Another surge in COVID-19 infections clouds Japan’s near-term outlook; a solid recovery is expected in the second half of 2021, taking the nation’s real GDP growth to 3.0% this year.

Japan’s external sector is an important driver of economic activity, while domestic demand prospects remain more uncertain due to the evolving COVID-19 situation. Fiscal policy is set to remain growth-supportive until the economy is back on its feet.

Given Japan’s muted inflationary pressures through the foreseeable future, the Bank of Japan is set to maintain its ultra-loose monetary policy stance much longer than other major central banks.

ECONOMIC GROWTH OUTLOOK

Japan’s economic recovery is facing notable downside risks. The country’s real GDP rebounded strongly in the second half of 2020, yet renewed weakness has appeared in the early months of 2021 on the back of another surge in COVID-19 infections (chart 1). Virus-related containment efforts likely triggered a contraction in real GDP in the first quarter of 2021. The situation has not stabilized yet, prompting the Japanese government to declare targeted state of emergency measures in Tokyo, Osaka, Hyogo and Kyoto prefectures from April 25 to May 11. The latest development threatens to delay the economy’s recovery as the measures cover areas that account for about one-third of the nation’s output. Nonetheless, we expect momentum to strengthen in the second half of the year, with Japanese real GDP forecasted to grow by 3.0% in 2021, compared with a 4.9% contraction in 2020. In 2022, economic growth will likely approach a more traditional trajectory with output gains forecasted to average 1.2% y/y.

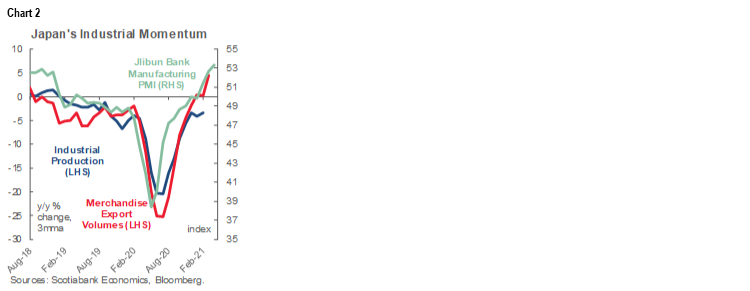

Japan’s external sector has been a driver of economic activity (chart 2), supported by strong overseas demand for Japanese electronics exports. Nevertheless, the global shortage of semiconductors will likely dampen Japanese auto production and shipments. As the global economic recovery will continue to be led by the US and China over the coming quarters—Japan’s two most important export destinations—net exports are set to provide support to GDP growth through 2022.

The outlook for private consumption will be influenced by near-term virus developments, as concerns about infections and a slow vaccination rollout may halt the recent rebound in consumer sentiment (chart 3). Moreover, spending prospects depend on the fate of the once-delayed Tokyo Olympics in July. Foreign spectators have been barred from the Games while organizers have yet to decide whether a domestic audience will be permitted. Furthermore, if the virus situation gets out of control, cancelling the Games altogether remains an option. Such a scenario would delay Japan’s economic recovery significantly. Should the Games proceed as planned, we expect pent-up demand to boost consumption in the second half of the year, assisted by a gradually improving labour market (chart 3) and elevated household savings. Meanwhile, fixed investment is expected to rebound gradually over the coming quarters, along with a supportive policy environment, strengthening business confidence and robust global demand.

Japan’s fiscal policy continues to underpin the economy’s recovery. The record ¥106.61 trillion (US$976 bn) Budget for fiscal year 2021 (April–March) is targeted at offsetting the pandemic’s adverse impact on the economy and buttressing the country’s health care system. Nevertheless, we assess that supplementary spending will likely be unveiled over the coming months. Japan’s pandemic-related fiscal response has been the highest among the G-20 group. According to the IMF, the country’s fiscal measures as of mid-March 2021 were equivalent to over 44% of GDP, consisting of around 16% of GDP of additional spending and over 28% of GDP of liquidity support. While the substantial fiscal stimulus is leading to a rise in public debt—Japan’s gross debt was equivalent to 256% of GDP in 2020, according to the IMF—we note that the government does not rely on external financing for its debt as almost 90% of it is held domestically, primarily by the Bank of Japan (BoJ) and other public institutions, banks, and pension funds. We assess that any debt-related turmoil is a distant possibility in Japan.

INFLATION, MONETARY POLICY AND YEN OUTLOOK

Japan’s inflation will remain muted through 2022, with the BoJ’s 2% annual inflation target being unachievable in the foreseeable future. The headline CPI has been in deflationary territory over the past six months; prices dropped by 0.2% y/y in March. The CPI excl. fresh food—the BoJ’s preferred inflation measure—decreased by 0.1% y/y in March, the 8th consecutive month of price declines (chart 4). While we expect a slight pickup in prices over the coming months, persisting slack in the economy and low wage gains will keep price pressures at bay. Indeed, inflation expectations have weakened, and the annual “Shunto” spring wage negotiation resulted in an increase of 1.8% in 2021—the lowest pay rise in eight years. We forecast headline inflation to close 2021 at 0.8% y/y. By the end of 2022 inflation is expected to reach 1.0% y/y, remaining well below the BoJ’s target.

The BoJ will likely maintain its ultra-loose monetary policy stance for an extended period, well past other major central banks’ monetary normalization timelines. We foresee that the BoJ will keep the policy rate at -0.1% and continue the "Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control” that maintains the 10-year JGB yield at around 0% via the BoJ’s government bond purchases.

The BoJ has recently added flexibility its monetary policy toolkit. In March 2021, it completed its assessment for “Further Effective and Sustainable Easing”. The BoJ introduced a wider +/-25 bps range for the 10-year bond yield target to improve the bond market’s functioning. Meanwhile, given that the negative policy rate has caused challenges for financial institutions’ profitability, the central bank announced that it would offer counterbalancing measures for banks if the policy rate was lowered further into negative territory. The central bank’s assessment found that ETF and J-REIT purchases have been effective in lowering the risk premia in the stock market, promoting economic activity. However, the BoJ also flagged concerns regarding indirect shareholding and corporate governance. To address these issues, it removed its earlier pledge to buy at least JPY 6 trillion of ETFs annually, yet it maintained the annual upper limit of JPY 12 trillion. From now on, the BoJ will only purchase ETFs that track the TOPIX. Overall, we assess that the tweaks announced make the BoJ’s accommodative monetary policy stance more sustainable.

The Japanese yen (JPY) depreciated by 7% against the US dollar (USD) in the first quarter of 2021 (chart 5) on the back of rising US yields and a faster economic recovery in the US. While we consider the yen’s Q1 depreciation excessive—indeed, the JPY has regained some of the losses in April—we expect limited further appreciation through the rest of the year with USDJPY closing 2021 at 107. As monetary policy normalization approaches in the US while the BoJ’s policy stance is set to remain ultra-accommodative for an extended period, the JPY is expected to return to the 110 mark in the second half of 2022.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.