relatively steady during the height of the pandemic (the jobless rate rose from 2.1% at end–2019 to the peak of 3.1% in October 2020) as firms primarily adjusted hours worked. Now, with the economy rebounding and production ramping up, Japanese employers have largely avoided the struggle to attract people back to work, which has limited pressure on wages. In August, real cash earnings were up by only 0.2% y/y.

We expect the BoJ to maintain its ultra-loose monetary policy stance for an extended period, well past other major central banks’ monetary normalization timelines. At the BoJ’s most recent monetary policy meeting on October 28, the central bank kept the policy rate at -0.1% and continued the "Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control”, which maintains the 10-year JGB yield at around 0% via the BoJ’s government bond purchases. The BoJ restated its earlier position that the central bank is prepared to take additional monetary easing measures if needed, and that it expects policy interest rates to remain “at their present or lower levels”. We do not foresee any changes to the BoJ’s policy parameters before the end of 2023.

The Japanese yen (JPY) has faced notable weakening pressure against the US dollar (USD) in recent weeks (chart 5), crossing the 110-threshold at end-September. The shift largely reflects rising interest rate differentials between the US and Japan as the US Federal Reserve prepares for tapering of its bond purchase program. Moreover, higher energy prices are eroding Japan’s positive trade balance that is providing support to the JPY. We forecast USDJPY to close the year at 113. Divergent monetary policies are set to weaken the yen further over the course of 2022, taking USDJPY to 116 by the end of 2022.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.